Key Takeaways

- Growth in U.S. initiatives and expanded sandwich group capacity could significantly increase revenues and operational margins by leveraging multiple sales channels and international markets.

- Investments in automation and balance sheet strategies, including asset sales and sale-leasebacks, may improve efficiency, financial flexibility, and support growth opportunities.

- Operational inefficiencies and external economic factors, combined with client onboarding delays and segment weaknesses, pose significant risks to revenue growth and net margins.

Catalysts

About Premium Brands Holdings- Through its subsidiaries, manufactures and distributes food products primarily in Canada and the United States.

- Premium Brands Holdings has a strong business development pipeline with a potential revenue run rate of $704 million from new U.S. initiatives expected to materialize in 2025, which could significantly boost overall revenues.

- The company has increased capacity to meet demand in its sandwich group, with growth opportunities in multiple channels, such as club stores and international markets, which could enhance revenues and improve operational margins.

- Expected stabilization and potential organic growth in the beef jerky and convenience store segments by 2025 could remove current revenue headwinds and support better net margins due to improved economies of scale.

- Premium Brands is investing in automation at key facilities, like the San Leandro bakery plant, which is projected to complete by the end of 2024, potentially leading to increased efficiency, lower costs, and improved margins starting in 2025.

- Anticipated balance sheet strengthening through asset sales and sale-leaseback transactions could provide financial flexibility to execute on growth strategies, potentially enhancing earnings and aligning capital structure with growth opportunities.

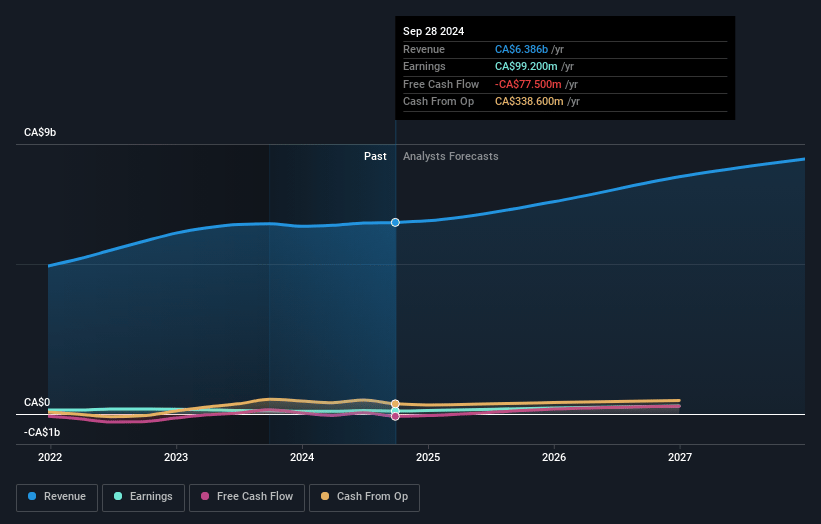

Premium Brands Holdings Future Earnings and Revenue Growth

Assumptions

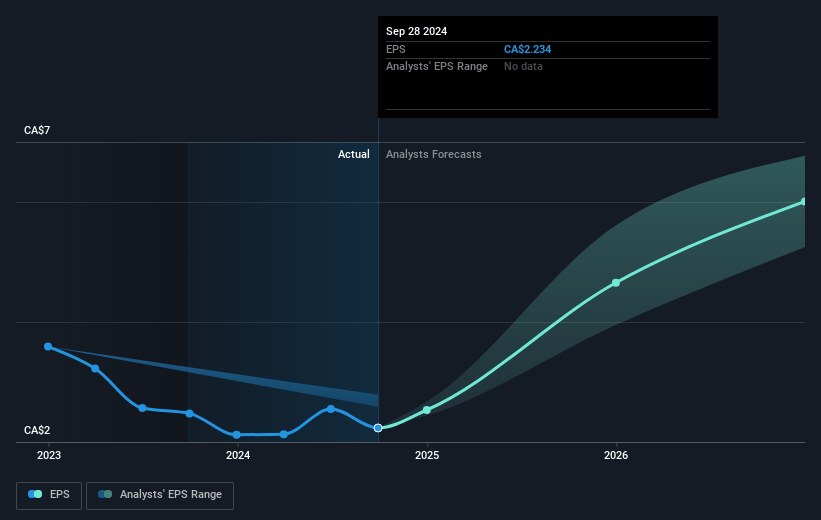

How have these above catalysts been quantified?- Analysts are assuming Premium Brands Holdings's revenue will grow by 9.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.6% today to 4.4% in 3 years time.

- Analysts expect earnings to reach CA$366.9 million (and earnings per share of CA$8.25) by about February 2028, up from CA$99.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.5x on those 2028 earnings, down from 33.7x today. This future PE is greater than the current PE for the CA Food industry at 12.8x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.74%, as per the Simply Wall St company report.

Premium Brands Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is facing delays in onboarding new clients, with concerns about the timing of launching programs. This could negatively impact revenue growth if anticipated sales do not materialize as expected.

- The Specialty Foods segment is experiencing weakness due to lower volumes, beef jerky sales declines, and weak spending in convenience stores and food service, which may affect net margins and earnings if these trends persist.

- There are operational issues at several new U.S. facilities, including debottlenecking problems and inefficiencies, which could affect production capacity, leading to potential cost overruns and impacting net margins.

- The reliance on a large QSR (Quick Service Restaurant) customer facing sales slowdowns poses a risk of decreased revenue if their challenges are not resolved quickly, impacting overall growth targets and earnings.

- External economic factors such as high lobster prices and weak international markets are affecting their Premium Food Distribution Group, with implications for international revenue streams and margin pressures.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$102.4 for Premium Brands Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$120.0, and the most bearish reporting a price target of just CA$90.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$8.3 billion, earnings will come to CA$366.9 million, and it would be trading on a PE ratio of 14.5x, assuming you use a discount rate of 5.7%.

- Given the current share price of CA$74.54, the analyst price target of CA$102.4 is 27.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives