Key Takeaways

- Project completions and tie-ins position Cenovus for increased production reliability, boosting future revenue and margins.

- Expanded oil sands output and improved market access drive revenue growth with low capital costs and enhanced realized prices.

- Reliability challenges and project delays, coupled with transport and crude price risks, could strain cash flow, affect margins, and impact earnings if not managed well.

Catalysts

About Cenovus Energy- Develops, produces, refines, transports, and markets crude oil, natural gas, and refined petroleum products in Canada and internationally.

- The completion of major turnarounds ahead of schedule and effective tie-in work for future projects positions Cenovus well for increased production reliability and operational efficiency, potentially boosting future revenue and margins.

- The ongoing development of the Narrows Lake project and optimization at Sunrise and Foster Creek are on track to increase oil sands production by 20,000 to 30,000 barrels per day in mid-2025, which is expected to support revenue growth at low capital costs.

- The recent commencement of the TMX pipeline has improved market access for Cenovus' crude, leading to a narrower WCS differential, which can enhance their revenue through higher realized prices.

- Significant progress on the West White Rose project, expected to start production in 2026, could transition from a cost to a significant cash flow generator, impacting earnings positively once operational.

- Refinery improvements post-turnaround, such as at Lloydminster and Lima, aim to resolve reliability issues that, once addressed, could enhance profitability and margin capture in the refining segment.

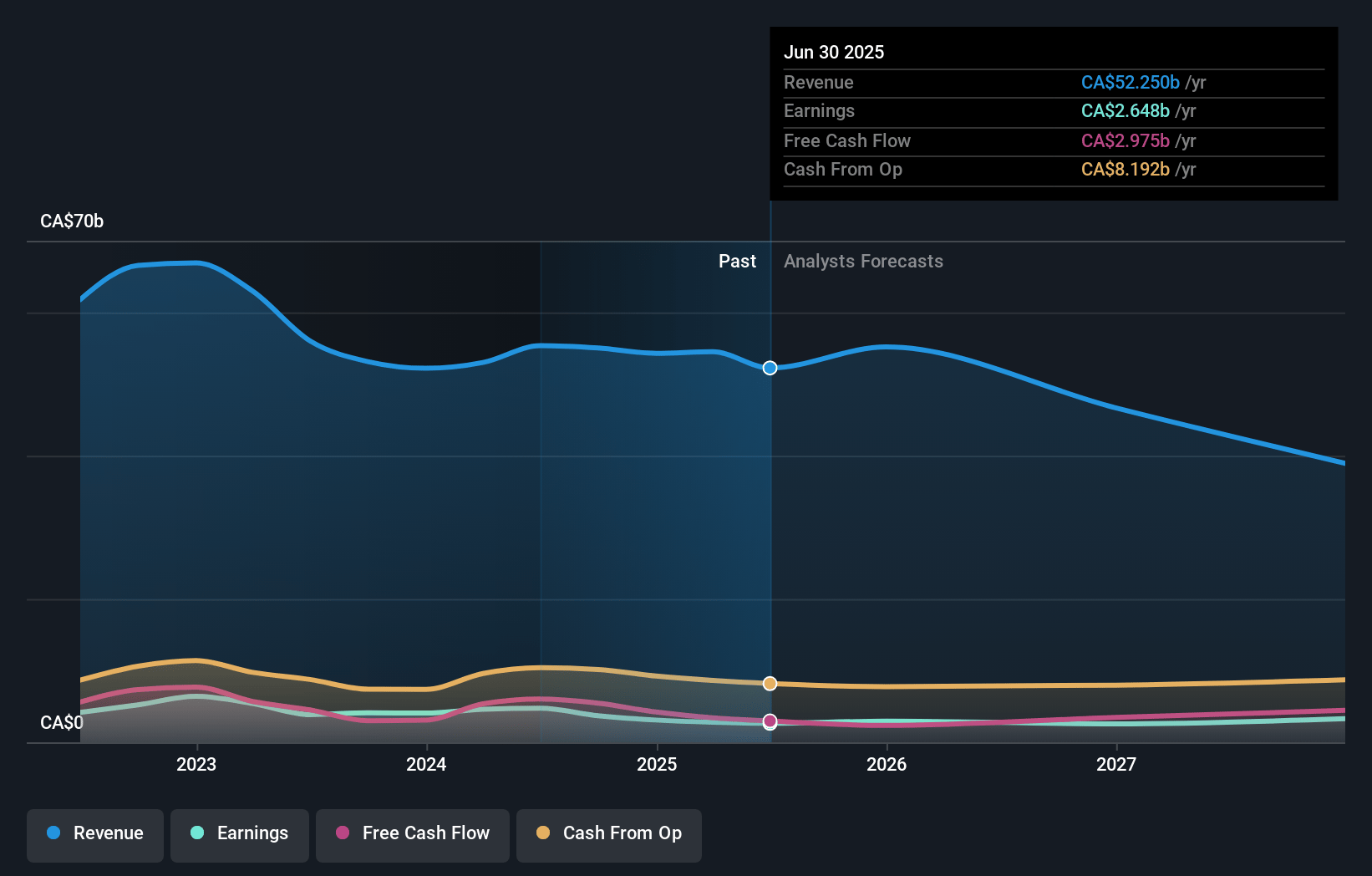

Cenovus Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Cenovus Energy's revenue will grow by 1.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.7% today to 7.7% in 3 years time.

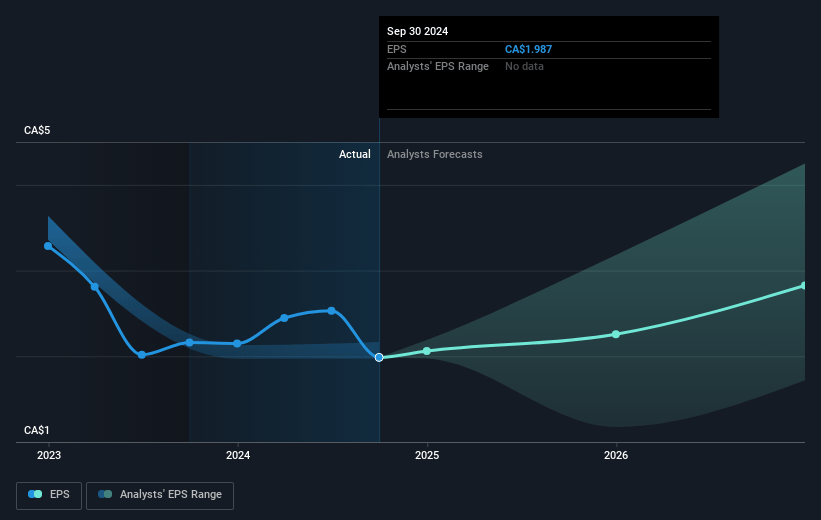

- Analysts expect earnings to reach CA$4.5 billion (and earnings per share of CA$2.9) by about January 2028, up from CA$3.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CA$5.7 billion in earnings, and the most bearish expecting CA$3.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.8x on those 2028 earnings, up from 10.4x today. This future PE is greater than the current PE for the US Oil and Gas industry at 10.9x.

- Analysts expect the number of shares outstanding to decline by 5.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.13%, as per the Simply Wall St company report.

Cenovus Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company has faced reliability challenges in its downstream operations, particularly in U.S. refining, impacting throughput and profitability. Efforts to address equipment issues and improve reliability could increase costs and affect net margins if not successfully managed.

- Moody projections for portion of upstream production not covered by existing takeaway capacities and reliance on rail transport in strategic decisions could lead to higher transport costs and impact earnings if differentials widen unexpectedly.

- Seasonality and weather-dependent project start-ups, such as the Narrows Lake steam line completion, present operational risks that could delay production increases and affect revenue.

- Sustained lower crude prices could challenge the company's ability to maintain dividend payouts and growth capital, potentially impacting shareholder returns and financial stability if prices trend below margins conducive to covering total expenses.

- The company is susceptible to capital expenditure overruns and project delays, such as seen with potentially uncertain toll resolutions and large investments like the West White Rose project, which could strain cash flow and impact earnings if not managed efficiently.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$30.32 for Cenovus Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$34.37, and the most bearish reporting a price target of just CA$25.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$58.4 billion, earnings will come to CA$4.5 billion, and it would be trading on a PE ratio of 12.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of CA$21.0, the analyst's price target of CA$30.32 is 30.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives