Narratives are currently in beta

Key Takeaways

- Increased long-term contract backlog and higher uranium prices suggest revenue growth potential from committed volumes.

- Strategic production optimization efforts at key sites aim to boost profitability without large capital expenditure, enhancing operational efficiency.

- Challenges with sulfuric acid supply, uranium contract uncertainties, and geopolitical issues could negatively impact Cameco's production, revenue consistency, and net margins.

Catalysts

About Cameco- Provides uranium for the generation of electricity.

- Cameco is aiming to enhance production efficiency by returning to a Tier 1 cost structure, potentially increasing net margins by reducing operational costs and optimizing production at existing sites without significant capital expense.

- There is a notable increase in backlog of long-term contracts from utilities, suggesting potential revenue growth from higher committed volumes amid rising uranium and fuel services prices.

- Planned scaling up of production at McArthur River and Key Lake with automation and optimization could boost future revenues and profitability without substantial additional spending.

- The company's strategic flexibility in inventory, purchases, and supply sources to meet contract demands positions it well to maintain robust earnings and revenue even amid supply uncertainties.

- Westinghouse's positive long-term outlook, with forecasted adjusted EBITDA growth, suggests increasing profitability from nuclear fuel cycle services and positions Cameco to capitalize on nuclear energy growth trends, potentially enhancing overall earnings.

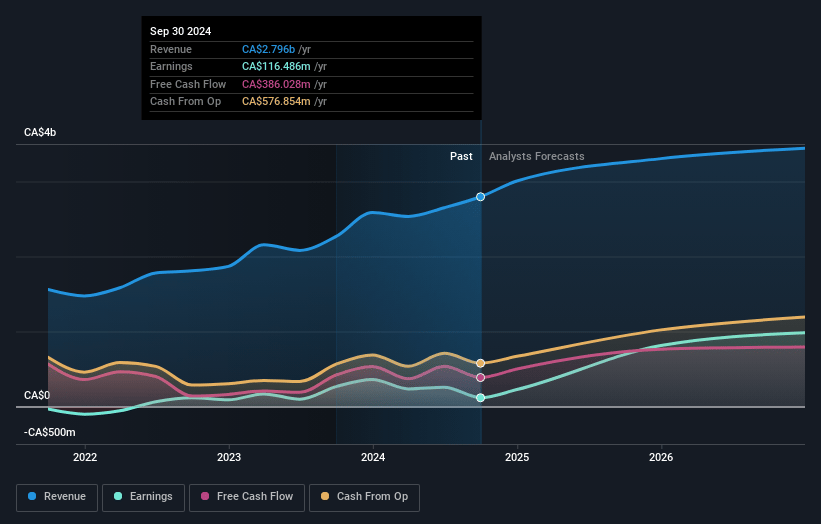

Cameco Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Cameco's revenue will grow by 6.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.2% today to 31.7% in 3 years time.

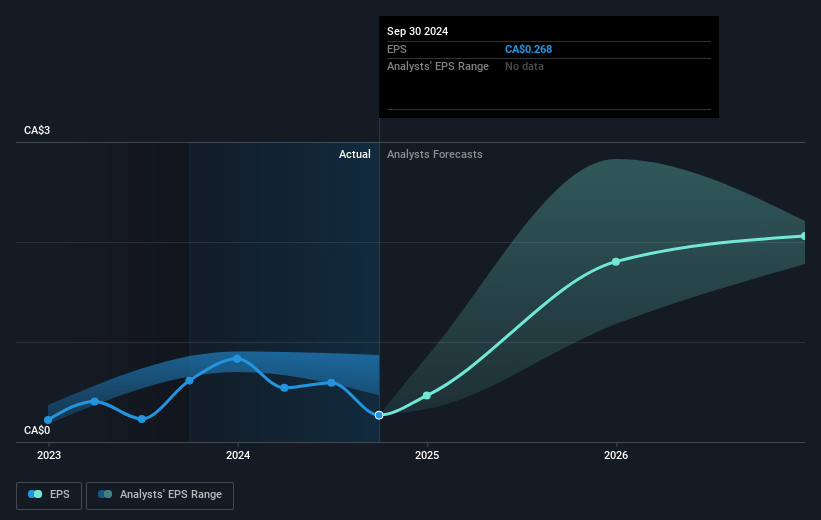

- Analysts expect earnings to reach CA$1.1 billion (and earnings per share of CA$2.32) by about January 2028, up from CA$116.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CA$1.2 billion in earnings, and the most bearish expecting CA$773.5 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 45.3x on those 2028 earnings, down from 261.4x today. This future PE is greater than the current PE for the US Oil and Gas industry at 10.9x.

- Analysts expect the number of shares outstanding to grow by 1.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.68%, as per the Simply Wall St company report.

Cameco Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There are ongoing challenges related to sulfuric acid supply in Kazakhstan, which have impacted production levels at the Inkai mine. This could negatively affect future production and, consequently, Cameco's revenue and supply consistency.

- There is a tendency for long-term contracting through the first nine months of the year to remain slow, indicating potential uncertainty or cautiousness among utilities about future uranium prices. This could impact Cameco's ability to secure its future revenue streams.

- Equity earnings from Westinghouse are being adversely impacted by the amortization of intangible assets due to acquisition accounting requirements, which might distort actual performance and impact reported net earnings.

- The U.S. ban on Russian uranium imports has created uncertainty in the supply chain, affecting procurement plans and producers' sales strategies. This geopolitical uncertainty can impact revenue projections and long-term security of supply.

- Incremental increases in production at key facilities have been noted, but Cameco may face increased Cost of Goods Sold (COGS) due to inflationary pressures and reliance on various procurement strategies to fulfill commitments, potentially impacting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$86.75 for Cameco based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$97.0, and the most bearish reporting a price target of just CA$77.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$3.4 billion, earnings will come to CA$1.1 billion, and it would be trading on a PE ratio of 45.3x, assuming you use a discount rate of 6.7%.

- Given the current share price of CA$69.97, the analyst's price target of CA$86.75 is 19.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives