Key Takeaways

- Transition to a capital-light model and strong focus on capital sales increases backlog, positively impacting future revenue and earnings.

- Strategic partnerships and expansion projects in Italy and Japan, backed by incentives, enhance capacity, technology, and competitive advantage.

- Declining revenue and increased SG&A expenses signal potential challenges in growth, profitability, and cash flow, despite improvements in net loss.

Catalysts

About Anaergia- Provides solutions for the generation of renewable energy and conversion of waste to resources in Italy, North America, Europe, the Middle East and Africa, and the Asia Pacific.

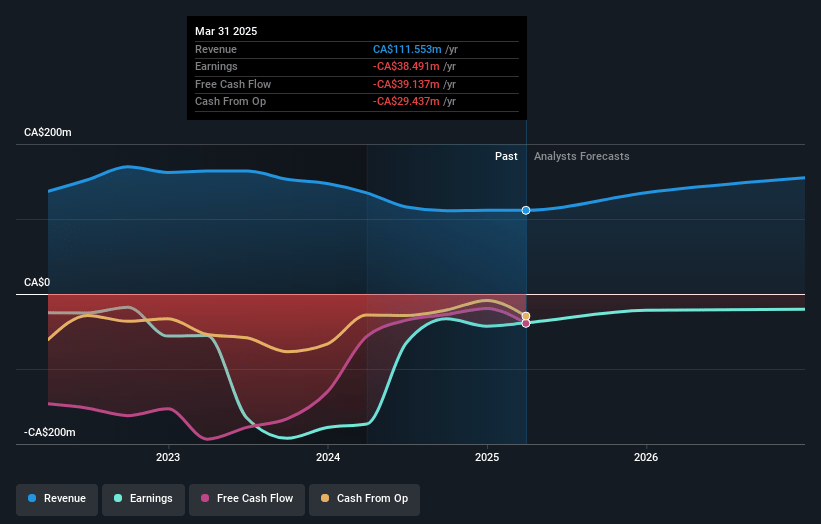

- Anaergia's transition to a capital-light model, with a strong focus on capital sales, has more than doubled its backlog since last year, which is expected to positively impact future revenue and earnings.

- Strengthening its capital market presence by trading on the OTCQX, Anaergia aims to improve its visibility and accessibility to U.S. investors, potentially leading to enhanced investment, which can bolster future revenue growth.

- The recent strategic partnerships and expansion projects in Italy and Japan, including major biomethane facility constructions, are poised to drive significant capacity and technological advancements, likely increasing revenue in the long term.

- The execution of these projects, backed by government incentives such as REPowerEU, is expected to provide Anaergia with a competitive advantage in rapidly growing markets, thus potentially boosting both revenue and net margins.

- Anaergia's strategic approach in North America and Singapore, through partnerships with universities and government projects, aims to secure long-term service contracts, which can stabilize earnings and improve net margins going forward.

Anaergia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Anaergia's revenue will grow by 20.7% annually over the next 3 years.

- Analysts are not forecasting that Anaergia will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Anaergia's profit margin will increase from -34.5% to the average CA Commercial Services industry of 4.2% in 3 years.

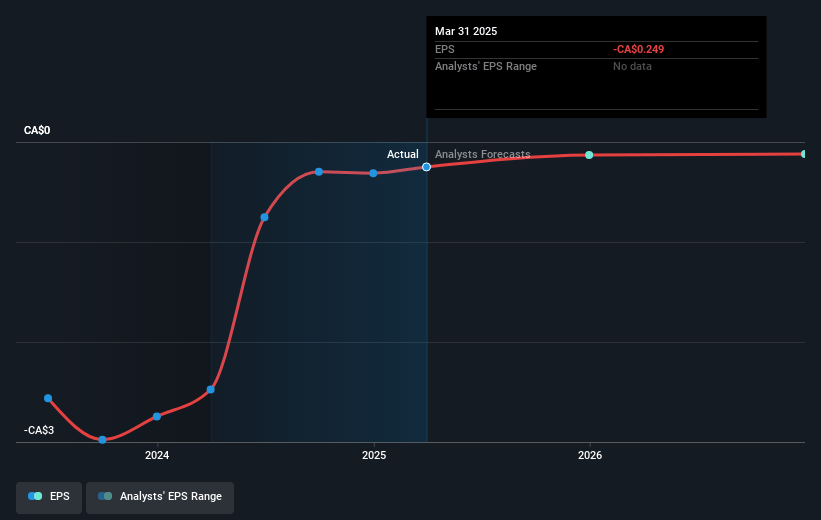

- If Anaergia's profit margin were to converge on the industry average, you could expect earnings to reach CA$8.2 million (and earnings per share of CA$0.04) by about July 2028, up from CA$-38.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.8x on those 2028 earnings, up from -6.1x today. This future PE is greater than the current PE for the CA Commercial Services industry at 25.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.53%, as per the Simply Wall St company report.

Anaergia Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Revenues showed a slight decrease of 0.4% compared to the previous year, primarily due to lower capital sales and food revenue, while APAC and Italy exhibited revenue decline, which can potentially impact future revenue growth.

- The net loss for the quarter was $5.9 million, though it improved compared to the previous year, indicating that profitability is still a concern, potentially affecting net margins.

- Gross profit for the quarter decreased by 16.6%, largely due to reduced profitability in the Food segment, affecting overall earnings and net margins.

- SG&A expenses increased by 3.4% due to a specific reserve against accounts receivable, which highlights potential issues with collections and cash flow management, impacting net margins.

- The Boost segment's revenue saw a slight decline, caused by the planned idling of a facility to reduce operating losses, illustrating potential challenges in maintaining revenue streams and earnings from certain facilities.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$1.3 for Anaergia based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$195.9 million, earnings will come to CA$8.2 million, and it would be trading on a PE ratio of 39.8x, assuming you use a discount rate of 6.5%.

- Given the current share price of CA$1.39, the analyst price target of CA$1.3 is 6.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.