Key Takeaways

- Strategic growth initiatives in sanitation and improved operational efficiencies in renewables are likely to enhance future revenue and earnings.

- Capital strengthening and cost management bolster financial stability and potentially improve margins and overall performance.

- Financial strain from acquired investments, supply chain issues, legal matters, and ambitious growth strategy may pressure margins and affect future revenue and earnings.

Catalysts

About Equatorial Energia- Through its subsidiaries, engages in the electricity generation, distribution, and transmission operations in Brazil.

- The capital increase of R$2.5 billion through private subscription strengthens Equatorial Energia's balance sheet, allowing for debt repayment and potentially improving future earnings by reducing interest expenses.

- The significant growth in distributed energy, up 6.7%, highlights future revenue potential, driven by rising incomes and increased energy demand, which is expected to maintain momentum.

- The acquisition of a 15% stake in SABESP and subsequent optimizations position Equatorial for strategic growth in the sanitation sector, potentially increasing future revenue streams and enhancing earnings.

- The implementation of new transmission lines and improved operational efficiencies in the renewables segment are expected to reduce curtailment impacts, potentially boosting revenue and improving margins for energy generation.

- A disciplined approach to cost management and operating efficiency, alongside investment in new infrastructure, supports sustained EBITDA growth, potentially enhancing net margins and overall financial performance.

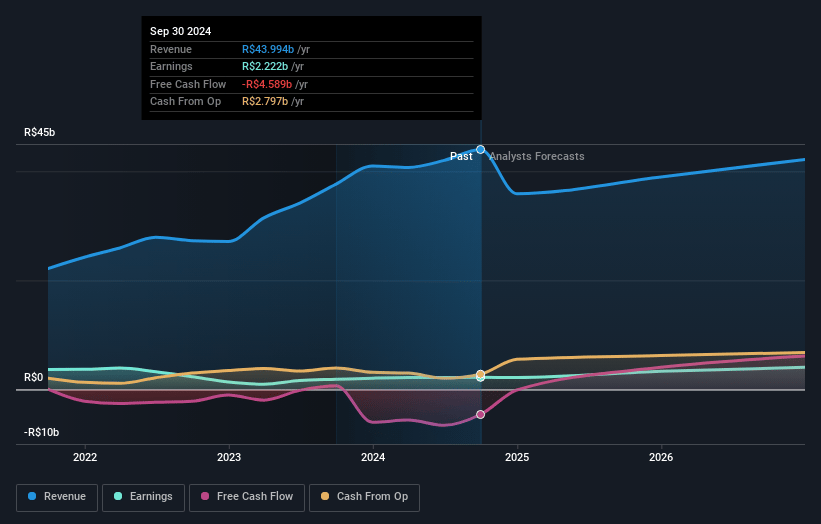

Equatorial Energia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Equatorial's revenue will decrease by 0.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.1% today to 9.2% in 3 years time.

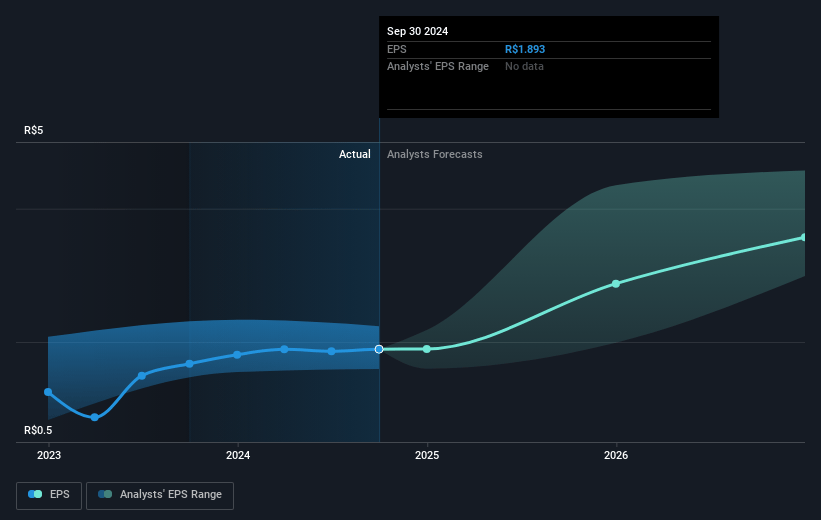

- Analysts expect earnings to reach R$4.1 billion (and earnings per share of R$3.65) by about January 2028, up from R$2.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting R$5.4 billion in earnings, and the most bearish expecting R$2.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.9x on those 2028 earnings, up from 16.5x today. This future PE is greater than the current PE for the BR Electric Utilities industry at 8.6x.

- Analysts expect the number of shares outstanding to decline by 3.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 17.06%, as per the Simply Wall St company report.

Equatorial Energia Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company has experienced an increase in net debt due to the acquisition of a stake in SABESP, which could impact the financial leverage and potentially pressure margins and earnings if leverage is not effectively managed.

- There are concerns about supply chain challenges in acquiring equipment for transmission and distribution, which could hinder the company's ability to execute on its CapEx plans, impacting future revenue and profitability.

- Ongoing discussions regarding reductions in energy curtailment and changes in methodology for energy cuts could affect the performance of their renewables segment and possibly decrease expected revenue from those assets.

- The company is involved in ongoing legal and regulatory matters, including the extension of concessions and litigation with ANEEL, which could create uncertainties and potentially impact revenue and expenses.

- Equatorial Energia's growth strategy includes possible inorganic moves, which could lead to increased financial risk if such acquisitions or investments do not yield expected returns, affecting future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of R$42.92 for Equatorial based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$50.1, and the most bearish reporting a price target of just R$34.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be R$44.6 billion, earnings will come to R$4.1 billion, and it would be trading on a PE ratio of 18.9x, assuming you use a discount rate of 17.1%.

- Given the current share price of R$29.35, the analyst's price target of R$42.92 is 31.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives