Narratives are currently in beta

Key Takeaways

- Cost management improvements and diversification of funding sources enhance financial flexibility, enabling potential CapEx investment and revenue growth.

- Transitioning to an integrated structure with advanced technologies should improve operational efficiency, supporting enhanced net margins and market position.

- Eletrobras faces revenue instability due to hydropower reliance, market uncertainties, regulatory risks, and potential impacts from legacy liabilities and exchange rate fluctuations.

Catalysts

About Centrais Elétricas Brasileiras - Eletrobrás- Through its subsidiaries, engages in the generation, transmission, and commercialization of electricity in Brazil.

- Eletrobras is targeting operational efficiency through significant cost management improvements, aiming to reduce PMSO to R$5.5 million by 2026. This should improve net margins as the company enhances its cost structure.

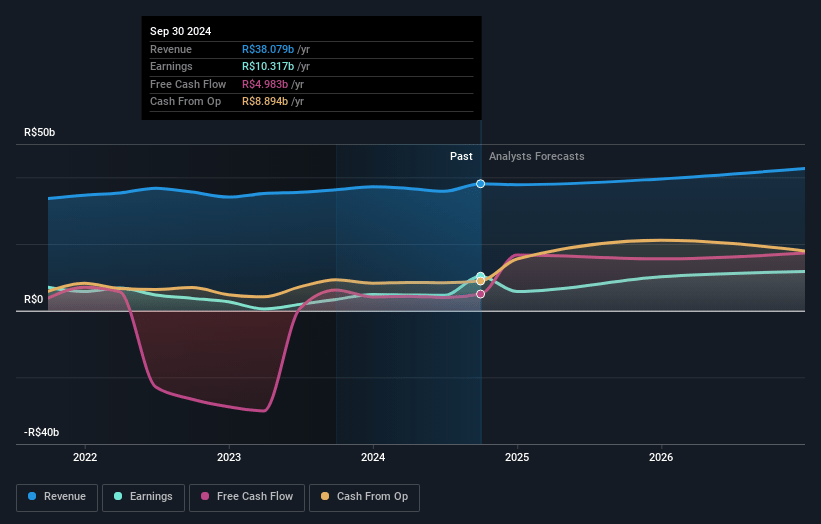

- The company has fortified its cash position by diversifying funding sources, raising R$22 billion in 2024 alone. This provides financial flexibility for future capital allocation, potentially leading to increased CapEx investment and revenue growth.

- Eletrobras is focusing on resolving legacy liabilities and non-recurring issues, which should positively impact future earnings by reducing unexpected financial hits.

- The transition to a more integrated company structure, along with the use of advanced technologies such as AI and machine learning, positions Eletrobras for enhanced operational efficiency and growth, potentially boosting net margins.

- The marketplace dynamics and evolving energy regulations create opportunities for Eletrobras to stabilize and potentially increase energy prices, supporting revenue growth and establishing a more robust position in the energy market.

Centrais Elétricas Brasileiras - Eletrobrás Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Centrais Elétricas Brasileiras - Eletrobrás's revenue will grow by 2.9% annually over the next 3 years.

- Analysts are assuming Centrais Elétricas Brasileiras - Eletrobrás's profit margins will remain the same at 27.1% over the next 3 years.

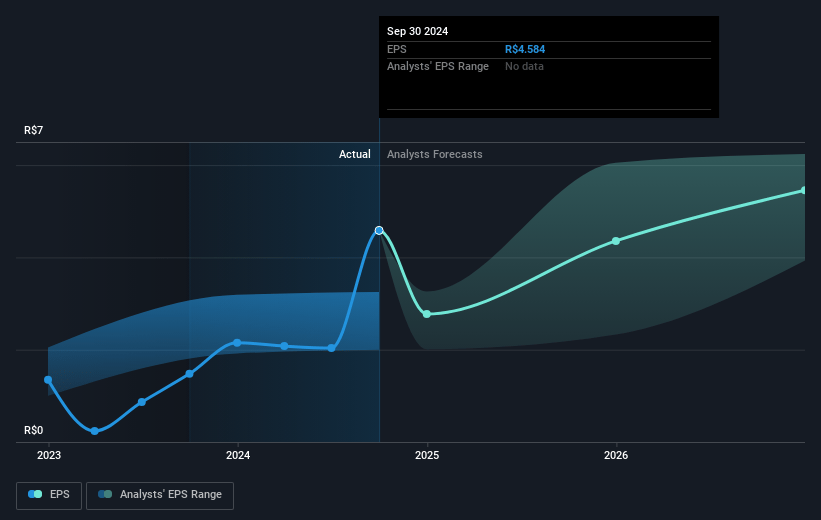

- Analysts expect earnings to reach R$11.3 billion (and earnings per share of R$5.66) by about January 2028, up from R$10.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting R$14.8 billion in earnings, and the most bearish expecting R$10.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.6x on those 2028 earnings, up from 8.6x today. This future PE is greater than the current PE for the US Electric Utilities industry at 8.6x.

- Analysts expect the number of shares outstanding to decline by 3.99% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.64%, as per the Simply Wall St company report.

Centrais Elétricas Brasileiras - Eletrobrás Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Eletrobras' results involve significant fluctuations and challenges related to hydropower modulation, which indicate reliance on volatile spot prices, potentially impacting revenue stability and future earnings.

- The company faces uncertainties surrounding the execution of investment plans, regulatory approvals, and rising equipment prices due to exchange rate depreciation, which could affect operating costs and capital expenditure efficiency.

- There is ongoing volatility and potential delinquency risks in Brazil's energy market, which could impact contract negotiations and price stability, presenting risks to future revenue.

- The streamlined management structure and cost-cutting initiatives depend on predictable regulatory outcomes and internal transformations, which, if delayed or insufficient, could pressure operational margins.

- Eletrobras still carries significant legacy liabilities, and while reductions are underway, unexpected compulsory loan adjustments could impact net margins and overall financial health.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of R$55.7 for Centrais Elétricas Brasileiras - Eletrobrás based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be R$41.5 billion, earnings will come to R$11.3 billion, and it would be trading on a PE ratio of 15.6x, assuming you use a discount rate of 16.6%.

- Given the current share price of R$39.56, the analyst's price target of R$55.7 is 29.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives