Key Takeaways

- Expansion and digital investment aim to increase market share and boost revenue via mature store growth and new store openings.

- Focus on health services and cost management seeks to improve margins, enhancing operating earnings and overall financial performance.

- Regulatory changes, intense competition, strained resources from rapid expansion, medication availability issues, and scaling challenges could impede RD Saude's revenue and profitability growth.

Catalysts

About Raia Drogasil- Engages in the retail sale of medicines, perfumery, personal care and beauty products, cosmetics, dermocosmetics, and specialty medicines in Brazil.

- RD Saude is focusing on growing its mature stores above inflation, which is expected to drive revenue growth as these stores increasingly contribute to the company's earnings.

- The company is aggressively expanding its footprint by opening new stores, with plans to reach the high end of its guidance range of 280 to 300 store openings, likely increasing its market share and future revenue potential.

- RD Saude's significant investment in digital platforms is expected to enhance customer engagement and sales, particularly of OTC and health-related products, thus bolstering revenue and potentially improving net margins due to the efficiencies of digital sales.

- The focus on health services, including the establishment of health hubs and pharmacy services, positions the company to capture additional revenue streams as pharmacies are redefined in consumer perception, potentially improving both top-line growth and net earnings.

- Strategic efforts to manage and reduce G&A expenses, alongside increasing personnel efficiencies, are expected to result in net margin improvements, supporting robust operating earnings for the company going forward.

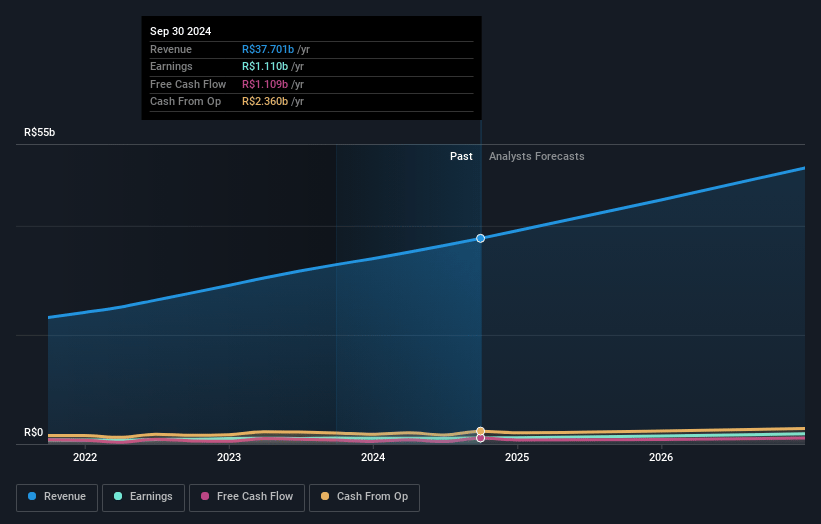

Raia Drogasil Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Raia Drogasil's revenue will grow by 14.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.9% today to 3.5% in 3 years time.

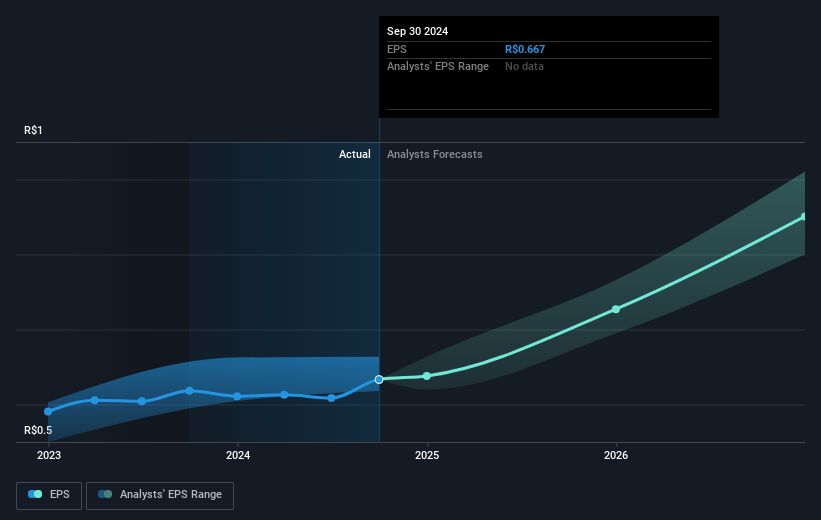

- Analysts expect earnings to reach R$2.0 billion (and earnings per share of R$1.15) by about January 2028, up from R$1.1 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as R$1.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.4x on those 2028 earnings, up from 32.4x today. This future PE is greater than the current PE for the BR Consumer Retailing industry at 11.8x.

- Analysts expect the number of shares outstanding to grow by 0.48% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.78%, as per the Simply Wall St company report.

Raia Drogasil Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The potential for regulatory changes in taxation and pricing could create unpredictability in RD Saude's expenses, complicating margin forecasts. This uncertainty might affect net margins if costs rise faster than anticipated price increases.

- Intense competition from local and national pharmacy chains could impact RD Saude's ability to gain market share as efficiently as before, potentially affecting future revenue growth.

- The company's rapid expansion into smaller towns could strain resources and management bandwidth, potentially impacting operational efficiency and margins if new stores take longer to mature.

- Fluctuations in the availability of specific high-demand medications such as semaglutide derivatives (e.g., Ozempic and Wegovy) could disrupt short-term sales and profitability in specific regions or segments.

- Challenges in effectively scaling digital and health services solutions, such as ensuring high NPS scores and maximizing digital engagement, could limit potential revenue enhancements and impact future profitability margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of R$28.54 for Raia Drogasil based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$33.0, and the most bearish reporting a price target of just R$19.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be R$56.7 billion, earnings will come to R$2.0 billion, and it would be trading on a PE ratio of 39.4x, assuming you use a discount rate of 16.8%.

- Given the current share price of R$21.0, the analyst's price target of R$28.54 is 26.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives