Last Update 24 Jun 26

BAR: Wireless Meeting Expansion Will Support Upside Despite Recent Bearish Downgrade

Analysts have trimmed their price target on Barco to €12.25, reflecting updated assumptions around slightly lower discount rates, modestly higher revenue, improved profit margins, and a more conservative future P/E multiple.

What’s in the News for Barco

- Barco and Huddly AS are expanding their collaboration with a new wireless room system bundle that combines Barco’s ClickShare Hub Pro with the Huddly C1 video bar, aimed at small and medium meeting rooms.

- The new Barco and Huddly bundle is designed as a Microsoft Teams Rooms solution, Certified for Microsoft Teams, and built on Microsoft’s Device Ecosystem Platform, with a focus on security by design and centralized IT management.

- Barco has announced an upcoming Special and Extraordinary Shareholders Meeting scheduled for April 30, 2026, at 15:45 Romance Standard Time.

Valuation Changes for Barco

- Fair Value: €12.25 remains unchanged, indicating no adjustment to the central valuation estimate.

- Discount Rate: The discount rate has fallen slightly from 8.71% to 8.69%, reflecting a small change in the required return assumption.

- Revenue Growth: The revenue growth assumption has risen moderately from 3.59% to 4.52%, suggesting a somewhat stronger expected sales trajectory for Barco.

- Net Profit Margin: The profit margin assumption has risen slightly from 8.94% to 9.69%, implying a modestly higher expected level of profitability.

- Future P/E: The future P/E multiple has fallen moderately from 11.50x to 10.33x, indicating a more conservative valuation applied to Barco’s projected earnings.

Key Takeaways

- Introducing higher-margin products and focusing on software aims to enhance revenue and gross margins positively.

- Operational enhancements and share buyback initiatives could improve gross profit margins and boost EPS.

- Weak EMEA and APAC performances, ClickShare declines, and reliance on one-time items highlight potential regional and operational challenges affecting revenue and earnings stability.

Catalysts

About Barco- Develops visualization solutions for the entertainment, enterprise, and healthcare markets in the Americas, Europe, Middle East, Africa, and the Asia-Pacific.

- The company plans to introduce new products with better margins this year, particularly in the image processing products, which could positively impact revenues and gross margins.

- The shift towards more software in the product mix aims to drive higher margins, as software typically offers better profit potential compared to hardware products.

- The company is working on its next platform in the ClickShare family, which will increase its reach in the video conferencing market, potentially boosting revenues in the enterprise division.

- Operational improvements, such as the Wuxi factory opening and investments in automation, are expected to enhance gross profit margins.

- The company has initiated a share buyback program up to €60 million, which could positively impact EPS by reducing the number of outstanding shares.

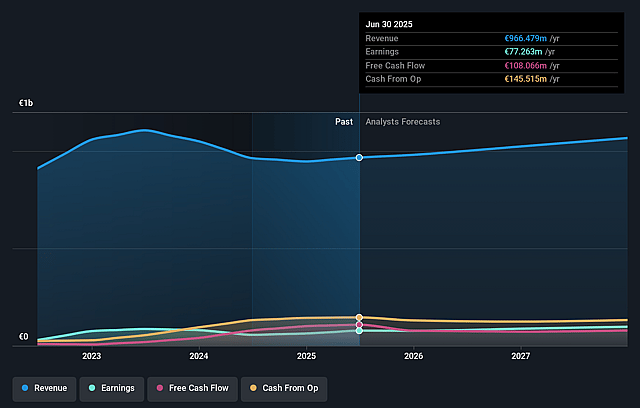

Barco Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Barco's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.4% today to 9.7% in 3 years time.

- Analysts expect earnings to reach €106.6 million (and earnings per share of €1.01) by about June 2029, up from €71.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 10.4x on those 2029 earnings, up from 9.7x today. This future PE is lower than the current PE for the GB Electronic industry at 13.7x.

- Analysts expect the number of shares outstanding to decline by 4.96% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.69%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The weak performance in EMEA and APAC regions, with a decline of 27% in EMEA and 8% in APAC, presents a risk, suggesting potential regional-specific challenges that could impact future revenue and earnings growth.

- The decline in sales of ClickShare, which was significant at 16%, indicates competition and market saturation, possibly affecting both top-line revenue and profit margins.

- The impact of restructuring costs, listed as consistent year-over-year, might continue if further restructuring is needed, affecting the net earnings due to these non-operational expenses.

- The reliance on positive inventory movements and nonrecurring items, like the sale and leaseback, to support cash flow and EBITDA indicates reliance on one-time boosts rather than sustainable operational improvements, thus potentially affecting the quality and recurrence of earnings.

- In the Entertainment division, external factors such as softer market conditions and reliance on a strong movie slate indicate vulnerability to market-driven conditions that are out of their control, which could lead to instability in revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of €12.25 for Barco based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €14.5, and the most bearish reporting a price target of just €9.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €1.1 billion, earnings will come to €106.6 million, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 8.7%.

- Given the current share price of €8.49, the analyst price target of €12.25 is 30.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Barco?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.