Key Takeaways

- Strategic expansion into new markets and high-value technology positions DUG for growth in revenue and improved market share in energy sectors.

- Innovations like multi-client assets and cooling technology suggest potential for diversified, high-margin revenue streams enhancing profitability and growth.

- Heavy reliance on oil and gas clients and rising costs may affect net margins, while investment in new tech and locations presents risks to cash flows.

Catalysts

About DUG Technology- Dug Technology Ltd, a technology company, provides hardware and software solutions for the technology and resource sectors in Australia, the United States, the United Kingdom, Malaysia, and the United Arab Emirates.

- Expansion into the Middle East and new markets such as India and Brazil provides DUG with increased opportunities for business development and project awards, likely boosting future revenue growth.

- Investment in Elastic Multi-parameter FWI technology and pilot projects, which are showing superior results, positions DUG to capture a larger share of the lucrative oil and gas production and exploration markets, potentially improving both revenue and margins.

- The transition to owning multi-client assets represents a strategic pivot that could yield high-margin, repeatable revenue, positively impacting net margins and profitability.

- Continued growth in software revenue, driven by strong customer renewals and new use cases in offshore wind and other sectors, is expected to accelerate, enhancing revenue growth and potentially improving net margins through higher-value software offerings.

- The global rollout of DUG Nomad and immersion cooling technology, coupled with BAC's new offerings, has the potential to open new revenue streams and diversify earnings, with long-term implications for both revenue and margin expansion.

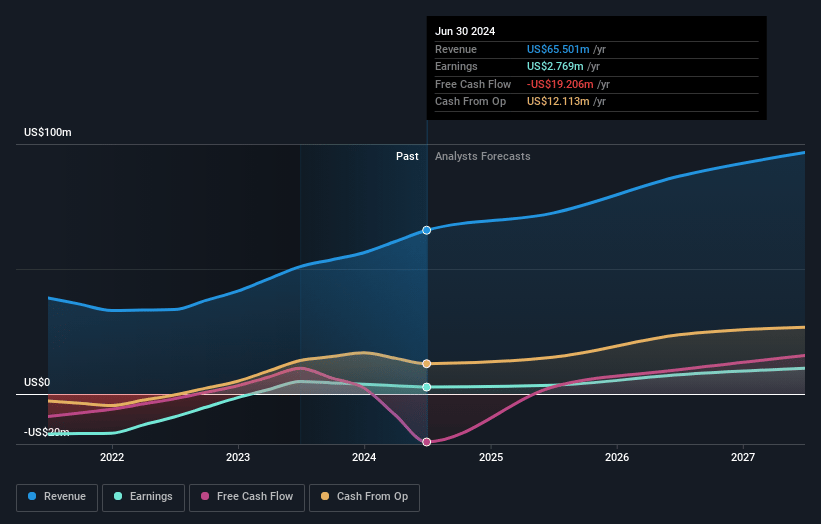

DUG Technology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DUG Technology's revenue will grow by 13.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -3.1% today to 12.8% in 3 years time.

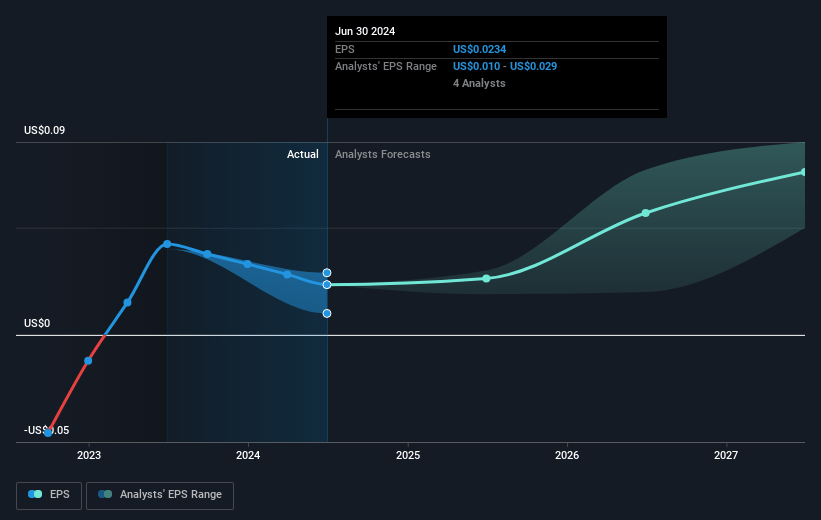

- Analysts expect earnings to reach $12.0 million (and earnings per share of $0.09) by about July 2028, up from $-2.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 26.8x on those 2028 earnings, up from -59.4x today. This future PE is lower than the current PE for the AU Software industry at 73.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.65%, as per the Simply Wall St company report.

DUG Technology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Despite the excitement about the technology, DUG's revenue was down 4%, and services revenue decreased by 3% in the first half, highlighting potential challenges in maintaining or growing future revenues.

- The HPC-as-a-Service revenue fell by 46%, which raises concerns about dependency on a narrow client base affecting earnings stability.

- Significant reliance on oil and gas clients, with the majority of revenue coming from this sector, may present a risk due to potential volatility and market fluctuations, potentially impacting net margins.

- The cost increase from employee benefits, particularly due to Middle East expansion, and other expenses related to restructuring, may squeeze net margins unless offset by growth in revenues.

- The company has significant investment in new technology and geographical expansion, which requires substantial capital and could impact future cash flows and earnings if these investments do not yield anticipated returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$2.324 for DUG Technology based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$2.96, and the most bearish reporting a price target of just A$1.91.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $93.7 million, earnings will come to $12.0 million, and it would be trading on a PE ratio of 26.8x, assuming you use a discount rate of 8.6%.

- Given the current share price of A$1.34, the analyst price target of A$2.32 is 42.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.