Key Takeaways

- Incitec Pivot's strategy to lead in global explosives aims to double earnings through advanced technology, affecting revenue and growth.

- Splitting the Fertilisers business and asset sales aim to optimize capital structure and boost shareholder returns.

- Gas price uncertainty, operational disruptions, capital expenditures, and strategic reviews pose significant financial risks and uncertainties to Incitec Pivot's revenue and profitability.

Catalysts

About Incitec Pivot- Manufactures and distributes industrial explosives, industrial chemicals, and fertilizers in Australia and the United State.

- Incitec Pivot's ambition to become the leading global explosives player includes plans to double earnings and deliver returns above the cost of capital, leveraging their unique competitive position and advanced technology. This is expected to impact revenue and earnings growth.

- The transformation program at IPL has already realized $64 million in EBIT improvements for fiscal year '24, with a goal to achieve a run rate equivalent to 40%-50% of the earnings uplift by the end of fiscal year '25, indicating potential for improved net margins and profitability.

- Strategies to expand margins through productivity enhancements, innovations, and reducing working capital are in place, aiming to improve net margins and overall earnings.

- Dyno Nobel Asia Pacific achieved record earnings and favorable recontracting, suggesting potential for sustained revenue growth and improved EBIT margins in future years.

- The separation of the Fertilisers business and the sale of real estate assets such as Gibson Island underscore potential capital returns and enhanced focus on high-return opportunities, directly impacting capital structure and shareholder returns.

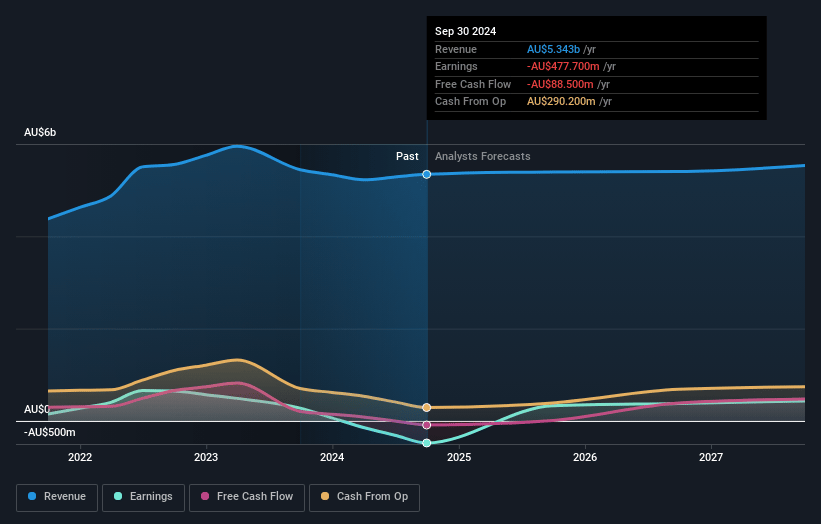

Incitec Pivot Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Incitec Pivot's revenue will grow by 1.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -8.9% today to 7.8% in 3 years time.

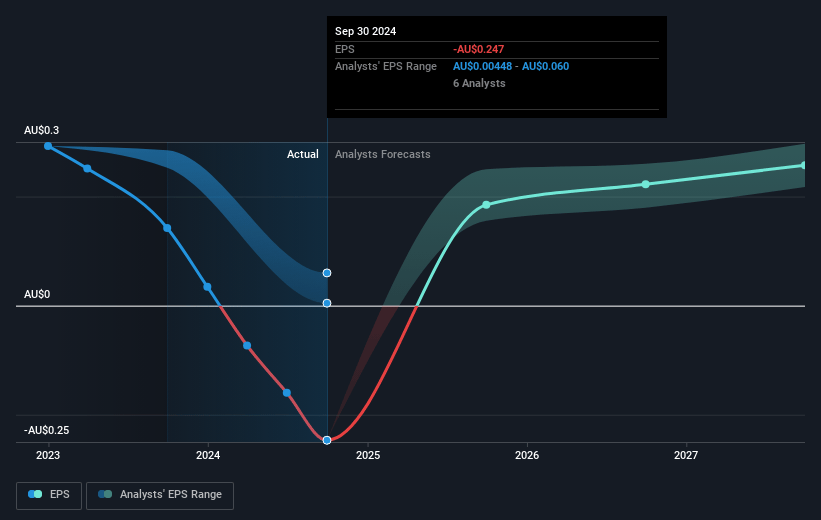

- Analysts expect earnings to reach A$430.2 million (and earnings per share of A$0.25) by about March 2028, up from A$-477.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$532.8 million in earnings, and the most bearish expecting A$386.2 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.4x on those 2028 earnings, up from -10.5x today. This future PE is lower than the current PE for the AU Chemicals industry at 20.1x.

- Analysts expect the number of shares outstanding to decline by 2.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.48%, as per the Simply Wall St company report.

Incitec Pivot Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Gas price uncertainty in Australia, particularly impacting Phosphate Hill, adds cost unpredictability and affects net margins, potentially leading to financial losses as seen with the $311 million after-tax statutory loss primarily due to noncash impairments.

- The strategic review and potential closure or sale of manufacturing facilities such as Geelong and issues in supply at Phosphate Hill highlight exposure to operational disruptions that can significantly impact earnings and return on capital.

- Planned capital expenditures and turnarounds at Moranbah, Cheyenne, and LOMO are likely to lead to short-term financial strain, affecting cash flow and operational stability, which may not immediately contribute positively to earnings until fully realized.

- Market conditions such as declining coal volumes due to low natural gas prices and slowness in construction and quarrying sectors may impact revenue growth in the Dyno Nobel Americas segment more than anticipated.

- The risks linked with the separation and strategic review of the Fertilisers business, including potential asset write-downs and restructuring charges, introduce heightened financial risks and uncertainty to future revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$3.302 for Incitec Pivot based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$3.9, and the most bearish reporting a price target of just A$2.9.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$5.5 billion, earnings will come to A$430.2 million, and it would be trading on a PE ratio of 16.4x, assuming you use a discount rate of 7.5%.

- Given the current share price of A$2.69, the analyst price target of A$3.3 is 18.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.