Key Takeaways

- Strategic exploration and potential restructuring could improve operational efficiency, cost management, and net margins amid nbn contract loss.

- Strong cash flow, no net debt, and recurring contracts in expanding markets position BSA for growth, enhancing revenue streams and earnings potential.

- Loss of key contracts and reliance on a few major agreements threatens revenue stability, necessitating costly restructuring to address concentration risk and financial uncertainty.

Catalysts

About BSA- Offers communications and utilities infrastructure, and property solutions in Australia.

- BSA is exploring strategic options and potential restructuring in response to the expected loss of the nbn Field Services contract, which could result in improved operational efficiency and cost management, positively impacting net margins.

- The company has shown significant improvements in financial performance, with increased EBITDA and improved cash flows driven by operational efficiency and margin mix, suggesting the potential for favorable earnings growth.

- Despite the nbn contract uncertainty, BSA maintains a strong balance sheet with positive cash flow and no net debt, which provides flexibility for future investments and growth initiatives, potentially benefiting net margins and earnings.

- BSA continues to service recurring contracts in smart metering, electric vehicle services, and Foxtel platforms, which contribute stable revenues and offer growth potential in rapidly expanding markets, potentially enhancing future revenue streams.

- The company is focused on optimizing working capital management and reducing dependency on discontinued operations, which could lead to improved operational cash flows and overall financial stability, positively impacting net margins and earnings.

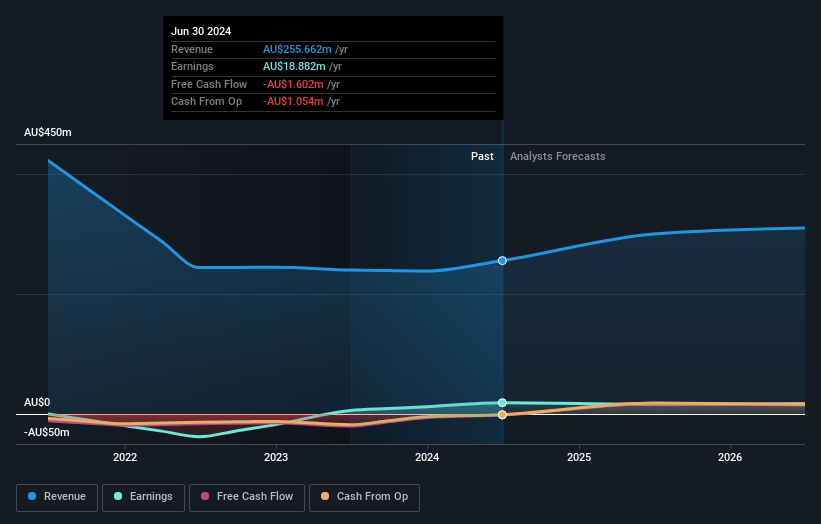

BSA Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BSA's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 6.7% today to 4.4% in 3 years time.

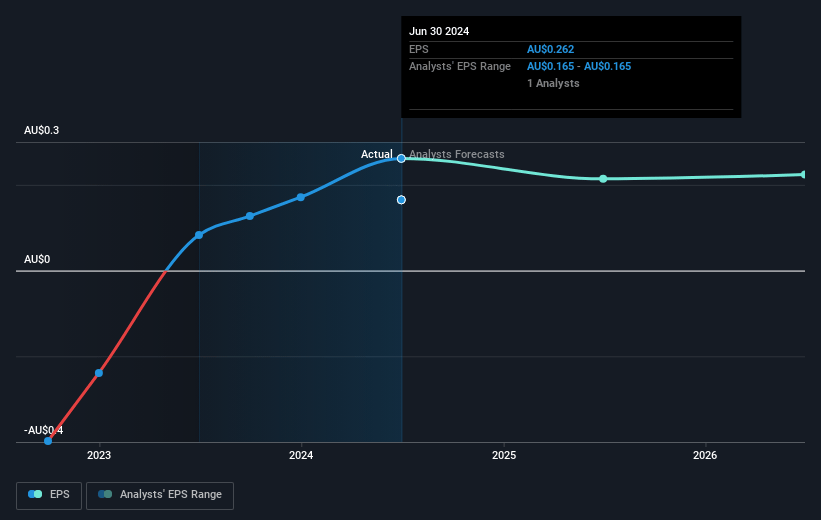

- Analysts expect earnings to reach A$14.9 million (and earnings per share of A$0.19) by about April 2028, down from A$19.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.0x on those 2028 earnings, up from 0.2x today. This future PE is lower than the current PE for the AU Construction industry at 15.5x.

- Analysts expect the number of shares outstanding to grow by 3.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.26%, as per the Simply Wall St company report.

BSA Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Loss of the nbn Field Services contract, which contributes approximately 83% of BSA's revenue, poses a significant risk to future revenue streams and financial stability.

- The uncertainty surrounding the transition arrangements with nbn could disrupt operations and lead to unpredictable revenue, impacting overall earnings and margins.

- The need for a significant restructuring to rightsize the company may incur additional costs and operational disruption, affecting net margins and profitability.

- Heavy reliance on a small number of key contracts, like the nbn Unified contract, exposes the company to customer concentration risk, which could impact revenue consistency and financial resilience if future contracts are not secured.

- Potential variability in client volumes, especially with the uncertainty of nbn arrangements, introduces risk to projected run rates and revenue forecasts, potentially impacting financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$1.85 for BSA based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$341.2 million, earnings will come to A$14.9 million, and it would be trading on a PE ratio of 13.0x, assuming you use a discount rate of 8.3%.

- Given the current share price of A$0.05, the analyst price target of A$1.85 is 97.4% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.