Key Takeaways

- Stricter decarbonization policies and rapid renewable adoption threaten core fossil-fuel and centralized power businesses, increasing long-term risk and pressuring revenue stability.

- Portfolio concentration, cost inflation, and higher capital expenses expose earnings to volatility, constraining growth, margins, and the ability to diversify revenue streams.

- Stable, regulated core business, international diversification, and strategic investments in energy infrastructure and renewables support resilient growth, steady earnings, and long-term shareholder returns.

Catalysts

About Abu Dhabi National Energy Company PJSC- Operates as an integrated utility company in the United Arab Emirates, North America, Europe, Africa, and internationally.

- Intensifying global decarbonization policies and carbon pricing, particularly in key export markets, threaten to erode demand for TAQA's traditional, fossil-fuel-powered generation assets and upstream Oil & Gas operations; this increases the long-term risk of asset impairment and constrains future revenue growth and profitability.

- The rapid adoption of distributed renewable energy technologies such as solar, wind, and battery storage-both at the utility and consumer level-reduces reliance on centralized power transmission and generation models, directly undermining TAQA's core business segments and placing long-term pressure on top-line revenues and grid utilization.

- Prolonged periods of elevated global interest rates and higher capital costs directly inflate project financing expenses for infrastructure expansion and renewable energy investments, which threatens to compress net margins and limit TAQA's ability to pursue earnings-accretive growth despite its current balance sheet stability.

- The company's portfolio remains heavily exposed to volatile Oil & Gas markets and geographic concentration in the UAE and select international markets, making long-term earnings vulnerable to regulatory shifts, energy transition risk, and regional policy or macroeconomic shocks, which heightens potential earnings volatility and weakens revenue diversification.

- Ongoing cost inflation for fuel, labor, and equipment in regulated utility businesses, combined with regulatory and consumer resistance to tariff increases, will likely suppress net margin expansion and diminish future free cash flow, further exacerbated by rising operational expenditure linked to maintaining and upgrading aging infrastructure in the face of climate variability and water scarcity challenges.

Abu Dhabi National Energy Company PJSC Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Abu Dhabi National Energy Company PJSC compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

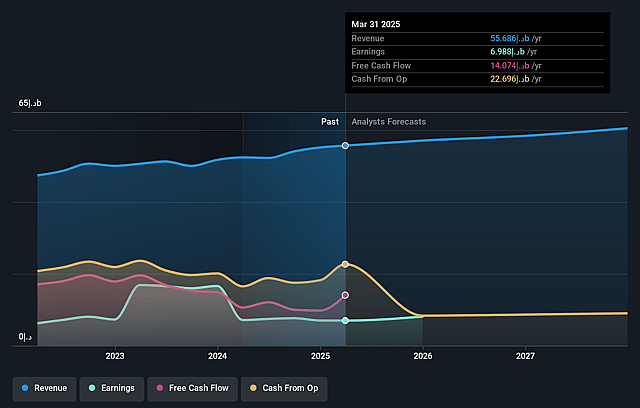

- The bearish analysts are assuming Abu Dhabi National Energy Company PJSC's revenue will grow by 3.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 12.5% today to 15.1% in 3 years time.

- The bearish analysts expect earnings to reach AED 9.3 billion (and earnings per share of AED 0.08) by about July 2028, up from AED 7.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 33.5x on those 2028 earnings, down from 52.8x today. This future PE is lower than the current PE for the AE Integrated Utilities industry at 38.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 18.81%, as per the Simply Wall St company report.

Abu Dhabi National Energy Company PJSC Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company derives approximately 90% of its revenues from contracted and regulated businesses, which provides stability and predictability even during periods of macroeconomic uncertainty, supporting the long-term stability of revenue and net income.

- Continued investments and growth in regulated Transmission & Distribution and Water Solutions have resulted in rising revenues and resilient operating performance, positioning the company to benefit from increasing regional demand for reliable power and water driven by urbanization and population growth, which can support revenue and earnings growth over time.

- The company is strategically investing in new network construction and upgrades, as well as supporting the UAE's AI Strategy 2031, which is expected to generate significant incremental demand for electricity and associated infrastructure, translating to potential sustained long-term growth in revenue and margins.

- Recent offshore transmission acquisition in the UK and the expansion of renewable energy activities through its Masdar subsidiary provide exposure to international markets and diversification, enhancing the company's ability to capitalize on the global shift toward renewables and regulated transmission, with positive implications for long-term revenue and free cash flow.

- A strong balance sheet featuring ample liquidity, controlled leverage, and favorable locked-in debt costs allows the company to pursue large-scale, earnings-accretive growth projects and maintain steady dividend payments, directly supporting stable earnings and return on equity into the future.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Abu Dhabi National Energy Company PJSC is AED1.65, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Abu Dhabi National Energy Company PJSC's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of AED3.14, and the most bearish reporting a price target of just AED1.65.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be AED61.4 billion, earnings will come to AED9.3 billion, and it would be trading on a PE ratio of 33.5x, assuming you use a discount rate of 18.8%.

- Given the current share price of AED3.28, the bearish analyst price target of AED1.65 is 98.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.