Narratives are currently in beta

Key Takeaways

- Expansion into new markets and strategic acquisitions are projected to enhance revenue and market presence, driving organic and inorganic growth.

- Investment in digital technologies and focus on wealth management are expected to improve efficiencies, increase margins, and drive revenue growth.

- Falling interest rates, higher costs, and tax hikes could pressure Emirates NBD’s earnings, while varying market environments pose balance sheet risks.

Catalysts

About Emirates NBD Bank PJSC- Provides corporate, institutional, retail, treasury, and Islamic banking services.

- Expansion into new markets such as Saudi Arabia and ongoing international growth initiatives are likely to enhance revenue by increasing market share and customer base.

- Investment in digital, advanced analytics, and AI technologies is expected to improve efficiencies and enhance customer service, potentially increasing net margins through better cost management.

- Continued focus on developing the wealth management business is anticipated to drive revenue growth, particularly as affluent customer segments expand within existing markets.

- Strategic plans for acquisitions in key markets aim to increase market presence and could lead to upward earnings growth through organic and inorganic expansion.

- The robust economic outlook for the UAE and other regional markets is projected to sustain high single-digit loan growth, potentially offsetting margin pressure from expected interest rate cuts and thereby supporting revenue stability.

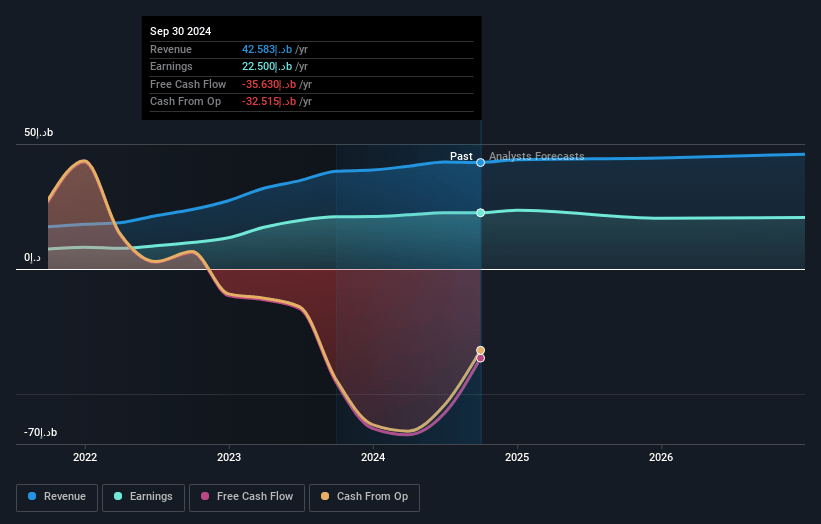

Emirates NBD Bank PJSC Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Emirates NBD Bank PJSC's revenue will grow by 3.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 52.8% today to 41.5% in 3 years time.

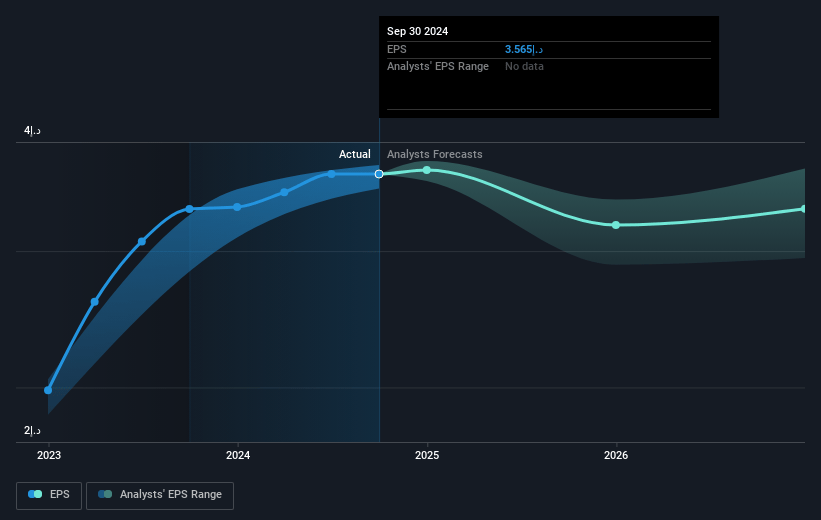

- Analysts expect earnings to reach AED 19.3 billion (and earnings per share of AED 3.05) by about January 2028, down from AED 22.5 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as AED23.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.1x on those 2028 earnings, up from 5.8x today. This future PE is greater than the current PE for the AE Banks industry at 8.7x.

- Analysts expect the number of shares outstanding to grow by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 19.94%, as per the Simply Wall St company report.

Emirates NBD Bank PJSC Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The potential impact of falling interest rates on net interest margins could pressure revenue growth, as lower rates might not be fully offset by asset growth. This could impact both net margins and overall earnings.

- DenizBank’s variable nonclient income and higher swap funding costs could lead to volatility, impacting nonfunded income and ultimately reducing total earnings.

- Rising costs attributed to inflation and accelerated depreciation on IT systems suggest an increasing cost-income ratio, which could squeeze net margins if not managed effectively.

- Additional corporate tax obligations in the UAE are expected to increase from 9% to 15%, potentially reducing net profits and impacting overall earnings.

- The UAE and Turkey's varying interest rate environments could introduce balance sheet risks, potentially requiring adjustments in asset-liability management and impacting revenues.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of AED24.89 for Emirates NBD Bank PJSC based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of AED28.5, and the most bearish reporting a price target of just AED20.2.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be AED46.5 billion, earnings will come to AED19.3 billion, and it would be trading on a PE ratio of 14.1x, assuming you use a discount rate of 19.9%.

- Given the current share price of AED20.5, the analyst's price target of AED24.89 is 17.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives