Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:EGLE

Analysts Just Made A Captivating Upgrade To Their Eagle Bulk Shipping Inc. (NASDAQ:EGLE) Forecasts

Eagle Bulk Shipping Inc. (NASDAQ:EGLE) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects. Could this be enough to reverse the market's pessimism for Eagle Bulk Shipping? Shares are down 4.8% to US$63.15 in the last 7 days.

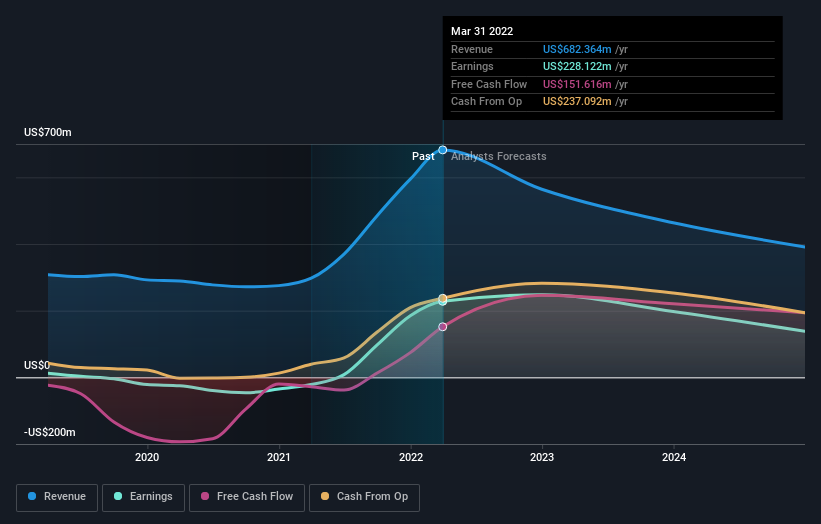

After the upgrade, the consensus from Eagle Bulk Shipping's six analysts is for revenues of US$564m in 2022, which would reflect a considerable 17% decline in sales compared to the last year of performance. Per-share earnings are expected to rise 2.5% to US$17.07. Prior to this update, the analysts had been forecasting revenues of US$500m and earnings per share (EPS) of US$16.59 in 2022. The forecasts seem more optimistic now, with a nice gain to revenue and a small lift in earnings per share estimates.

View our latest analysis for Eagle Bulk Shipping

With these upgrades, we're not surprised to see that the analysts have lifted their price target 6.8% to US$76.00 per share. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Eagle Bulk Shipping analyst has a price target of US$90.00 per share, while the most pessimistic values it at US$50.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 22% annualised revenue decline to the end of 2022. That is a notable change from historical growth of 20% over the last five years. Yet aggregate analyst estimates for other companies in the industry suggest that industry revenues are forecast to decline 5.3% per year. So it's pretty clear that Eagle Bulk Shipping's revenues are expected to shrink faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Notably, analysts also upgraded their revenue estimates, with sales performing well although Eagle Bulk Shipping's revenue growth is expected to trail that of the wider market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, Eagle Bulk Shipping could be worth investigating further.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 6 potential risks with Eagle Bulk Shipping, including a weak balance sheet. You can learn more, and discover the 5 other risks we've identified, for free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

Valuation is complex, but we're here to simplify it.

Discover if Eagle Bulk Shipping might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:EGLE

Eagle Bulk Shipping

Eagle Bulk Shipping Inc. engages in the ocean transportation of dry bulk cargoes worldwide.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor