American Airlines Group (AAL) shares have seen some movement over the past month, gaining around 13%. Investors are taking stock of recent performance and considering how broader airline trends might shape the months ahead.

While American Airlines Group’s 13% share price return over the past month is impressive, the bigger story is its continued recovery from a rocky start to the year. Long-term momentum, however, remains mixed. A 1-year total shareholder return of -3.5% and a 5-year figure of 12% remind investors that progress still comes in fits and starts.

If the market’s shifting sentiment around travel stocks has you reassessing your own strategy, this could be the perfect moment to discover See the full list for free.

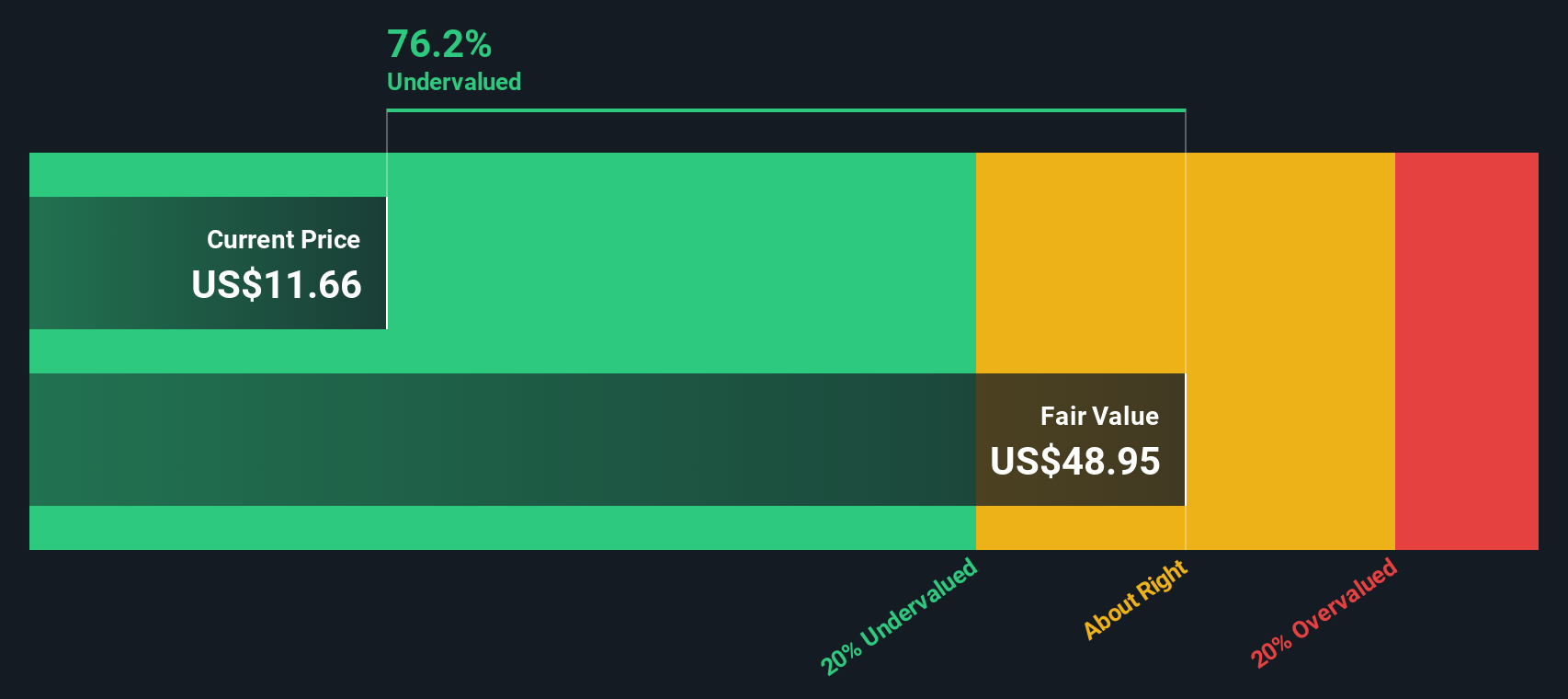

That leaves a critical question for investors today: Is American Airlines stock undervalued after its recent rebound, or has the market already priced in every bit of its potential recovery and future growth?

Advertisement

Most Popular Narrative: 23.9% Overvalued

According to PittTheYounger, the most-followed narrative sets a fair value for American Airlines at $10.61, noticeably below the stock’s recent close of $13.15. This signals that the current rally might be getting ahead of the company’s true potential, especially when weighed against fundamental financial concerns.

There’s a single reason why American is the least attractive of US legacy carriers (in terms of investing, anyway): its balance sheet. If most airlines and certainly those in the US are loaded up to the hilt with debt, American goes so far as to boast negative equity. Any startup would go belly-up with a balance sheet such as this one. Now, you can survive and even generate decent returns with a precarious capital structure, but of course you’re super-sensitive to any shock on the demand side of your business, hitting both revenues and margins. That is where the clouds gather on American.

Curious about why this valuation feels so harsh? The narrative’s conclusion pivots on bold assumptions around profit margins and future market dynamics, yet leaves some numbers just out of reach. The real twist is how one specific financial metric makes or breaks the case for American’s long-term upside. Ready to uncover exactly which lever, if pulled, could change the story for good?

However, if refinancing conditions improve or if American successfully boosts yields with its Premium Economy strategy, the narrative could quickly shift in their favor.

Another View: Discounted Cash Flow Model Points to Undervaluation

Looking at American Airlines through the lens of our DCF model, the story shifts. This method estimates a fair value of $23.15 per share, which is significantly higher than the current price of $13.15. According to this approach, the market might be underestimating the company’s long-term potential.

If you think there’s another side to this story or want to dig into the details yourself, you can shape your own perspective in just a few minutes. Do it your way

A great starting point for your American Airlines Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let your next investing breakthrough slip away. See what else is out there by checking these handpicked opportunities tailored to different strategies and goals:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks