Keysight Technologies (NYSE:KEYS) Powers AMD's Next-Gen CPU Testing With PCIe 6.0 Integration

Keysight Technologies (NYSE:KEYS) recently collaborated with AMD to advance PCI Express 6.0 technology, marking a significant step in high-speed data transfer and AI application development. Over the past quarter, the company experienced a 3% stock price increase, aligning closely with the market's modest gains. While the market has shown a 10% rise this year and anticipates 15% annual earnings growth, Keysight's performance was supported by its strong Q2 earnings and share buyback activities. These elements collectively reinforced the company's positive trajectory amid the broader market context, with no standout divergences from overall trends.

Rare earth metals are the new gold rush. Find out which 24 stocks are leading the charge.

The collaboration between Keysight Technologies and AMD on PCI Express 6.0 technology could bolster revenue and earnings forecasts by enhancing the company's product offerings in high-speed data transfer and AI applications. This alignment with industry advancements is expected to strengthen Keysight's market position, potentially driving further growth in their software-centric and recurring revenue streams. As a result, this partnership may enhance the company's attractiveness to investors and improve its competitive edge in the evolving tech landscape.

Over the past five years, Keysight Technologies achieved a total return of 58.19%, reflecting consistent performance and resilience in a competitive market. This long-term gain provides context for the company's overall stock trajectory, supported by its strategic initiatives and diverse product portfolio. In contrast, during the past year, Keysight's return has outpaced the US Market, which generated a 9.8% rise, underscoring its robust positioning relative to industry peers.

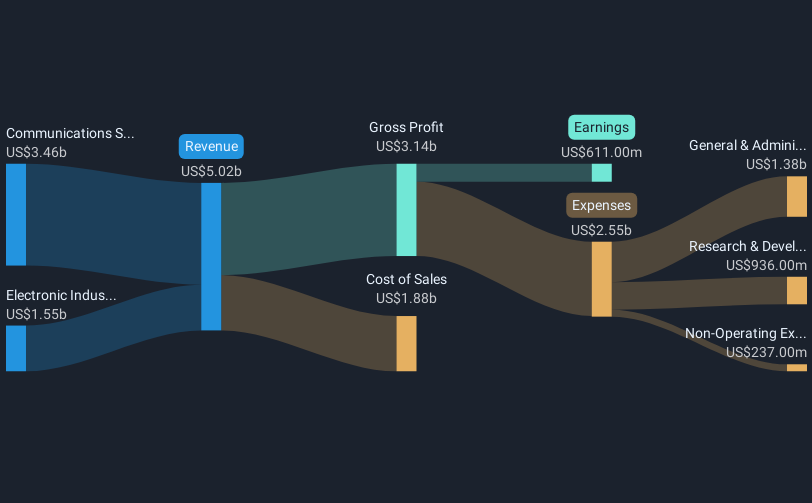

The recent news could position Keysight to capitalize on growing demand in AI and data centers, potentially enhancing its revenue growth from the current 6% annual forecast. Moreover, aided by strategic acquisitions and collaboration, Keysight may experience improved margins and earnings stability. While its current share price of US$163.61 remains roughly 10.8% below the analyst consensus target of US$183.44, the emerging technology synergies may contribute positively towards closing this valuation gap. These developments could affirm analyst expectations if Keysight continues leveraging high-growth areas and optimizing its product mix.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keysight Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KEYS

Keysight Technologies

Provides electronic design and test solutions worldwide.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

An Undervalued 3.3Moz Gold Project in Canada

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Recently Updated Narratives

Strong DAU drives Ads and AI Data narrative

Silver X Has 152 Million Ounces, Already Producing and Its Biggest Growth Phase May Still Be Ahead

Cochlear’s Crossroads: Temporary Setback or Structural Shift?

Popular Narratives

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

NVIDIA will see a profit margin surge of 55% in the next 5 years