- Japan

- /

- Medical Equipment

- /

- TSE:7741

3 Undervalued Stocks Trading At Up To 34.4% Below Intrinsic Value

Reviewed by Simply Wall St

Amid a cooling U.S. labor market and significant economic data releases, global markets have experienced notable volatility, with major indices such as the S&P 500 and Nasdaq Composite pulling back sharply. This environment of heightened uncertainty presents an opportunity to identify undervalued stocks that are trading significantly below their intrinsic value. In this context, a good stock is one that demonstrates strong fundamentals and potential for growth despite broader market challenges. Here are three stocks currently trading up to 34.4% below their intrinsic value, offering potential opportunities for investors seeking value in uncertain times.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | US$16.68 | US$33.25 | 49.8% |

| Elders (ASX:ELD) | A$9.08 | A$18.11 | 49.9% |

| Members (TSE:2130) | ¥712.00 | ¥1416.24 | 49.7% |

| SMRT Holdings Berhad (KLSE:SMRT) | MYR1.03 | MYR2.06 | 49.9% |

| Bowhead Specialty Holdings (NYSE:BOW) | US$26.98 | US$53.76 | 49.8% |

| Green Thumb Industries (CNSX:GTII) | CA$15.46 | CA$30.83 | 49.9% |

| Seatrium (SGX:5E2) | SGD1.42 | SGD2.83 | 49.8% |

| SK Biopharmaceuticals (KOSE:A326030) | ₩85300.00 | ₩170336.89 | 49.9% |

| Sandfire Resources (ASX:SFR) | A$8.31 | A$16.55 | 49.8% |

| Paratus Energy Services (OB:PLSV) | NOK54.68 | NOK109.01 | 49.8% |

Here we highlight a subset of our preferred stocks from the screener.

Li Auto (NasdaqGS:LI)

Overview: Li Auto Inc. operates in the energy vehicle market in the People’s Republic of China and has a market cap of $20.01 billion.

Operations: The company generates revenue of CN¥130.70 billion from its Auto Manufacturers segment.

Estimated Discount To Fair Value: 34.4%

Li Auto's recent sales surge, with a record 51,000 vehicles delivered in July 2024 and cumulative deliveries reaching 873,345, highlights its strong market position. Despite legal challenges and past shareholder dilution, Li Auto is trading at US$18.94—34.4% below its estimated fair value of US$28.87—indicating significant undervaluation based on discounted cash flow analysis. Forecasts suggest robust revenue growth of 20.1% annually and earnings growth of 20.8%, outpacing the broader market expectations.

- Insights from our recent growth report point to a promising forecast for Li Auto's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Li Auto.

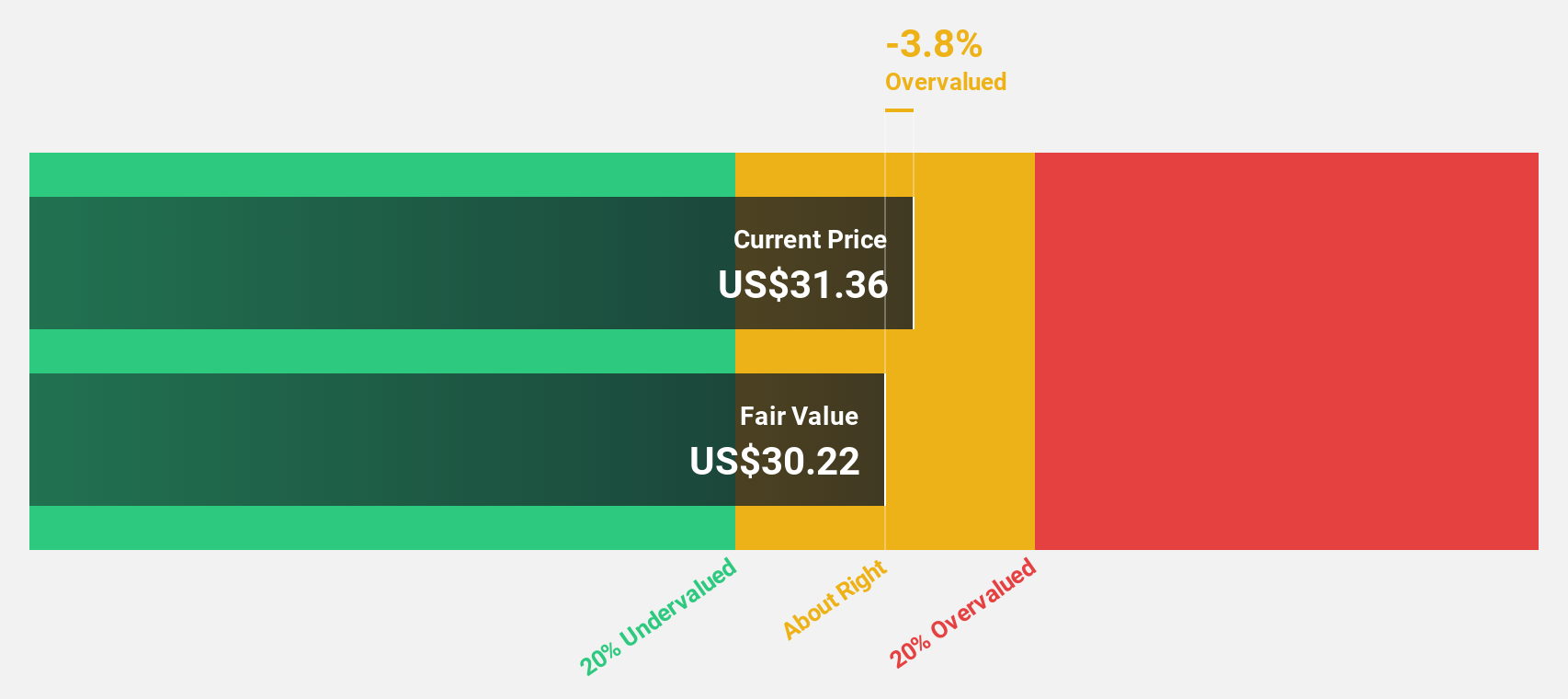

Corning (NYSE:GLW)

Overview: Corning Incorporated operates in the display technologies, optical communications, environmental technologies, specialty materials, and life sciences sectors globally and has a market cap of $32.31 billion.

Operations: The company's revenue segments include Optical Communications ($3.86 billion), Display Technologies ($3.73 billion), Specialty Materials ($1.99 billion), Environmental Technologies ($1.76 billion), and Life Sciences ($957 million).

Estimated Discount To Fair Value: 27.3%

Corning is trading at US$38.33, 27.3% below its estimated fair value of US$52.71 based on discounted cash flow analysis, indicating significant undervaluation. Despite high debt levels and a dividend yield of 2.92% not well covered by earnings or free cash flows, the company forecasts robust annual earnings growth of 28%, driven by new optical connectivity products for generative AI in Optical Communications, offsetting other market slowdowns.

- Our growth report here indicates Corning may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of Corning stock in this financial health report.

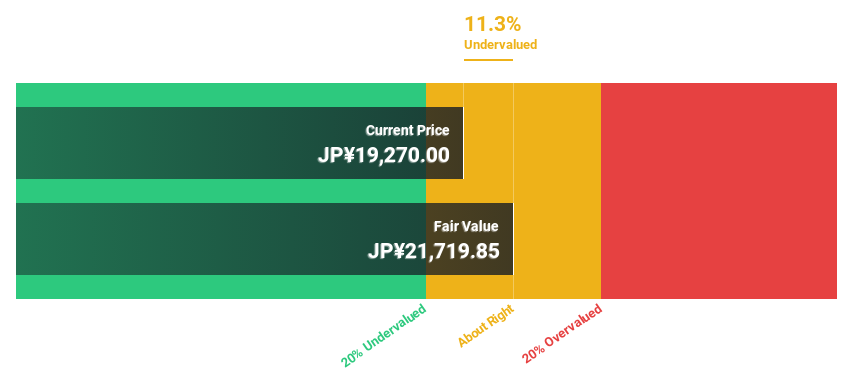

HOYA (TSE:7741)

Overview: HOYA Corporation, with a market cap of ¥6.52 trillion, is a med-tech company that provides high-tech and medical products worldwide.

Operations: HOYA Corporation's revenue segments include Life Care at ¥537.56 billion and Telecommunications at ¥253.04 billion.

Estimated Discount To Fair Value: 12.3%

HOYA is trading at ¥19,235, 12.3% below its estimated fair value of ¥21,935.15 based on discounted cash flow analysis, indicating undervaluation. Recent FDA clearance for a new sterilization cycle in collaboration with ASP could boost revenue growth and enhance market position. Additionally, HOYA's earnings are forecast to grow 11.29% annually, outpacing the Japanese market average of 8.9%. The company’s ongoing share buyback program further supports shareholder value enhancement strategies.

- The analysis detailed in our HOYA growth report hints at robust future financial performance.

- Navigate through the intricacies of HOYA with our comprehensive financial health report here.

Next Steps

- Access the full spectrum of 897 Undervalued Stocks Based On Cash Flows by clicking on this link.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HOYA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7741

HOYA

A med-tech company, provides high-tech and medical products worldwide.

Flawless balance sheet with solid track record.