Advertisement

Did Benchmark's (BHE) Q3 Beat and Sector Gains Signal a New Growth Chapter?

Simply Wall St

Reviewed by Sasha Jovanovic

- Benchmark Electronics announced third-quarter 2025 earnings, reporting US$680.68 million in sales and double-digit sector gains, with strong performance in the Medical and Aerospace & Defense segments, while also confirming a leadership transition effective March 2026.

- Restructuring initiatives, facility closures, and capacity expansions, especially in precision machining, highlight Benchmark’s continued focus on operational efficiency and growth opportunities across key end-markets.

- We'll examine how Benchmark's revenue beat and expansion investments in Q3 2025 influence the company's investment narrative and future outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Benchmark Electronics Investment Narrative Recap

For investors considering Benchmark Electronics, the key thesis rests on the company's ability to capitalize on sector momentum in Medical and Aerospace & Defense while balancing operational improvements and expansion in precision machining. The recent Q3 2025 report, posting a revenue beat and confirming ongoing restructuring, primarily reinforces short-term confidence on growth in these end-markets; it does not materially alter the most significant short-term catalyst, which remains new high-performance computing (HPC) and AI-related wins, or the primary risk around continued weakness in the semiconductor capital equipment sector.

Among recent company updates, the Q4 2025 earnings guidance stands out as most relevant, as it aligns closely with analyst expectations while pointing to steady revenue between US$670 million and US$720 million and diluted GAAP EPS guidance of US$0.44 to US$0.50. This steadiness supports the near-term catalyst of expected revenue growth from ongoing sector strength, but does not lessen exposure to sector-specific volatility and macroeconomic headwinds.

On the flip side, investors should be aware that ongoing weakness in the semiconductor capital equipment sector remains a risk that could...

Read the full narrative on Benchmark Electronics (it's free!)

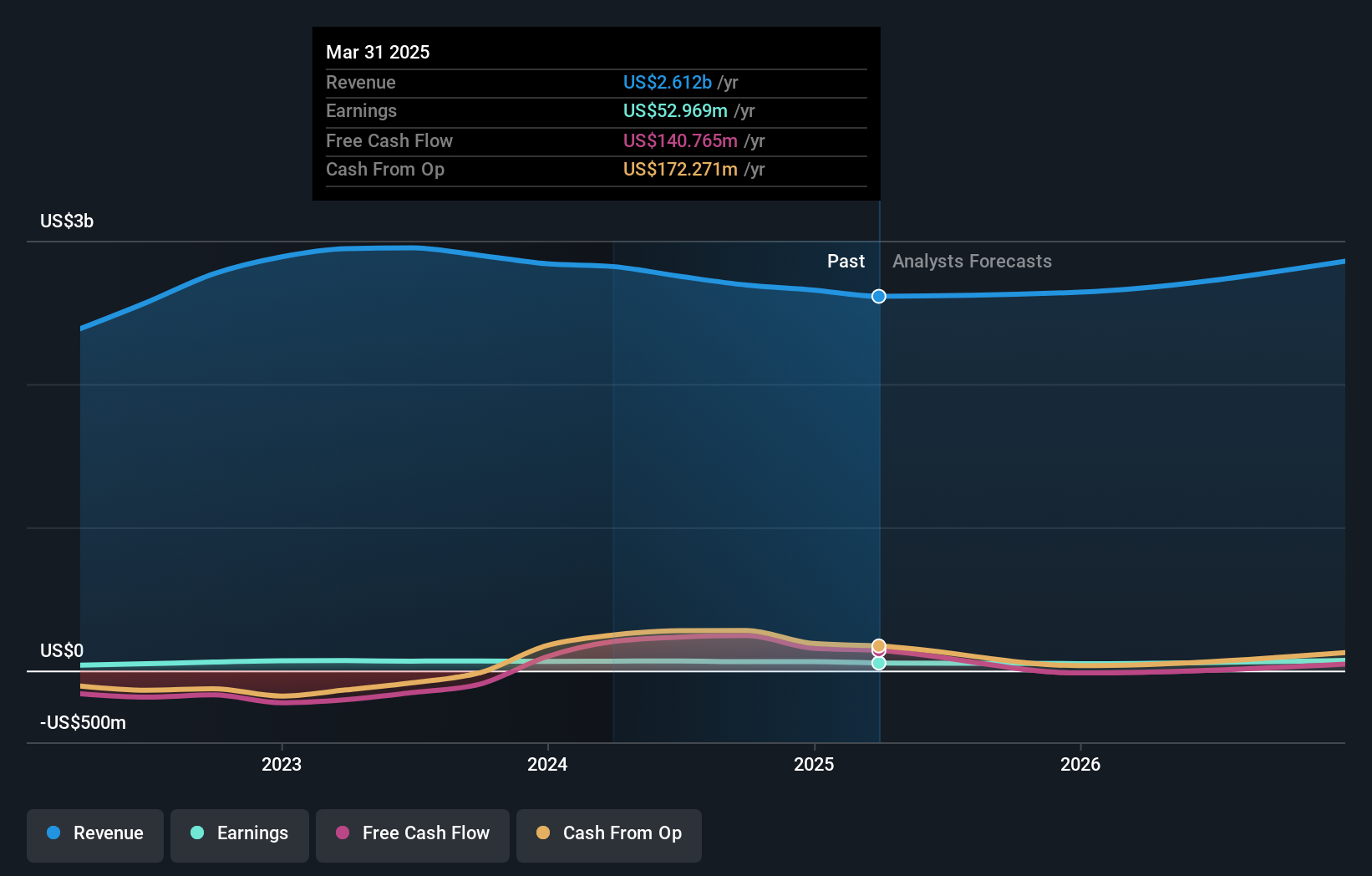

Benchmark Electronics is projected to reach $3.0 billion in revenue and $95.5 million in earnings by 2028. This outlook assumes a 5.3% annual revenue growth rate and an increase in earnings of $57.1 million from the current $38.4 million.

Uncover how Benchmark Electronics' forecasts yield a $47.33 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community range from US$10.36 to US$47.33 per share. Some readers highlight emerging growth opportunities in AI-driven HPC projects, which could reshape expectations for future performance.

Explore 3 other fair value estimates on Benchmark Electronics - why the stock might be worth less than half the current price!

Build Your Own Benchmark Electronics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Benchmark Electronics research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Benchmark Electronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Benchmark Electronics' overall financial health at a glance.

No Opportunity In Benchmark Electronics?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Benchmark Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BHE

Benchmark Electronics

Offers product design, engineering services, technology solutions, and manufacturing services in the Americas, Asia, and Europe.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor