Benchmark Electronics (BHE) shares slipped about 3% after a recent stretch of declines. The move has caught investors’ attention, especially with the stock now down 12% over the past year and almost 18% year to date.

After sliding 3% today, Benchmark Electronics is extending its losing streak and momentum seems to be fading. The company’s 1-year total shareholder return is negative, despite its impressive 3- and 5-year total returns of 56% and 95%. This hints at solid long-term potential even as near-term sentiment cools.

With shares trading below analyst price targets and strong long-term growth in mind, it raises the question: Is Benchmark Electronics currently undervalued, or is the market already factoring in all its future potential?

Advertisement

Most Popular Narrative: 16.4% Undervalued

Benchmark Electronics closed at $37.36, yet the most popular narrative values the shares noticeably higher. This difference is fueling new debate, especially with analyst expectations pointing up while the stock drifts lower in the short term.

Benchmark is positioned to benefit from the surging demand for advanced computing and AI infrastructure, as evidenced by recent contract wins in water-cooling for high-performance computing and AI data centers, and ramping opportunities expected to drive a return to revenue growth in AC&C by late 2025 and into 2026. This supports both revenue acceleration and an upward mix in gross margin due to the complexity of these projects.

What makes the current valuation so compelling? The narrative hinges on surging AI and tech opportunities, but also leans on tightly managed costs and ambitious earnings targets. Just what kind of profit leap is being projected? Big assumptions are built in. See what’s driving this surprising price target.

However, ongoing softness in the semi-cap sector or renewed supply chain challenges could stall the anticipated recovery and place pressure on revenue growth.

Another View: Is the Market Overlooking Key Risks?

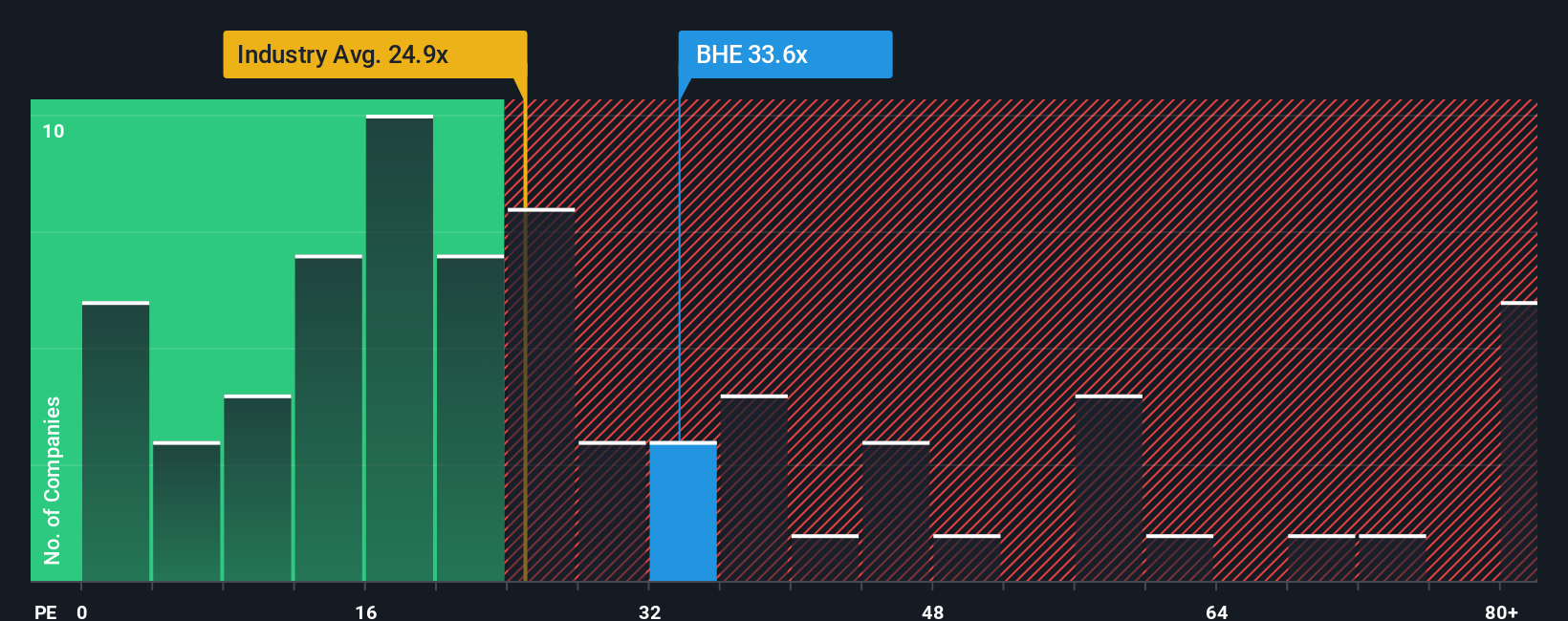

While the analyst-based fair value puts Benchmark Electronics in undervalued territory, a closer look at its price-to-earnings ratio tells a different story. At 34.9x, it is noticeably higher than both the industry average (25.2x) and peer average (26.9x), which could signal elevated valuation risk if growth fails to accelerate. The fair ratio stands at 40.4x, suggesting room for further market adjustment. Could investors be too optimistic, or is the company justifiably commanding a premium?

If you see things differently, or want to test your own ideas against the data, you can quickly shape your own perspective using available tools such as Do it your way.

A great starting point for your Benchmark Electronics research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Stay ahead of the curve and unlock tomorrow’s opportunities by tapping into these handpicked investment screens. Don’t risk missing the next big mover in the market.

Capitalize on the future of medicine by reviewing these 32 healthcare AI stocks, where innovation in AI is transforming healthcare outcomes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Benchmark Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.