Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:PLUS

Is ePlus’ Stronger FY26 Outlook And M&A Focus Altering The Investment Case For PLUS?

Reviewed by Sasha Jovanovic

- In early February 2026, ePlus inc. reported third-quarter fiscal 2026 results showing higher revenue and earnings, raised full-year 2026 net sales guidance to 20%–22% year-over-year growth from mid-teens, confirmed a US$0.25 quarterly dividend, updated on recent share buybacks, and reiterated its acquisition plans to expand solutions and geographic reach.

- A distinctive angle for investors is how ePlus is combining stronger earnings and upgraded guidance with capital returns and a stated focus on acquisitions in higher-growth solution areas and workplace transformation.

- With that backdrop, we'll explore how the upgraded full-year guidance and emphasis on acquisitions could reshape ePlus's existing investment narrative.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

ePlus Investment Narrative Recap

To own ePlus, you need to believe it can turn IT spending on AI, security and workplace transformation into durable, profitable growth while managing lumpier project revenue and margin pressure. The latest earnings beat and higher full-year net sales guidance reinforce the current growth story, but they do not remove the key near term risk that large deals and concentrated vertical exposure could still make results volatile from quarter to quarter.

Among the new disclosures, the upgraded outlook for 20% to 22% net sales growth versus fiscal 2025’s US$2.01 billion feels most relevant, because it directly ties into the main catalyst of expanding higher value IT solutions and services. It gives investors a clearer near term yardstick for how well ePlus is converting its acquisitions, AI and security focus, and workplace transformation push into top line momentum.

Yet against this stronger guidance, investors still need to weigh the risk that revenue driven by a few large enterprise and SLED projects could...

Read the full narrative on ePlus (it's free!)

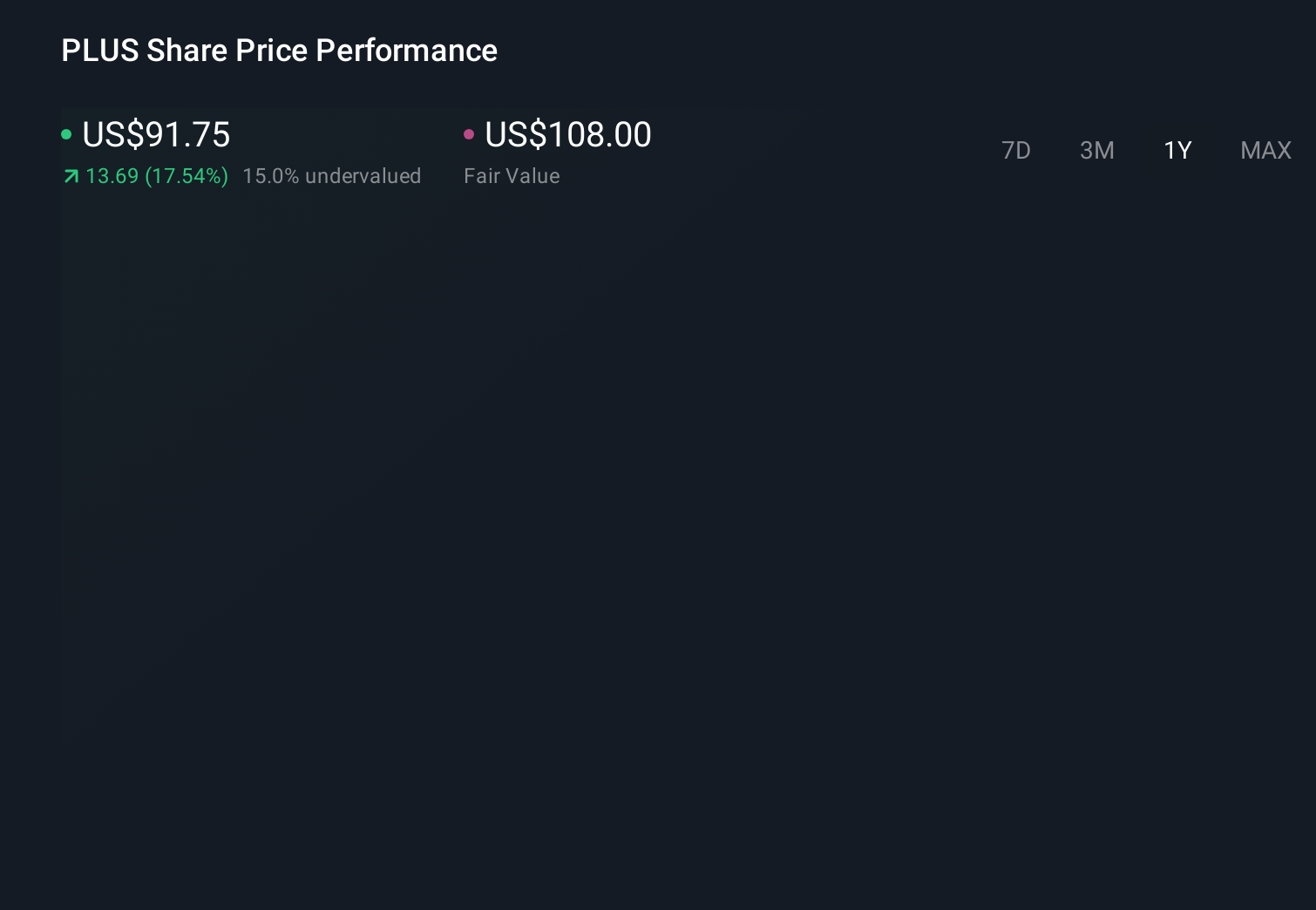

ePlus' narrative projects $2.2 billion revenue and $78.4 million earnings by 2028. This implies a 0.2% yearly revenue decline and a $32.5 million earnings decrease from $110.9 million today.

Uncover how ePlus' forecasts yield a $108.00 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between US$108 and about US$124 per share, underlining how far opinions can stretch. You should weigh that against the raised 20% to 22% net sales growth guidance, which could matter if large project driven revenue or margin compression start to affect how the business performs over time.

Explore 2 other fair value estimates on ePlus - why the stock might be worth just $108.00!

Build Your Own ePlus Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ePlus research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ePlus research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ePlus' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PLUS

ePlus

Provides information technology (IT) solutions that enable organizations to optimize IT environment and supply chain processes in the United States and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on American Resources ·

American Resources, $263M Market Cap + 19% ReElement Stake, From Coal to Critical Minerals

Fair Value:US$557.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on EPB Group Berhad ·

EPB: Strong Shareholder Backing, Continuous Insider Buying and Growth Opportunities Ahead

Fair Value:RM 0.548.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YO

youwakeup on Harvest Strategy Enhanced High Income Shares ETF ·

MSTE: Turning Bitcoin Volatility Into Monthly Cash Flow

Fair Value:CA$11.7579.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

57 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative