Advertisement

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like GoDaddy (NYSE:GDDY). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

See our latest analysis for GoDaddy

GoDaddy's Earnings Per Share Are Growing.

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS). Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Impressively, GoDaddy has grown EPS by 22% per year, compound, in the last three years. This has no doubt fuelled the optimism that sees the stock trading on a high multiple of earnings.

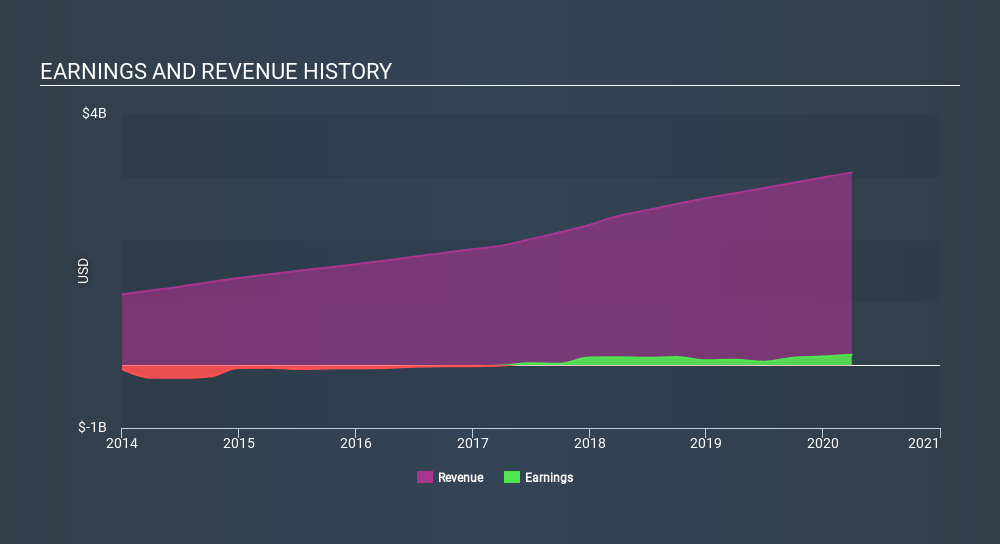

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. The good news is that GoDaddy is growing revenues, and EBIT margins improved by 3.1 percentage points to 8.7%, over the last year. Ticking those two boxes is a good sign of growth, in my book.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

While we live in the present moment at all times, there's no doubt in my mind that the future matters more than the past. So why not check this interactive chart depicting future EPS estimates, for GoDaddy?

Are GoDaddy Insiders Aligned With All Shareholders?

Since GoDaddy has a market capitalization of US$13b, we wouldn't expect insiders to hold a large percentage of shares. But we do take comfort from the fact that they are investors in the company. Indeed, they hold US$39m worth of its stock. That's a lot of money, and no small incentive to work hard. Even though that's only about 0.3% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

Is GoDaddy Worth Keeping An Eye On?

Given my belief that share price follows earnings per share you can easily imagine how I feel about GoDaddy's strong EPS growth. I think that EPS growth is something to boast of, and it doesn't surprise me that insiders are holding on to a considerable chunk of shares. Fast growth and confident insiders should be enough to warrant further research. So the answer is that I do think this is a good stock to follow along with. You should always think about risks though. Case in point, we've spotted 2 warning signs for GoDaddy you should be aware of, and 1 of them makes us a bit uncomfortable.

You can invest in any company you want. But if you prefer to focus on stocks that have demonstrated insider buying, here is a list of companies with insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NYSE:GDDY

GoDaddy

Engages in the design and development of cloud-based products in the United States and internationally.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor