Advertisement

- United States

- /

- Real Estate

- /

- NYSE:JOE

Assessing St. Joe (JOE) Valuation Following Strong Q3 Results and Leasing Gains

Simply Wall St

Reviewed by Simply Wall St

St. Joe (NYSE:JOE) posted growth across sales, revenue, and net income for the third quarter. Its Watersound Town Center continues to attract new tenants, bringing the retail hub to 98% leased.

See our latest analysis for St. Joe.

St. Joe has seen its share price jump 24.8% over the past month and 31.1% year-to-date, reflecting growing investor confidence after strong quarterly results, a bigger dividend, and steady leasing momentum at Watersound Town Center. With a one-year total shareholder return of 12.1% and multi-year gains topping 100%, the long-term trend remains positive and underscores optimism around both earnings growth and the company’s evolving business model.

If St. Joe’s momentum has you scanning the horizon for what else is attracting attention, broaden your view and discover fast growing stocks with high insider ownership

With shares rallying and the company reporting robust growth, the question now is whether St. Joe’s recent success leaves room for upside or if the market has already accounted for future gains in the stock price.

Price-to-Earnings of 32.3x: Is it justified?

St. Joe is trading at a price-to-earnings ratio of 32.3x, which the data shows is lower than its direct peer group but higher than the broader industry average. With shares recently rallying and the last close at $58.52, the valuation reflects significant optimism in the outlook relative to competitors and raises the question of whether future growth will meet expectations.

The price-to-earnings ratio measures how much investors are willing to pay for each dollar of earnings. It is a key comparison tool in the real estate sector, where earnings power and growth tend to be focal points for value assessment. A rising ratio can signal high confidence in profit growth, but it may also mean that the stock is priced for perfection.

Compared to its peer average P/E of 43.3x, St. Joe appears attractively valued. However, when compared to the US real estate industry’s average P/E of 28.2x, the stock appears somewhat expensive. This nuanced positioning shows that investors view St. Joe’s near-term prospects more favorably than the average sector company, though at a premium. No regression-based fair ratio estimate is available, so the current valuation could remain a moving target as the market recalibrates expectations.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 32.3x (ABOUT RIGHT)

However, slower revenue growth or unexpected industry headwinds could challenge current optimism and test whether the recent rally is sustainable in the months ahead.

Find out about the key risks to this St. Joe narrative.

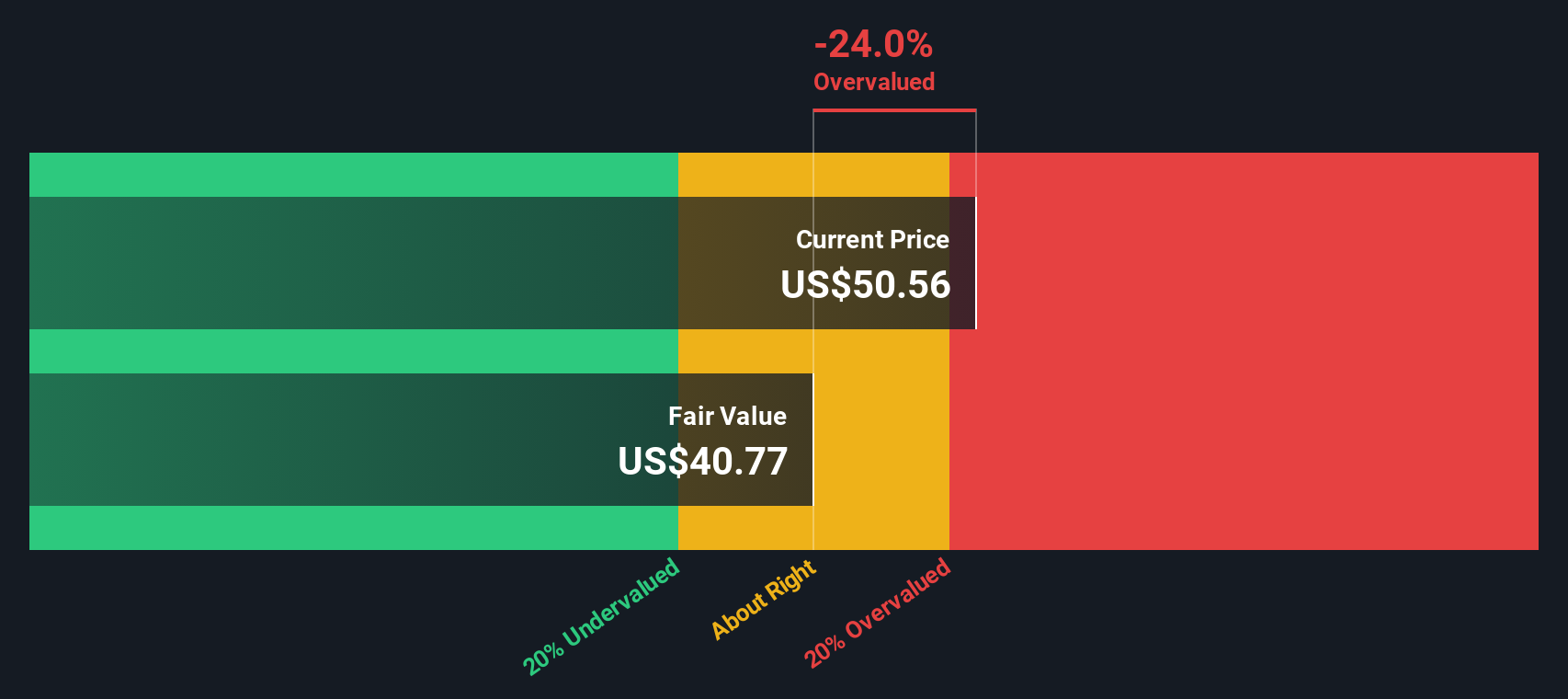

Another View: Discounted Cash Flow Tells a Different Story

While current valuation based on earnings multiples suggests St. Joe is somewhat expensive relative to the industry, our DCF model provides a different perspective. According to SWS DCF, the stock trades 27.7% below its estimated fair value, indicating it may actually be undervalued by the market. Could this disconnect signal untapped upside, or are the risks being overlooked?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out St. Joe for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own St. Joe Narrative

If these findings don’t quite fit your view, or you’d rather dig into the numbers and craft your own story, you can easily do so in just a few minutes with Do it your way

A great starting point for your St. Joe research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t limit your strategy to just one stock. Make smarter, bolder choices by taking advantage of cutting-edge screeners that spotlight tomorrow’s market leaders today.

- Spot opportunities for compounding income and boost your portfolio by tapping into these 16 dividend stocks with yields > 3% with attractive yields and strong financials.

- Catch the wave of technological change with these 25 AI penny stocks driving innovation in artificial intelligence, robotics, and automation across industries.

- Unlock hidden value by targeting these 876 undervalued stocks based on cash flows that may be overlooked by the crowd but stand out based on their cash flow fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:JOE

St. Joe

Operates as a real estate development, asset management, and operating company in the United States.

Solid track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor