Waters (WAT) has been making steady progress lately, and recent performance numbers are catching some attention. Shares climbed 32% over the past 3 months, driven by annual revenue growth and improving profit margins.

After a year of uneven total shareholder returns, Waters’ recent momentum stands out. The stock’s 31.99% three-month share price gain signals shifting sentiment and growing optimism, even as its 12-month total return remains modestly negative.

With shares closing in on analyst targets and still trading at a slight premium to intrinsic value, investors now face a classic dilemma: is Waters undervalued after its rally, or has the future already been priced in?

Advertisement

Most Popular Narrative: 3.1% Undervalued

Waters’ most followed narrative places fair value above the last closing price, suggesting analysts see even more upside despite the recent surge.

The planned combination with BD's Biosciences and Diagnostic Solutions business is expected to accelerate entry into biologics, precision medicine, and cell/gene therapy markets. These are segments with expanding analytical needs, unlocking new addressable markets and providing a multi-year revenue synergy opportunity, directly impacting future revenues and EPS growth.

Want to decode why analysts are betting on a premium for Waters? The answer is not just growth or guidance, but a series of bold, quantitative calls for revenue, profits, and future multiples. Curious which positive assumptions really drive this price target? Find out what lies beneath the headline numbers that could change the narrative for good.

However, execution risks related to Waters’ major acquisitions or ongoing weakness in key markets could quickly challenge analysts’ optimism about sustained profit growth.

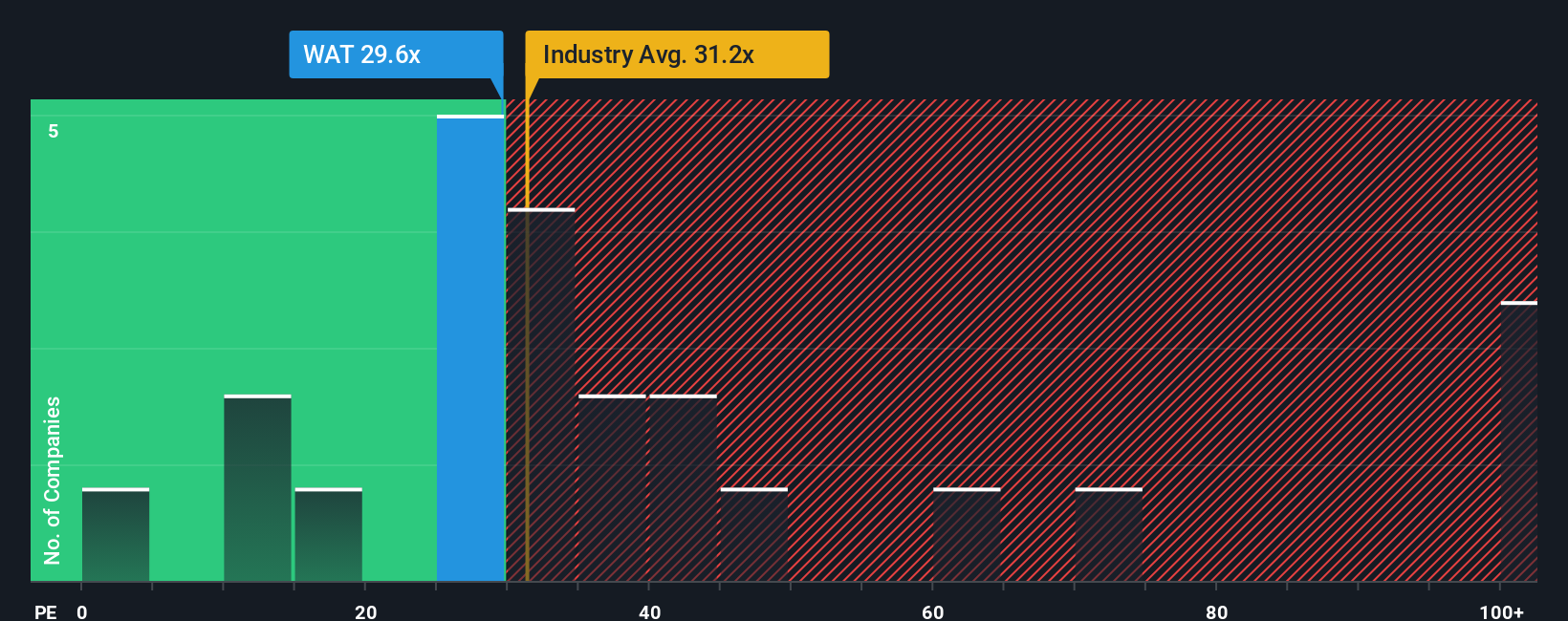

Looking at Waters using the price-to-earnings ratio, shares trade at 34.1x, which is pricier than both the peer average of 30.7x and the estimated market “fair ratio” of 24.5x. This gap suggests investors are paying a premium for growth and certainty. However, is that justified if sentiment turns?

If you see a different angle or want to dig into the numbers yourself, you can put together your own take on Waters in just a few minutes. Do it your way.

Tap into tech-driven breakthroughs by evaluating which companies top the charts as these 24 AI penny stocks, positioning themselves at the frontier of artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Waters might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.