Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:TTWO

Assessing Take-Two Interactive Software (TTWO) Valuation After Earnings Beat And Raised Guidance

Why Take-Two’s Latest Earnings Are Back in Focus

Take-Two Interactive Software (TTWO) moved back onto investors’ radar after reporting fiscal third quarter revenue of about US$1.70b, above prior guidance, along with a smaller net loss and higher full year earnings guidance.

See our latest analysis for Take-Two Interactive Software.

Despite the earnings beat and raised guidance, Take-Two’s recent 30-day share price return of 19.35% and year to date share price return of 23.02% show selling pressure, while the 3-year total shareholder return of 72.14% points to stronger longer term momentum.

If this latest quarter has you thinking about where growth in gaming and AI might show up next, it could be worth scanning 58 profitable AI stocks that aren't just burning cash as a starting list of ideas.

With the share price still well below its recent price targets and the stock showing mixed returns across different time frames, is Take-Two offering a sensible entry point, or are markets already factoring in the next leg of growth?

Most Popular Narrative: 30.4% Undervalued

With Take-Two Interactive Software last closing at $193.67 against a most-followed fair value estimate of about $278.23, the current setup hinges on how future bookings, margins and GenAI efficiencies actually play out.

Strategic investments in technology, AI, and content pipeline efficiency, alongside a strong release slate with multiple high-profile launches (including Borderlands 4, NBA 2K26, and Mafia: The Old Country), undergird management's outlook for record net bookings and enhanced profitability in the coming years.

Want to see what sits behind that confidence in record bookings and higher profitability? The narrative leans on faster growth, rising margins and a premium future earnings multiple. Curious how those ingredients combine to support that higher fair value and still use a discount rate just above 9%? The full story lays out the numbers in plain sight.

Result: Fair Value of $278.23 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to keep an eye on delays or underperformance in core franchises, as well as the ongoing pressure from rising development and marketing costs.

Find out about the key risks to this Take-Two Interactive Software narrative.

Another Angle On Valuation

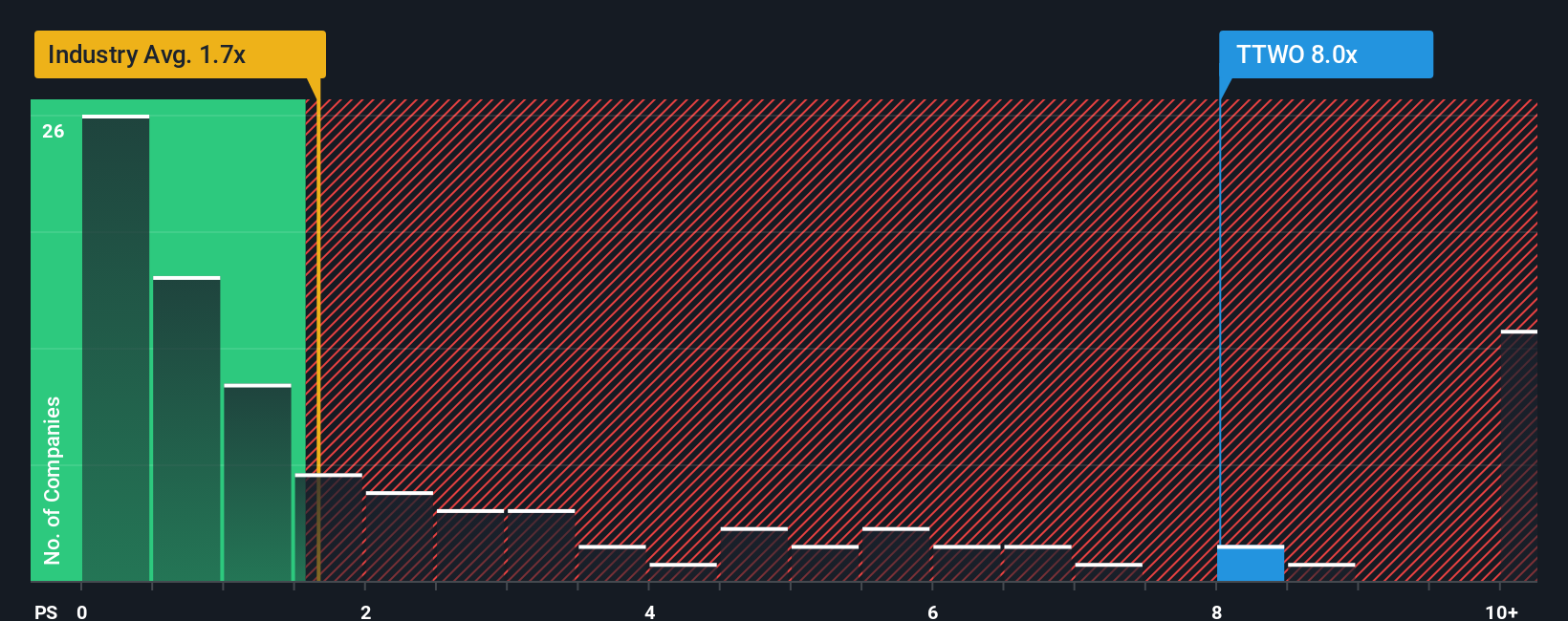

The 30.4% discount to the fair value estimate sits awkwardly next to Take-Two’s P/S of 5.5x, which is higher than peers at 4.5x, the US Entertainment industry at 1.4x, and even its own 3.9x fair ratio. Is the market pricing in extra execution risk, or something else?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Take-Two Interactive Software Narrative

If you see the numbers differently or just want to stress test your own view, you can spin up a personalized Take-Two thesis in minutes, Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Take-Two Interactive Software.

Looking for more investment ideas?

If you stop at Take-Two, you could miss other compelling setups. Use the screener to quickly spot different types of opportunities that fit your style.

- Target potential value opportunities by reviewing our 54 high quality undervalued stocks that combine solid fundamentals with pricing that may not fully reflect them.

- Prioritize resilience by checking out the 83 resilient stocks with low risk scores, focused on businesses with relatively lower risk profiles based on our scoring.

- Hunt for early-stage potential through the screener containing 24 high quality undiscovered gems, where smaller, less-followed companies still pass quality and fundamentals checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Take-Two Interactive Software might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TTWO

Take-Two Interactive Software

Develops, publishes, and markets interactive entertainment solutions for consumers worldwide.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4345.1% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

35 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

10 commentsusers have commented on this narrative

29 likesusers have liked this narrative

AH

AHaron on Eli Lilly ·

Eli Lilly: A Pipeline-Driven Growth Story Trading 30% Below What the Business Is Actually Worth

Fair Value:US$1.48k37.2% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$38110.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on DXN Holdings Bhd ·

DXN: New executive director appointment reinforces continuity and strengthens execution at board level

Fair Value:RM 0.6123.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UI

Uio96 on Alibaba Group Holding ·

Alibaba’s Next Act: Reclaiming Growth by Going Back to Its Online Roots

Fair Value:HK$20040.8% undervalued

12 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9829.2% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

35 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

10 commentsusers have commented on this narrative

29 likesusers have liked this narrative