Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ESI

Element Solutions (ESI) Margin Compression Challenges Bullish Outlook Despite Strong Growth Forecast

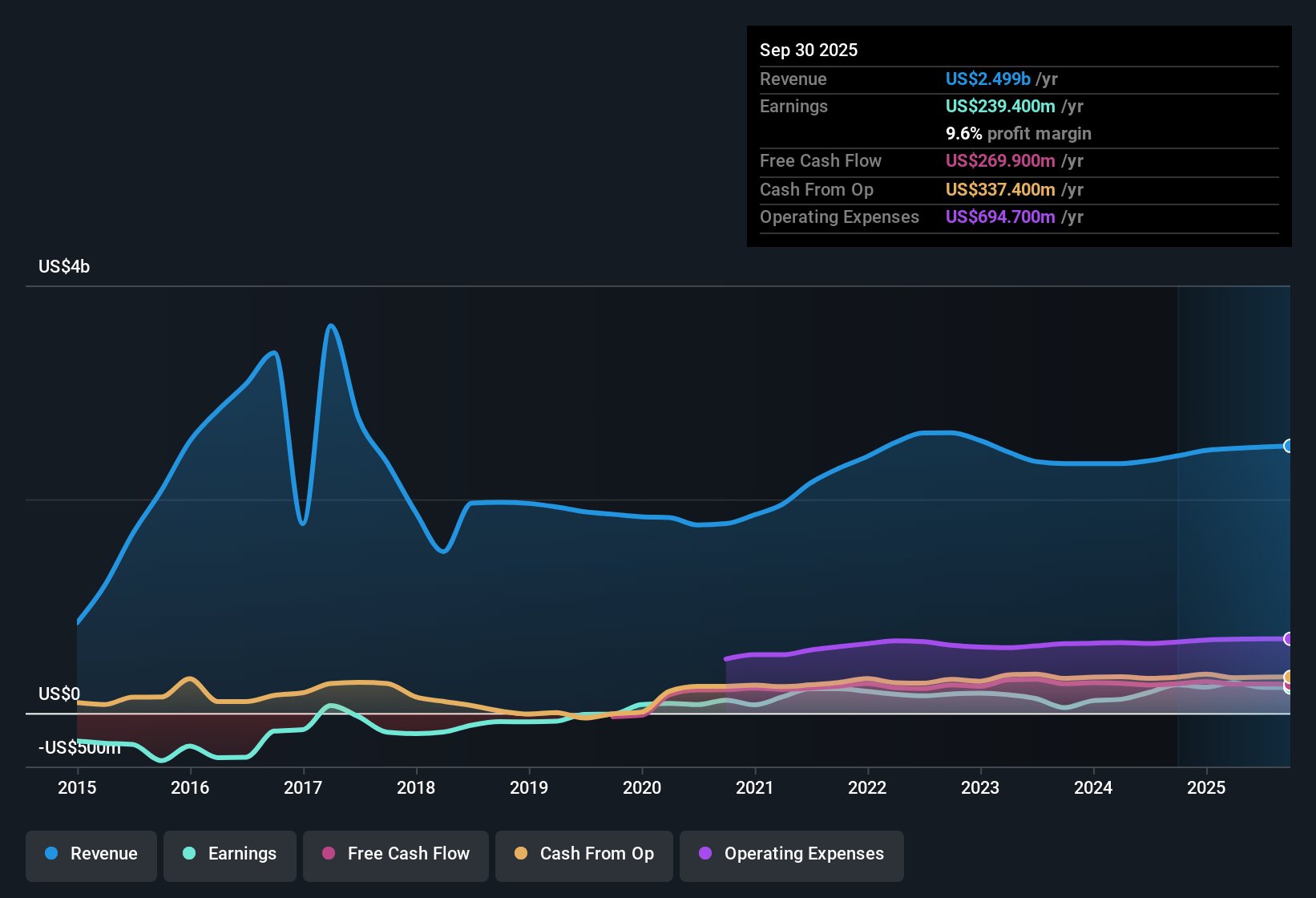

Element Solutions (NYSE:ESI) posted a net profit margin of 9.6%, down from 11% last year, and delivered average annual earnings growth of 9.8% over the past five years, even though its most recent year saw negative earnings growth. Analysts expect ESI’s earnings to accelerate by 28.6% per year moving forward, far outpacing the forecasted 15.7% annual gain for the broader US market. Revenue growth is projected at 6.4% per year. With a share price of $26, below fair value estimates, and a strong growth outlook, the market is watching both the company’s profit potential and the pressures from recent margin compression.

See our full analysis for Element Solutions.Now it is time to see how the numbers compare to the stories investors are telling. Let’s match the latest results against the prevailing narratives and see what holds up.

See what the community is saying about Element Solutions

Margin Expansion Forecast: 9.7% to 15.7% in Three Years

- Analysts expect profit margins to climb from today's 9.7% to 15.7% by 2028, a projected jump of 6 percentage points, despite the recent decline in reported margins compared to last year.

- According to the analysts’ consensus narrative, margin improvement is set to be driven by a mix of factors:

- Commercialization of higher-margin products like active copper and new portfolio optimization should improve sales mix and recurring profitability.

- Continued operational efficiency gains and investments in digitalization are anticipated to reduce operating costs. These efforts are expected to help fuel stronger net earnings growth that matches the ambitious margin guidance.

- Analysts' consensus view ties these expected margin conditions directly to near-term growth catalysts and cost management, suggesting the profit outlook is more robust than what recent results might imply.

See what Wall Street is forecasting around these margin gains 📊 Read the full Element Solutions Consensus Narrative.

PE Ratio Stays High Versus Peers

- Element Solutions' price-to-earnings ratio of 26.2x currently matches the US chemicals industry average but remains roughly double its direct peer average of 12.9x. This underscores that the stock still trades at a significant premium to closer competitors even after share price declines.

- Analysts' consensus narrative points out two sides to this valuation:

- Despite this high multiple, analysts believe sustained earnings quality and the expectation of robust profit growth can justify paying a premium relative to peers.

- At the same time, this premium is only warranted if Element Solutions successfully delivers on margin expansion targets and accelerates growth as projected. Otherwise, downside risk could catch up to the valuation.

Analyst Price Target: 18.5% Upside From Here

- With the current share price at $26.00 and analysts targeting $30.80, Element Solutions is seen as offering about 18.5% upside from today’s levels, provided its future earnings trajectory holds.

- According to the consensus narrative, realizing this upside depends on several factors:

- Revenue must grow to $2.8 billion and earnings to $438.6 million by 2028, with the PE ratio moderating to 19.9x, for the price target to materialize.

- While valuation models point to a much higher DCF fair value of $45.53, the more conservative analyst target expresses confidence in growth but also reflects the balance between notable expansion catalysts and enduring competitive or macro risks.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Element Solutions on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Looking at the figures from another angle? Share your perspective and shape your own narrative in just a few minutes by using Do it your way.

A great starting point for your Element Solutions research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Element Solutions’ rich valuation means its premium is justified only if ambitious margin and earnings growth targets materialize, leaving little room for disappointment.

If you want to avoid the risk of paying too much for uncertain growth, check out these 849 undervalued stocks based on cash flows where you’ll find stocks trading at more attractive valuations right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Element Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ESI

Element Solutions

Operates as a specialty chemicals company in the United States, China, and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3637.3% undervalued

42 followersusers have followed this narrative

14 commentsusers have commented on this narrative

20 likesusers have liked this narrative

MA

Marek_Trnka on CSG ·

Czechoslovak Group - is it really so hot?

Fair Value:€5547.3% undervalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

AL

alex30free on Swedencare ·

The Compound Effect: From Acquisition to Integration

Fair Value:SEK 46.2849.1% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$27.0328.7% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on Meta Platforms ·

The Superintelligence Pivot: Meta’s $135 Billion Bet on the Energy-Compute Nexus

Fair Value:US$555.8515.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on Apple ·

The Privacy Fortress: Apple’s Lean AI Path and the $100 Billion Buyback Engine

Fair Value:US$180.6341.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.6% undervalued

59 followersusers have followed this narrative

5 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$603.2233.5% undervalued

1277 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.7% undervalued

1072 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

Trending Discussion

US

User on Tesla ·

When was the last time that Tesla delivered on its promises? Lets go through the list! The last successful would be the Tesla Model 3 which was 2019 with first deliveries 2017. Roadster not shipped. Tesla Cybertruck global roll out failed. They might have a bunch of prototypes (that are being controlled remotely) And you think they'll be able to ship something as complicated as a robot? It's a pure speculation buy.

4

|1

US

User on Tesla ·

This article completely disregards (ignores, forgets) how far China is in this field. If Tesla continues on this path, they will be fighting for their lives trying to sell $40000 dollar robots that can do less than a $10000 dollar one from China will do. Fair value of Tesla? It has always been a hype stock with a valuation completely unbased in reality. Your guess is as good as mine, but especially after the carbon credit scheme got canned, it is downwards of $150.

3

|0

US

User on Tesla ·

There is a lot of Musk's puffery being echoed in this article. "ecosystem dominance", Tesla certainly do not dominate any of their new markets. If Tesla is the undisputed leader of the premium "Closed Garden.", it is only through EV's and that business has been declining year-on-year, despite the market increasing. Vehicle manufactures are finding that customers are rejecting the subscription model. "The Cybercab fleet (launching 2026) acts as the financial bridge.", that is a stretch. Even if Level 4/5 autonomy is achieved, "profitability" still has to be proved, where the competition is not necessarily Waymo, but Uber. Taking the driver out of a ride‑hailing service may not be the killer saving people think it will be. Likewise, outside of CGI and for quite some time, an Optimus humanoid robot may prove more expensive and not as useful, versatile, skilled and knowledgeable as a domestic worker. Telsa may be withdrawing from the EV market, but for its other ventures, they have arrived late to the party, do not lead and show no sign that they will dominate any of them.

2

|0