Advertisement

- United States

- /

- Healthcare Services

- /

- NasdaqGS:ADUS

How Addus HomeCare's Strong Q3 Results and Guidance Beat May Shape ADUS Investor Sentiment

Simply Wall St

Reviewed by Sasha Jovanovic

- Addus HomeCare reported third quarter 2025 earnings, delivering net income of US$22.85 million and diluted EPS of US$1.24, both up from the prior year, with revenues increasing 25% year over year and adjusted EPS surpassing analyst expectations.

- The results were driven by ongoing favorable demand for home-based healthcare services and improved hiring trends, particularly in the company's personal care segment.

- We’ll examine how the company's significant revenue and earnings beat supports its longer-term investment narrative and outlook.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

Addus HomeCare Investment Narrative Recap

To be a shareholder in Addus HomeCare, you need to believe that robust demand for home-based care and stable hiring trends can offset heavy exposure to government reimbursement and regulatory shifts. The recent earnings beat confirms solid execution and supports optimism around near-term top-line growth, but it does not materially reduce the largest immediate risk: potential Medicare rate reductions and policy changes that could directly impact profitability, particularly in the home health segment.

Among the recent announcements, Addus’s Q3 2025 results stand out: revenues climbed 25% year over year, and adjusted EPS beat expectations. This positive news directly reinforces the company’s ability to capture organic growth in its Personal Care segment, which is a key catalyst as Addus continues to benefit from state rate increases and growing demand for aging-in-place solutions.

Yet, despite these strong results, investors must not overlook the risk of future policy changes in Medicare or state-mandated rates that could...

Read the full narrative on Addus HomeCare (it's free!)

Addus HomeCare's narrative projects $1.7 billion revenue and $136.9 million earnings by 2028. This requires 10.1% yearly revenue growth and a $53.9 million earnings increase from $83.0 million today.

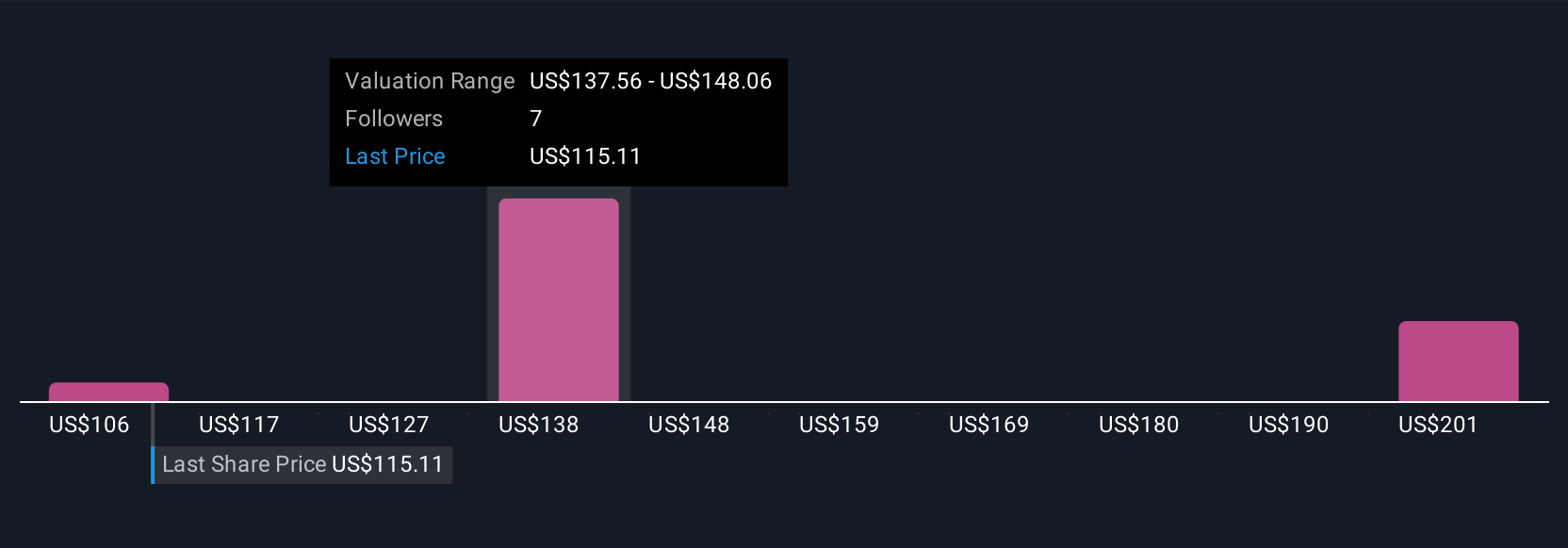

Uncover how Addus HomeCare's forecasts yield a $142.91 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community range from US$111.80 to US$198.30 per share. While opinions vary, the biggest current risk remains potential Medicare payment cuts and their impact on profitability, so you can see why many participants weigh regulatory outlooks differently.

Explore 5 other fair value estimates on Addus HomeCare - why the stock might be worth as much as 65% more than the current price!

Build Your Own Addus HomeCare Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Addus HomeCare research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Addus HomeCare research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Addus HomeCare's overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADUS

Addus HomeCare

Provides personal care services to elderly, chronically ill, disabled persons, and individuals who are at risk of hospitalization or institutionalization in the United States.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor