Advertisement

- United States

- /

- Food

- /

- NYSE:GIS

Is General Mills a Hidden Bargain After 26% Slide and Health-Focused Strategy Shift?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if General Mills stock is a hidden bargain or just priced for safety? If you're curious about where the real value lies, you're in the right place.

- Recently, the stock has seen some shifts, ticking up 0.6% over the past week but still down 26.2% so far this year and 25.2% in the past 12 months, hinting at changing market sentiment.

- Recent headlines have centered on the company's strategic push into health-focused brands and supply chain investments, which investors believe could set the stage for longer-term gains. At the same time, rising costs and ongoing concerns about inflation continue to weigh on sentiment.

- On our valuation checks, General Mills scores a 5 out of 6, suggesting it's undervalued in most key areas. See for yourself in the valuation scorecard. Let's break down what these valuation methods actually tell us, and stick around for an even smarter approach to value at the end of the article.

Find out why General Mills's -25.2% return over the last year is lagging behind its peers.

Approach 1: General Mills Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to today's value. This approach highlights what those future earnings are worth in present terms, helping investors see if a stock is trading below or above its intrinsic value.

For General Mills, the latest reported Free Cash Flow stands at $2.01 Billion. According to analyst estimates and Simply Wall St projections, Free Cash Flow is expected to grow steadily, reaching about $2.29 Billion in 2029. While analysts only directly estimate up to five years ahead, further projections extend out to ten years with moderate growth factored in.

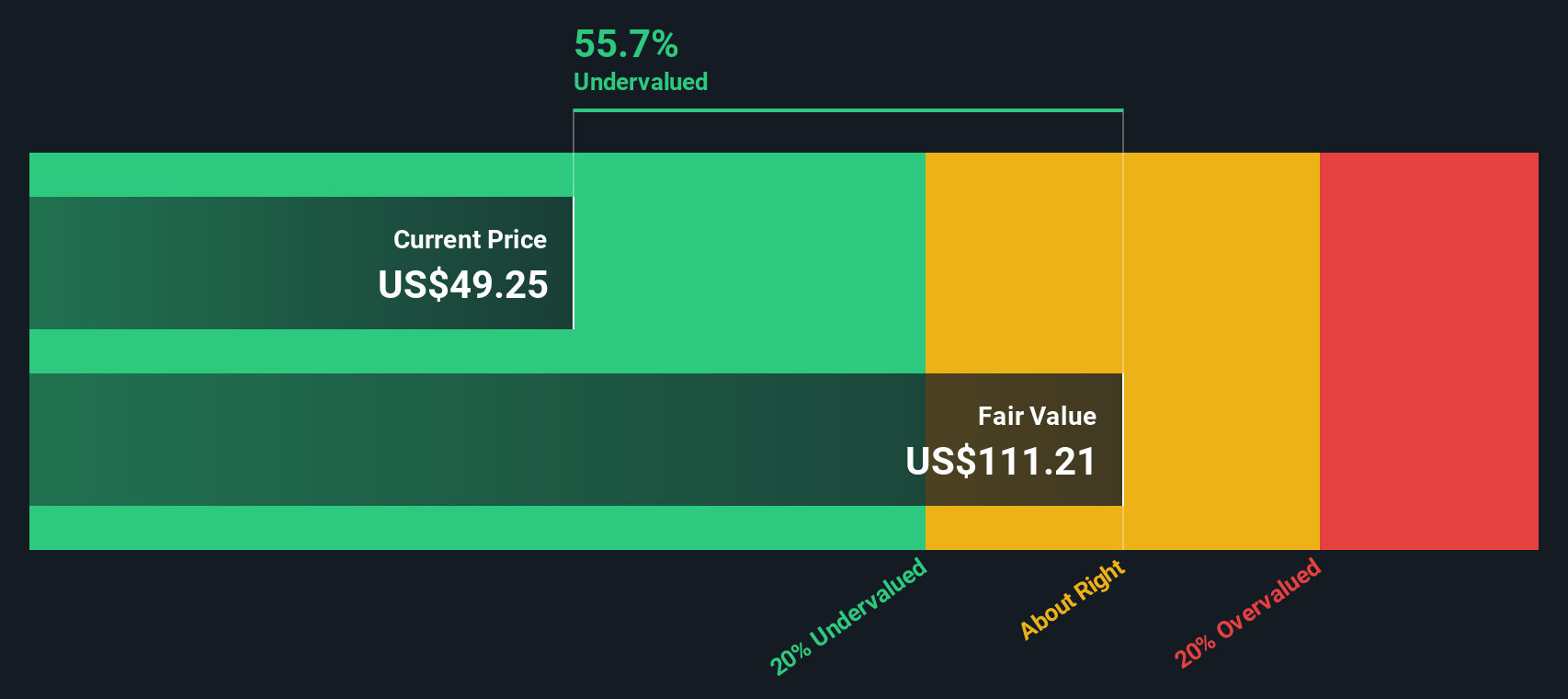

Based on this DCF method, the estimated intrinsic value for General Mills stock is $103.97 per share. Compared to its current share price, this implies the stock is trading at a steep 54.9% discount, which indicates it is significantly undervalued by this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests General Mills is undervalued by 54.9%. Track this in your watchlist or portfolio, or discover 876 more undervalued stocks based on cash flows.

Approach 2: General Mills Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for established, profitable companies like General Mills. It helps investors determine how much they are paying for each dollar of current earnings. This makes it especially relevant when a company has consistent profits and relatively stable cash flows.

What counts as a "fair" PE ratio shifts based on factors such as earnings growth prospects and the perceived risk of the business. Companies expected to grow faster or carry less risk will often command higher PE ratios, while slower-growing or riskier companies tend to trade at lower multiples compared to sector norms.

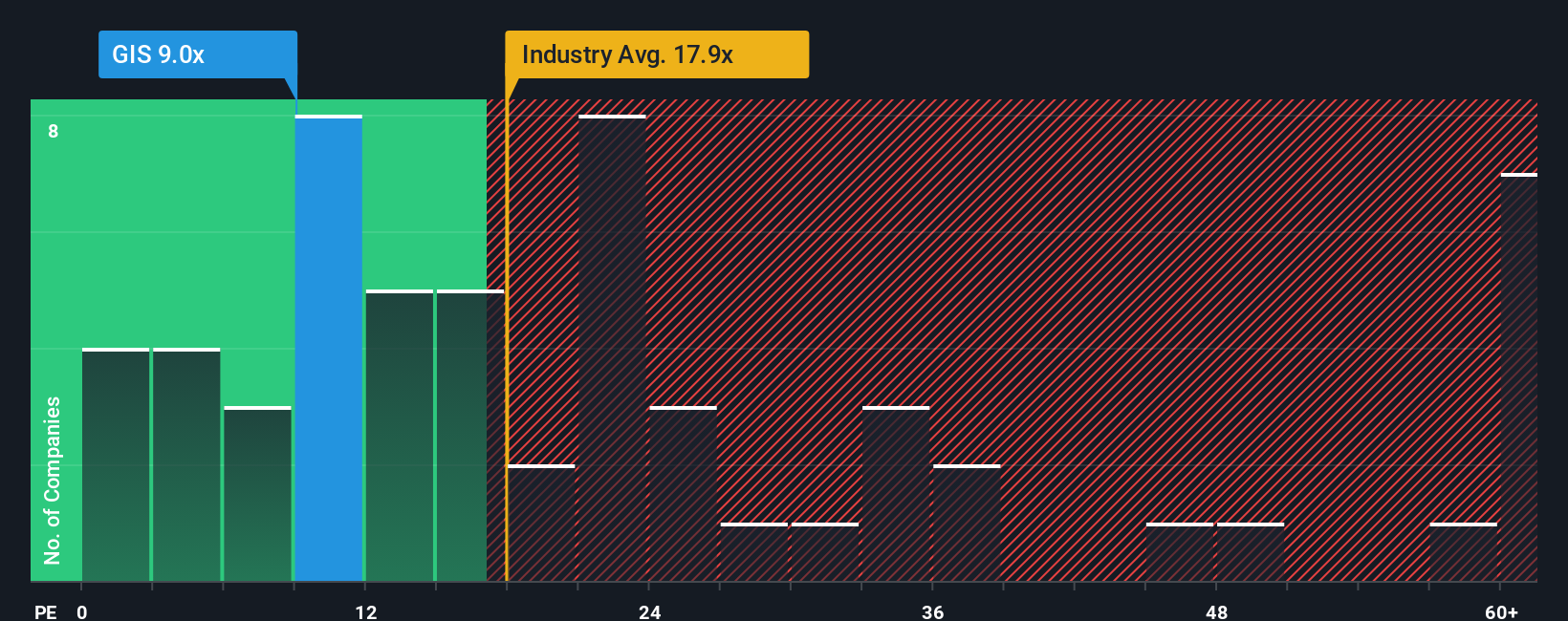

Currently, General Mills trades at a PE ratio of 8.6x, which is well below both the industry average of 18.6x and the average among peers at 23.6x. This kind of discount can signal a lack of market confidence, or potentially an overlooked opportunity for value. Simply Wall St’s proprietary “Fair Ratio” for General Mills is 11.4x. This reflects an expected PE multiple based on the company's unique earnings growth outlook, industry, margins, market cap, and risk profile.

While industry and peer comparisons are useful, the Fair Ratio distills more factors to paint a nuanced picture of value by accounting for General Mills’ specific characteristics. By comparing the actual PE to the Fair Ratio, we see General Mills trades meaningfully below its tailored benchmark. This suggests the stock is undervalued by this approach.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1403 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your General Mills Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story about a company, where you connect events, strategy, and outlook to what you believe the numbers will look like in the future, such as revenue growth, profit margins, and a fair value that makes sense to you. Narratives let you link the company's real-world story to a forecast and, ultimately, a price you'd be willing to pay, all within an intuitive tool on Simply Wall St's Community page that millions already use.

With Narratives, anyone can build or adopt a scenario for General Mills and see how their assumptions stack up against today’s price. This helps you decide when to act, not just based on static ratios but on how your view of the company's future compares to the market's. As new news and earnings are released, Narratives update in real time, keeping your analysis current and actionable.

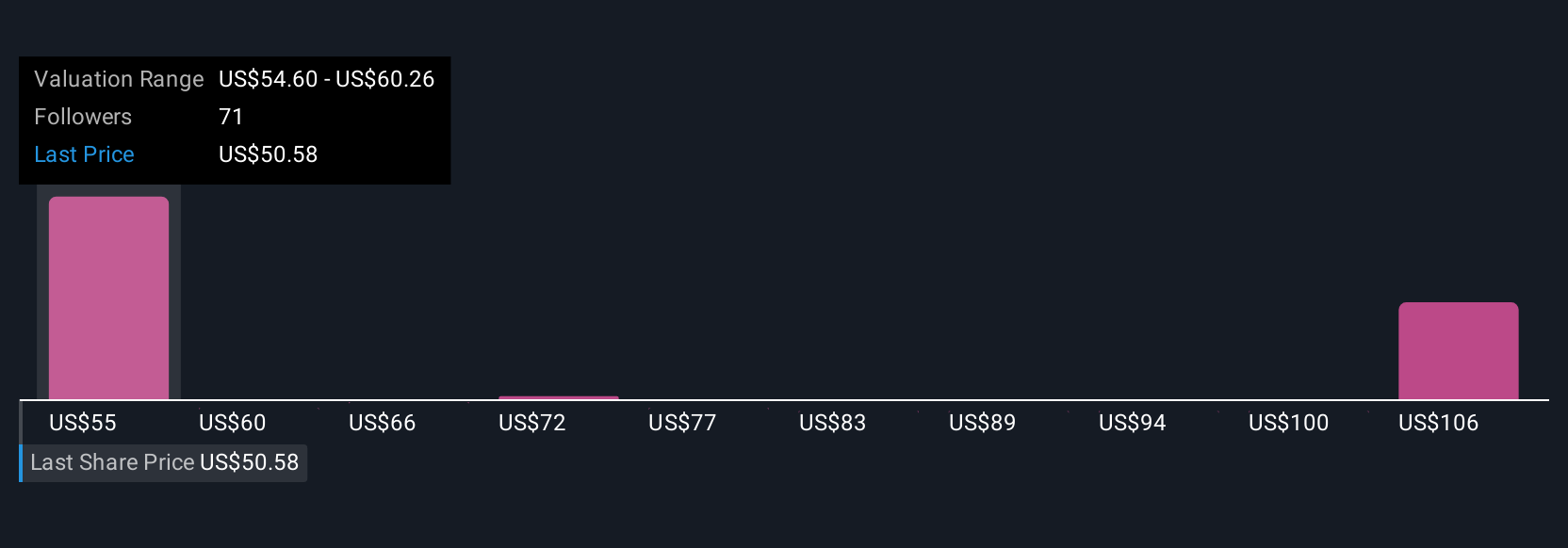

For example, one investor might see recent reinvestment and potential Yoplait closures as risks, predicting margin pressure and a lower fair value near $45 per share. Another might believe in the company’s innovation and expect stronger growth, supporting a more optimistic fair value as high as $63. Narratives make it easy to compare these perspectives and choose your own path.

Do you think there's more to the story for General Mills? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GIS

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor