Stock Analysis

- United States

- /

- Oil and Gas

- /

- NYSE:PR

We Think Permian Resources (NYSE:PR) Can Stay On Top Of Its Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Permian Resources Corporation (NYSE:PR) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Permian Resources

What Is Permian Resources's Debt?

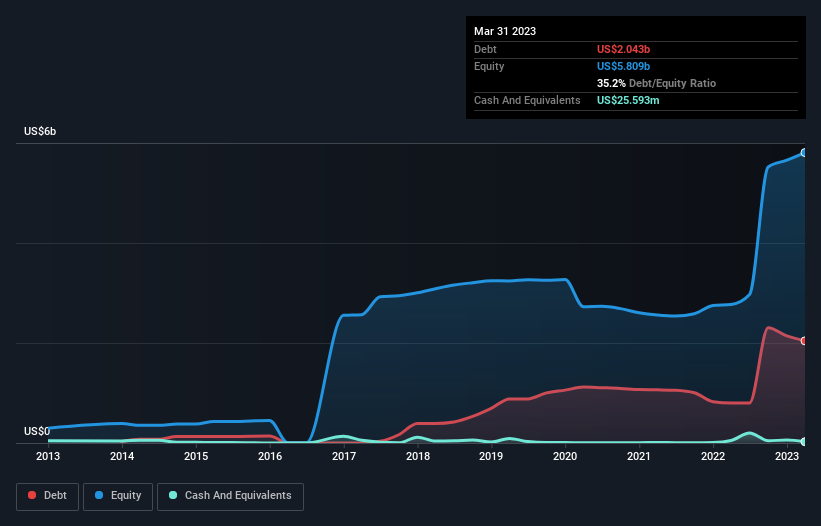

As you can see below, at the end of March 2023, Permian Resources had US$2.04b of debt, up from US$801.2m a year ago. Click the image for more detail. Net debt is about the same, since the it doesn't have much cash.

How Strong Is Permian Resources' Balance Sheet?

We can see from the most recent balance sheet that Permian Resources had liabilities of US$682.0m falling due within a year, and liabilities of US$2.23b due beyond that. Offsetting this, it had US$25.6m in cash and US$286.6m in receivables that were due within 12 months. So it has liabilities totalling US$2.60b more than its cash and near-term receivables, combined.

Permian Resources has a market capitalization of US$5.72b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Permian Resources has a low net debt to EBITDA ratio of only 1.1. And its EBIT easily covers its interest expense, being 11.0 times the size. So we're pretty relaxed about its super-conservative use of debt. Even more impressive was the fact that Permian Resources grew its EBIT by 460% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Permian Resources can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. During the last two years, Permian Resources produced sturdy free cash flow equating to 51% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Permian Resources's demonstrated ability to grow its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. Taking all this data into account, it seems to us that Permian Resources takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for Permian Resources (1 makes us a bit uncomfortable) you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're helping make it simple.

Find out whether Permian Resources is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PR

Permian Resources

Permian Resources Corporation, an independent oil and natural gas company, focuses on the development of crude oil and related liquids-rich natural gas reserves in the United States.

Reasonable growth potential second-rate dividend payer.