Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:LPG

Revenue Miss: Dorian LPG Ltd. Fell 5.5% Short Of Analyst Revenue Estimates And Analysts Have Been Revising Their Models

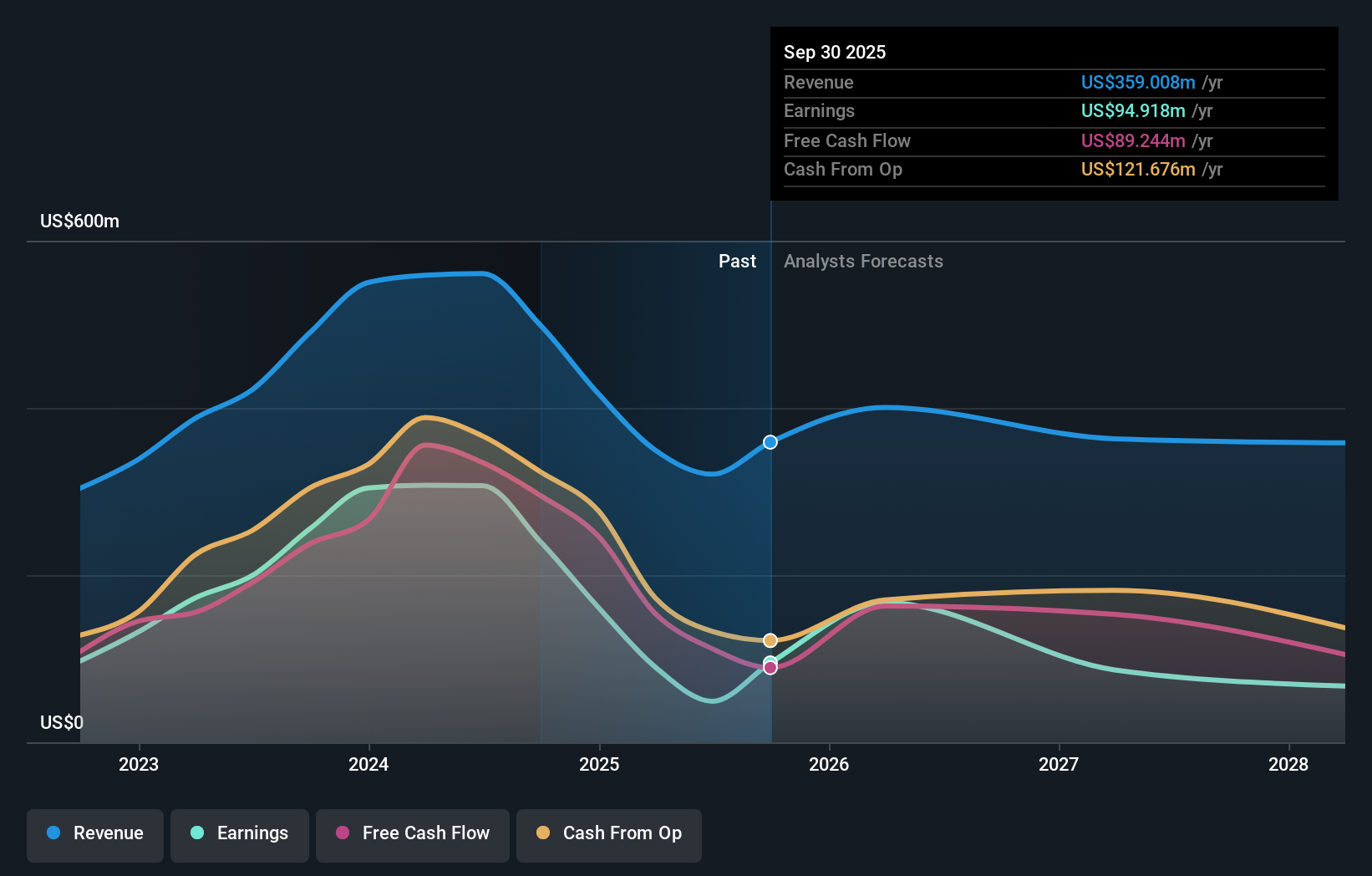

Dorian LPG Ltd. (NYSE:LPG) missed earnings with its latest second-quarter results, disappointing overly-optimistic forecasters. Results look to have been somewhat negative - revenue fell 5.5% short of analyst estimates at US$123m, and statutory earnings of US$1.30 per share missed forecasts by 4.4%. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Taking into account the latest results, the current consensus from DorianG's three analysts is for revenues of US$400.5m in 2026. This would reflect a meaningful 12% increase on its revenue over the past 12 months. Per-share earnings are expected to jump 54% to US$3.42. Before this earnings report, the analysts had been forecasting revenues of US$387.5m and earnings per share (EPS) of US$4.04 in 2026. So it's pretty clear the analysts have mixed opinions on DorianG after the latest results; even though they upped their revenue numbers, it came at the cost of a substantial drop in per-share earnings expectations.

Check out our latest analysis for DorianG

The consensus price target was unchanged at US$35.20, suggesting the business is performing roughly in line with expectations, despite some adjustments to profit and revenue forecasts. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic DorianG analyst has a price target of US$48.00 per share, while the most pessimistic values it at US$26.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting DorianG's growth to accelerate, with the forecast 24% annualised growth to the end of 2026 ranking favourably alongside historical growth of 9.1% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 2.9% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that DorianG is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. The consensus price target held steady at US$35.20, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple DorianG analysts - going out to 2028, and you can see them free on our platform here.

It is also worth noting that we have found 4 warning signs for DorianG (2 are significant!) that you need to take into consideration.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:LPG

DorianG

Engages in the transportation of liquefied petroleum gas through its LPG tankers worldwide.

Excellent balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor