Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:ET

How Entergy Louisiana’s 20-Year Gas Deal Could Strengthen Energy Transfer’s (ET) Revenue Stability

Simply Wall St

Reviewed by Sasha Jovanovic

- In November 2025, Entergy Louisiana and Energy Transfer announced a 20-year agreement for Energy Transfer to supply 250,000 MMBtu per day of firm natural gas transportation, supporting new energy facilities and projects such as Meta's upcoming data center in North Louisiana.

- This long-term arrangement signals the growing importance of natural gas infrastructure in powering major developments tied to technology and economic growth.

- We'll explore how this new contract and related pipeline expansion could enhance Energy Transfer's investment narrative by strengthening its contracted revenue base.

Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

Energy Transfer Investment Narrative Recap

To be a shareholder in Energy Transfer, you would need to believe in sustained demand for U.S. natural gas infrastructure, underpinned by long-term contracts and expansion into growth sectors like data centers. The new 20-year agreement with Entergy Louisiana further supports the revenue base but does not materially change the most important short-term catalyst, volume recovery in core pipeline assets, or the leading near-term risk of weaker-than-expected Bakken and Permian volumes.

Among recent announcements, the increase in Energy Transfer’s quarterly cash distribution to $0.3325 per unit stands out. This reflects management’s continued commitment to returning cash to unitholders, supporting investor confidence during a period where execution and project development remain crucial catalysts for the business.

However, against this backdrop, investors should be aware that execution risks, such as project delays or cost overruns...

Read the full narrative on Energy Transfer (it's free!)

Energy Transfer's narrative projects $99.8 billion in revenue and $6.7 billion in earnings by 2028. This requires 7.4% yearly revenue growth and a $2.2 billion increase in earnings from the current $4.5 billion.

Uncover how Energy Transfer's forecasts yield a $21.87 fair value, a 30% upside to its current price.

Exploring Other Perspectives

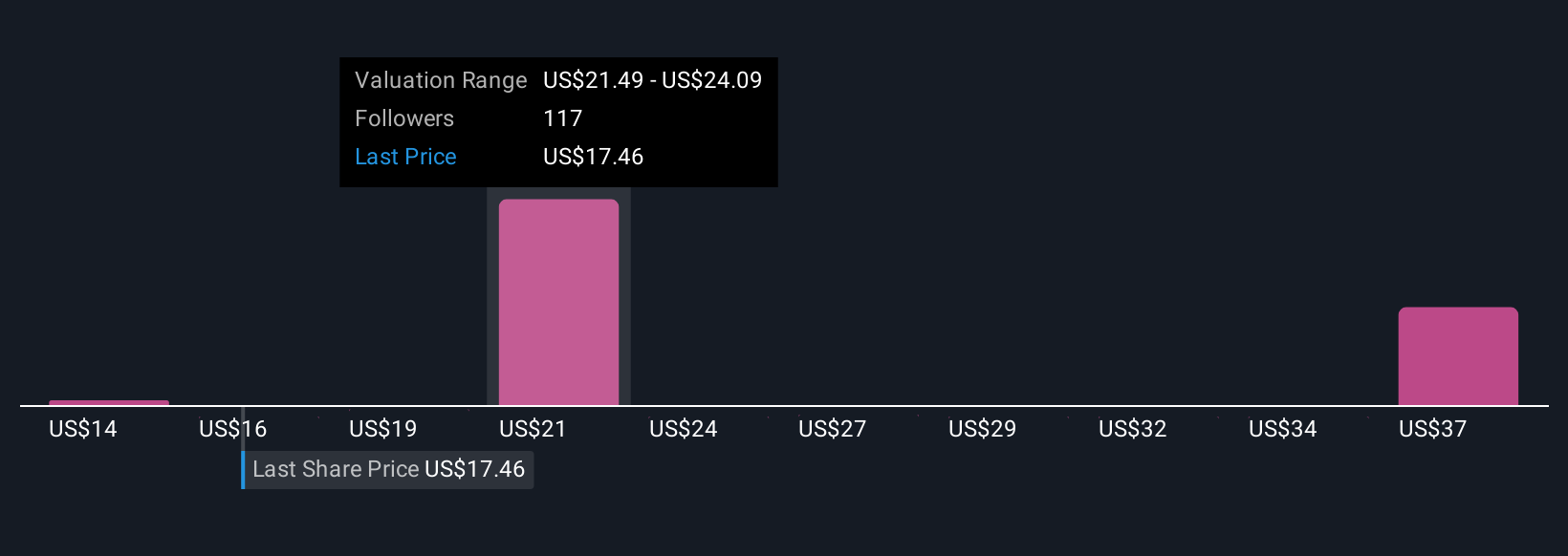

The Simply Wall St Community includes 22 opinions on fair value for Energy Transfer, ranging from US$15.48 to US$46.93 per share. While many are watching the company’s progress on new long-term contracts, the variety of forecasts highlights just how widely views can differ on the company’s next phase, consider exploring these alternative viewpoints for a fuller picture.

Explore 22 other fair value estimates on Energy Transfer - why the stock might be worth over 2x more than the current price!

Build Your Own Energy Transfer Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Energy Transfer research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Energy Transfer research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Energy Transfer's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Energy Transfer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ET

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor