- United States

- /

- Trade Distributors

- /

- NYSE:WSO

Watsco (NYSE:WSO) Expands in Southwest with AI Innovations, Faces Supply Chain and Cost Challenges

Reviewed by Simply Wall St

Navigate through the intricacies of Watsco with our comprehensive report here.

Unique Capabilities Enhancing Watsco's Market Position

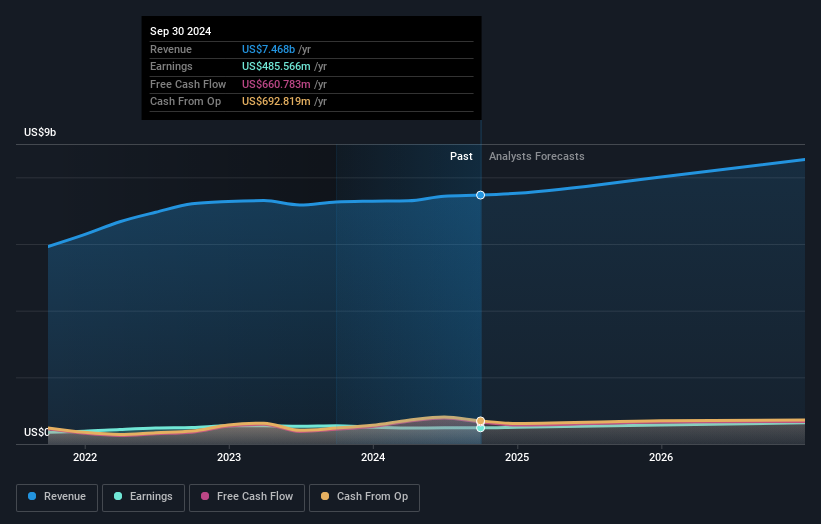

Watsco's revenue growth, as highlighted by a 15% increase year-over-year, underscores its strong market position. This growth is driven by high demand in both residential and commercial sectors, as noted by CEO Albert Nahmad. The company's commitment to product innovation, with new lines contributing significantly to sales, showcases its ability to maintain a competitive edge. Furthermore, Watsco's focus on customer satisfaction, as evidenced by improved scores, reinforces its dedication to service excellence, potentially leading to repeat business and referrals. Additionally, the company’s debt-free status and stable dividends over the past decade highlight its financial health and stability.

Critical Issues Affecting the Performance of Watsco and Areas for Growth

Challenges such as supply chain disruptions have impacted inventory levels, reflecting operational inefficiencies that need addressing. Rising raw material costs have also pressured profit margins, necessitating strategic cost management to sustain profitability. Furthermore, increased competition in the HVAC market has led to pricing pressures, requiring Watsco to remain vigilant and innovative. The company's current net profit margin of 6.5% is below the previous year's 7.6%, and earnings growth has seen an 11.9% decline over the past year. Moreover, the company's trading above its estimated fair value suggests it may be overvalued compared to industry standards.

Emerging Markets Or Trends for Watsco

Watsco is strategically expanding into new markets, such as the Southwest region, where HVAC demand is rising. This geographical expansion could significantly boost market share and revenue. The company's investment in AI-driven solutions aims to enhance operational efficiency and customer engagement, reflecting a forward-thinking approach. Additionally, exploring partnerships with local contractors could leverage local expertise, improving service delivery and customer satisfaction.

Regulatory Challenges Facing Watsco

The current economic climate presents uncertainties that could affect consumer spending on home improvements, posing a potential risk to sales. Regulatory changes could also impact operational costs and compliance requirements, necessitating proactive management. Supply chain vulnerabilities remain a concern, highlighting the need for diversified suppliers to ensure continuity of operations.

Conclusion

Watsco's impressive 15% revenue growth highlights its strong market position, driven by high demand in both residential and commercial sectors. However, the company faces challenges such as supply chain disruptions and rising raw material costs that have pressured profit margins, which have declined from 7.6% to 6.5% over the past year. Despite these issues, Watsco's strategic expansion into the Southwest region and investment in AI-driven solutions position it well for future growth. The company's current trading price above its estimated fair value suggests a potential risk of overpricing, but its debt-free status and stable dividends underscore financial stability, presenting a mixed outlook for investors.

Turning Ideas Into Actions

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Watsco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NYSE:WSO

Watsco

Engages in the distribution of air conditioning, heating, refrigeration equipment, and related parts and supplies in the United States and internationally.

Flawless balance sheet established dividend payer.