StandardAero (NYSE:SARO) has caught investor attention this week as its stock moved in line with broader market sentiment. Recent trading data shows little change in price, which prompts a closer look at what is driving the company’s valuation.

While StandardAero’s share price has barely budged this week, investors should note that momentum has faded over the past quarter after a solid start to the year. The stock’s year-to-date share price return stands at 9.37%, but its 1-year total shareholder return is down 9.81%, suggesting that confidence has softened even as growth potential still exists.

With analyst price targets suggesting upside and the company showing robust financial growth, investors are left to consider if StandardAero is currently undervalued or if the market has already factored in all of its future potential. Is there a genuine buying opportunity here, or is everything priced in?

Advertisement

Price-to-Earnings of 67.5x: Is it justified?

StandardAero is trading at a price-to-earnings (P/E) ratio of 67.5x, which stands out as notably expensive against its listed price of $26.84 per share. This elevated multiple sends a clear signal that the market is currently pricing in substantial future profit growth.

The P/E ratio reflects how much investors are willing to pay for each dollar of a company’s earnings. For a business like StandardAero in the Aerospace & Defense sector, a high P/E can sometimes be justified by strong growth expectations or a unique profit profile. However, it also suggests buyers are paying a premium for anticipated results.

Compared to its sector, the contrast is even sharper. The US Aerospace & Defense industry averages a P/E of just 38.5x, while StandardAero’s fair P/E, based on regression analysis, would be 35.8x. The current market valuation nearly doubles these benchmarks, indicating the price may be running well ahead of sector norms and underlying fundamentals.

However, persistent sector underperformance or slower than expected earnings growth could quickly alter market sentiment and challenge the current valuation.

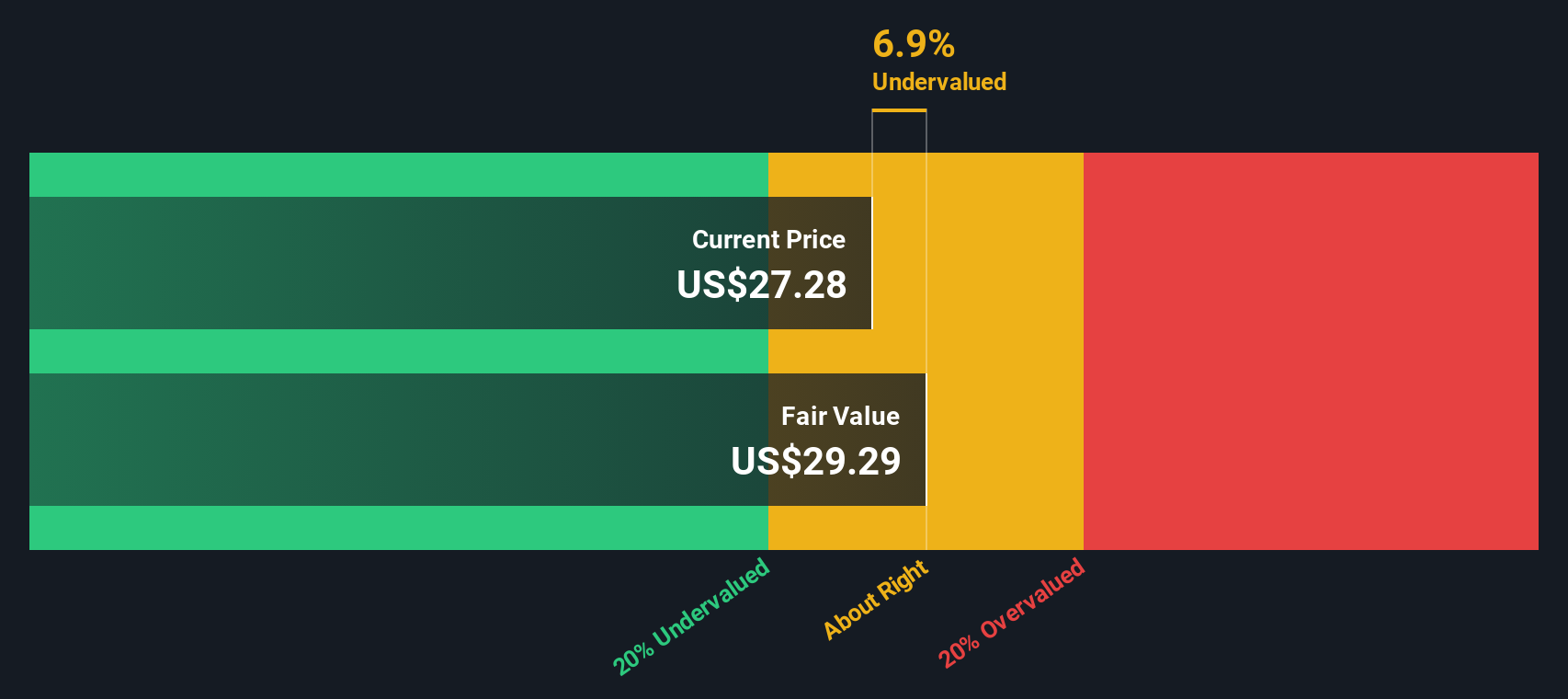

Another View: SWS DCF Model Suggests Undervaluation

While StandardAero appears expensive when considering its P/E ratio, our DCF model offers a contrasting assessment. The SWS DCF model estimates fair value at $31.56 per share, which is about 14.9% higher than the current price. This difference could indicate an overlooked opportunity, or it may highlight a risk that investors should consider.

Keep in mind, if you have a different perspective or want to dig into the numbers yourself, you can build your own view in just a few minutes with Do it your way.

A great starting point for your StandardAero research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Winning Investment Ideas?

Great opportunities rarely wait around. Uncover stocks with strong upside potential, sector innovations, and real growth by using these targeted screeners before others spot them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Provides aerospace engine aftermarket services for fixed and rotary wing aircraft in the United States, Canada, the United Kingdom, Rest of Europe, Asia, and internationally.