- United States

- /

- Machinery

- /

- NYSE:HY

Is Hyster-Yale Materials Handling (NYSE:HY) Weighed On By Its Debt Load?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Hyster-Yale Materials Handling, Inc. (NYSE:HY) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Hyster-Yale Materials Handling

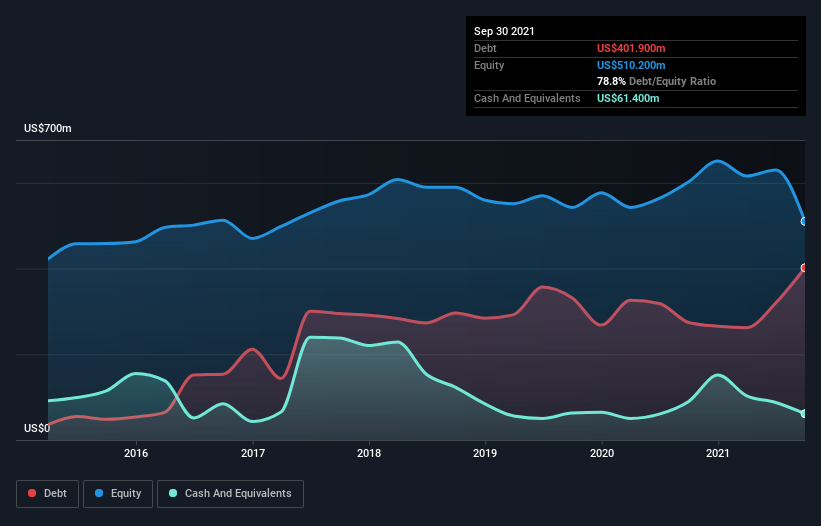

What Is Hyster-Yale Materials Handling's Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Hyster-Yale Materials Handling had US$401.9m of debt, an increase on US$274.3m, over one year. On the flip side, it has US$61.4m in cash leading to net debt of about US$340.5m.

How Healthy Is Hyster-Yale Materials Handling's Balance Sheet?

According to the last reported balance sheet, Hyster-Yale Materials Handling had liabilities of US$1.01b due within 12 months, and liabilities of US$495.1m due beyond 12 months. On the other hand, it had cash of US$61.4m and US$475.8m worth of receivables due within a year. So it has liabilities totalling US$963.5m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's US$668.4m market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Hyster-Yale Materials Handling's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Hyster-Yale Materials Handling's revenue was pretty flat, and it made a negative EBIT. While that hardly impresses, its not too bad either.

Caveat Emptor

Importantly, Hyster-Yale Materials Handling had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at US$30m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of US$145m over the last twelve months. So suffice it to say we consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Hyster-Yale Materials Handling (of which 1 shouldn't be ignored!) you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Hyster-Yale might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:HY

Hyster-Yale

Through its subsidiaries, designs, engineers, manufactures, sells, and services a line of lift trucks, attachments, and aftermarket parts worldwide.

Outstanding track record, undervalued and pays a dividend.