Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:BCC

Should Boise Cascade’s (BCC) Lower Earnings and New Buyback Program Prompt Reevaluation by Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past week, Boise Cascade Company reported third quarter 2025 earnings showing a decrease in sales to US$1.67 billion and net income falling to US$21.77 million, alongside the announcement of a new share repurchase program of up to US$300 million and a quarterly dividend of US$0.22 per share.

- The combination of lower earnings and renewed capital return initiatives signals management’s focus on supporting shareholder value despite recent profit challenges.

- With both reduced profitability and a substantial new share buyback now in focus, we’ll review how these latest developments may reshape Boise Cascade’s investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Boise Cascade Investment Narrative Recap

To be a shareholder in Boise Cascade today, one needs confidence in the company’s ability to weather earning pressures from softer wood products pricing and demand, while capturing long-term opportunities in U.S. residential and remodeling construction. The steep decline in third-quarter earnings puts added attention on both sustained revenue headwinds and management’s capital allocation, but does not materially alter the underlying catalysts or key risks, particularly exposure to pricing volatility and construction activity, in the near term.

The fresh US$300 million share repurchase authorization stands out among recent company developments, reinforcing Boise Cascade’s commitment to capital returns even as profitability weakens. This move, paired with the continued quarterly dividend, may help support the stock against ongoing earnings volatility, but investors still face the challenge of lower margins and uncertainty in end-market demand.

Yet, despite capital return efforts, investors should be aware that ongoing earnings declines tied to ...

Read the full narrative on Boise Cascade (it's free!)

Boise Cascade's outlook anticipates $7.0 billion in revenue and $285.8 million in earnings by 2028. This scenario requires a 2.4% annual revenue growth rate and a $23.5 million increase in earnings from the current $262.3 million level.

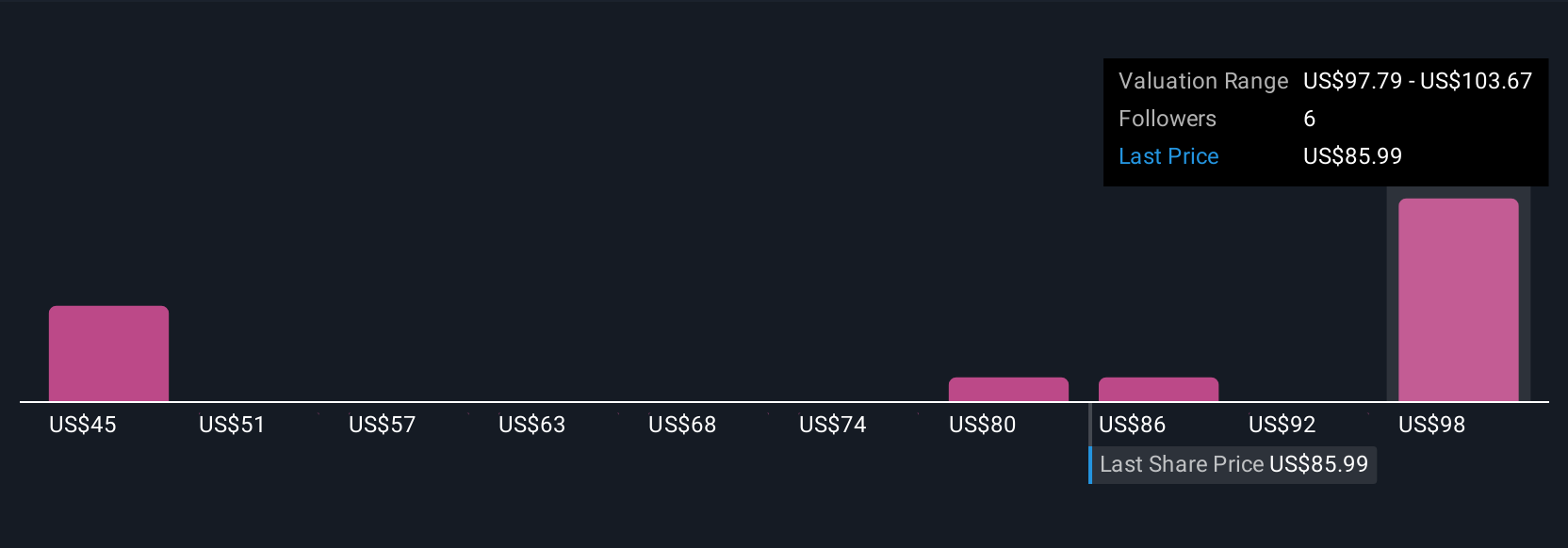

Uncover how Boise Cascade's forecasts yield a $91.17 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community estimate Boise Cascade's fair value from US$70 to US$229, underscoring substantial differences in expectations. Recent profit declines amplified by softer product pricing remain top-of-mind, shaping how some view future returns and risks.

Explore 5 other fair value estimates on Boise Cascade - why the stock might be worth over 3x more than the current price!

Build Your Own Boise Cascade Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Boise Cascade research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boise Cascade research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boise Cascade's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boise Cascade might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BCC

Boise Cascade

Engages in manufacture and sale of engineered wood products (EWP) and plywood, and wholesale distribution of building materials in the United States and Canada.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor