Advertisement

- United States

- /

- Machinery

- /

- NasdaqGS:NDSN

Nordson’s Rising Sales Mask Ongoing Margin Questions - What Investors Need To Know Now

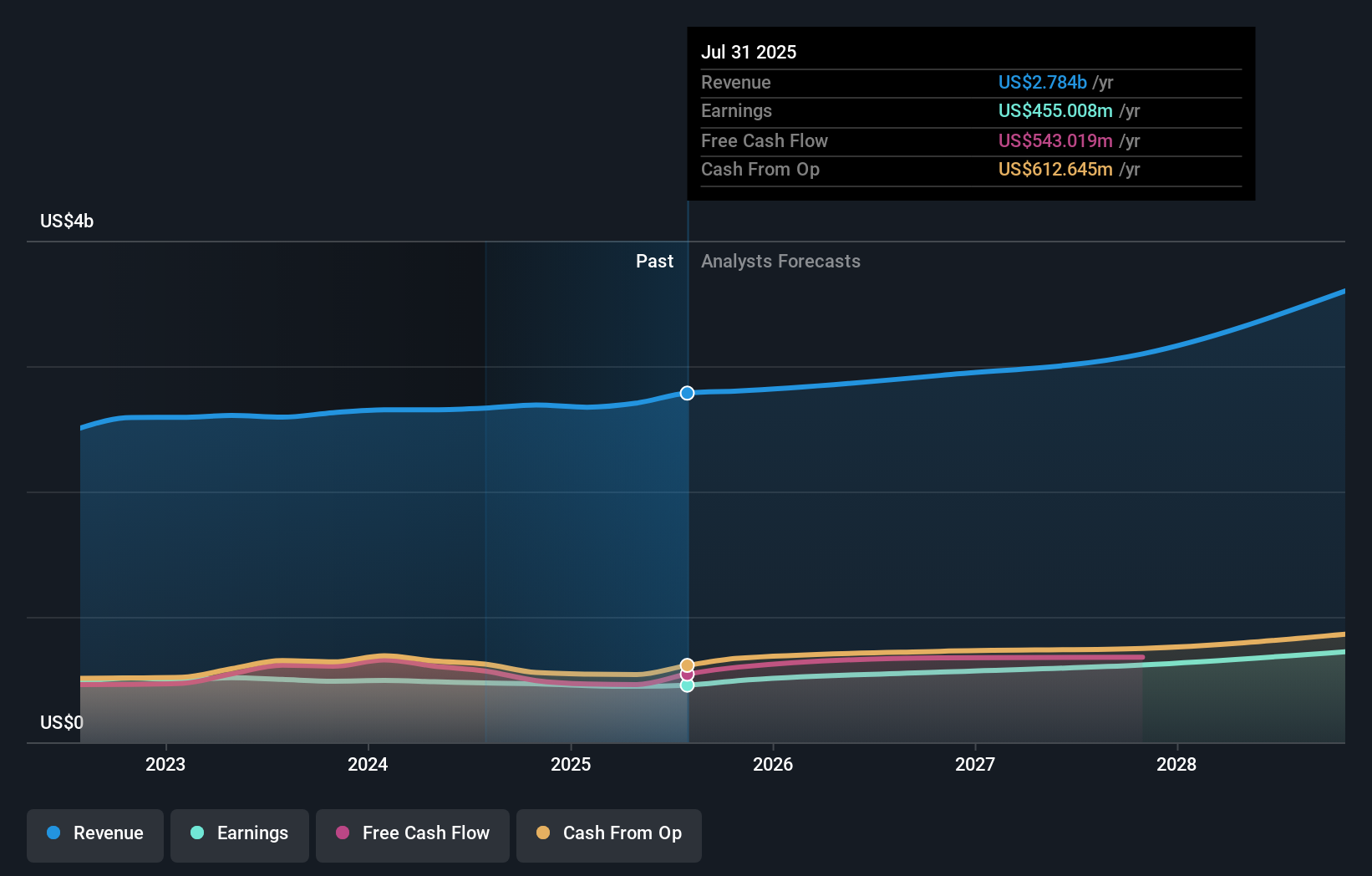

- Nordson reported second quarter sales of US$682.94 million, up from US$650.64 million a year ago, and issued guidance for third quarter sales of US$710 to US$750 million, supported by a healthy backlog and strong order entry.

- In addition to operational performance, Nordson repurchased 423,441 shares for US$85.32 million, further reducing its outstanding share count under a buyback program that has been running since 2014.

- With the company projecting further sales growth and highlighting backlog strength, we'll now explore how these updates may impact Nordson’s investment narrative.

Nordson Investment Narrative Recap

Being a Nordson shareholder means believing in the company’s ability to turn its steady order flow and backlog into sales growth, while also managing earnings volatility and margin pressure. The latest quarterly update reinforced stronger revenue guidance for the short term, largely supported by higher order intake, but the decline in net income and EPS suggests profitability remains the key issue to watch, this news doesn’t seem to materially reduce that risk right now.

Of all recent company announcements, Nordson’s third quarter sales guidance, set at US$710 to US$750 million, is most relevant, as it reflects management’s view of continued demand strength and near-term sales momentum. Short-term optimism around order flow and revenue only partially addresses concerns about earnings growth, meaning investors may want to look beyond just the headline sales figure.

However, while sales may be trending higher, investors should be aware of the persistent risk that margin pressures...

Read the full narrative on Nordson (it's free!)

Exploring Other Perspectives

Three members of the Simply Wall St Community estimate Nordson’s fair value between US$232.93 and US$243.29 per share. While opinions vary, renewed margin pressure linked to recent earnings trends could shape broader views on Nordson’s future performance.

Explore 3 other fair value estimates on Nordson - why the stock might be worth $232.93!

Build Your Own Nordson Narrative

Disagree with existing narratives? Create your own in under 3 minutes , extraordinary investment returns rarely come from following the herd.

- A great starting point for your Nordson research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Nordson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Nordson's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 23 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nordson might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NDSN

Nordson

Nordson Corporation engineers, manufactures, and markets products and systems to dispense, apply, and control adhesives, coatings, polymers, sealants, biomaterials, and other fluids.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor