Advertisement

- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:6278

Uncovering November 2024's Hidden Opportunities on None Exchange

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate a landscape marked by geopolitical tensions and economic uncertainty, smaller-cap indexes have shown resilience, outperforming their larger counterparts. With the S&P 600 for small-cap stocks reflecting this trend, investors are increasingly looking toward these nimble companies as potential opportunities amid broader market gains. In such an environment, identifying promising stocks involves assessing factors like strong fundamentals and innovative business models that can thrive despite external challenges.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Hubei Three Gorges Tourism Group | 11.32% | -9.98% | 7.95% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Uchida Yoko | 3.31% | 7.02% | 14.81% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| Jamuna Bank | 85.07% | 7.37% | -3.87% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| Innovana Thinklabs | 6.09% | 12.62% | 20.18% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

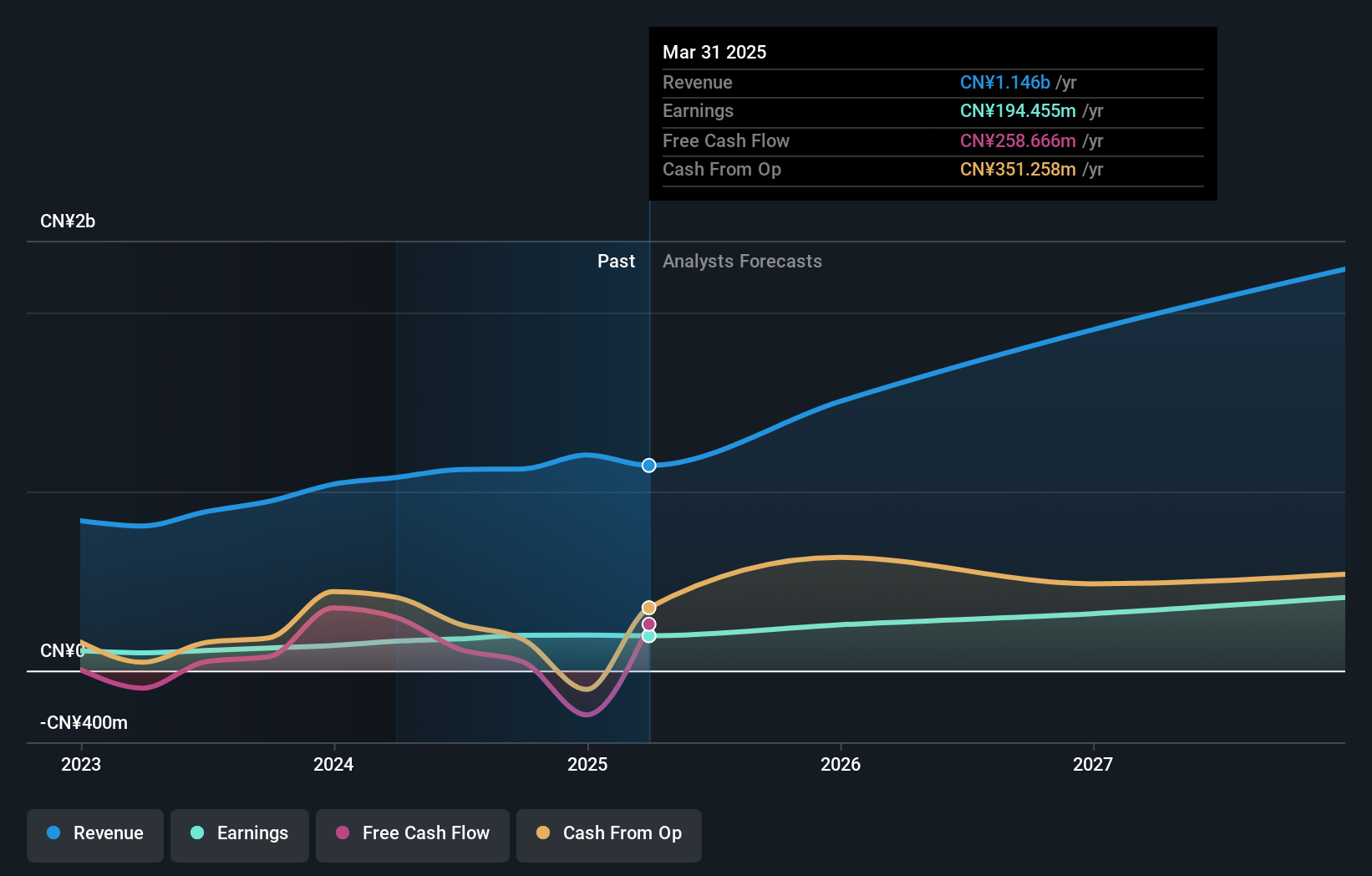

Jiangxi Guoke Defence GroupLtd (SHSE:688543)

Simply Wall St Value Rating: ★★★★★★

Overview: Jiangxi Guoke Defence Group Co., Ltd. is engaged in the research, development, production, and sale of military products with a market capitalization of CN¥8.93 billion.

Operations: Jiangxi Guoke Defence Group generates revenue primarily from its Aerospace & Defense segment, amounting to CN¥1.13 billion. The company's financial performance is influenced by the cost structure associated with this segment, impacting its profitability metrics.

Jiangxi Guoke Defence Group, a dynamic player in the defense sector, has shown impressive financial health with its debt-to-equity ratio dropping from 91.7% to just 2.7% over five years. Recent earnings reveal a robust net income of CNY 149 million for the first nine months of 2024, up from CNY 93 million last year, reflecting strong growth momentum. The company also repurchased shares worth CNY 76 million this year, signaling confidence in its future prospects. With earnings per share rising to CNY 0.85 from CNY 0.63 and being added to the S&P Global BMI Index, it seems well-positioned for continued growth.

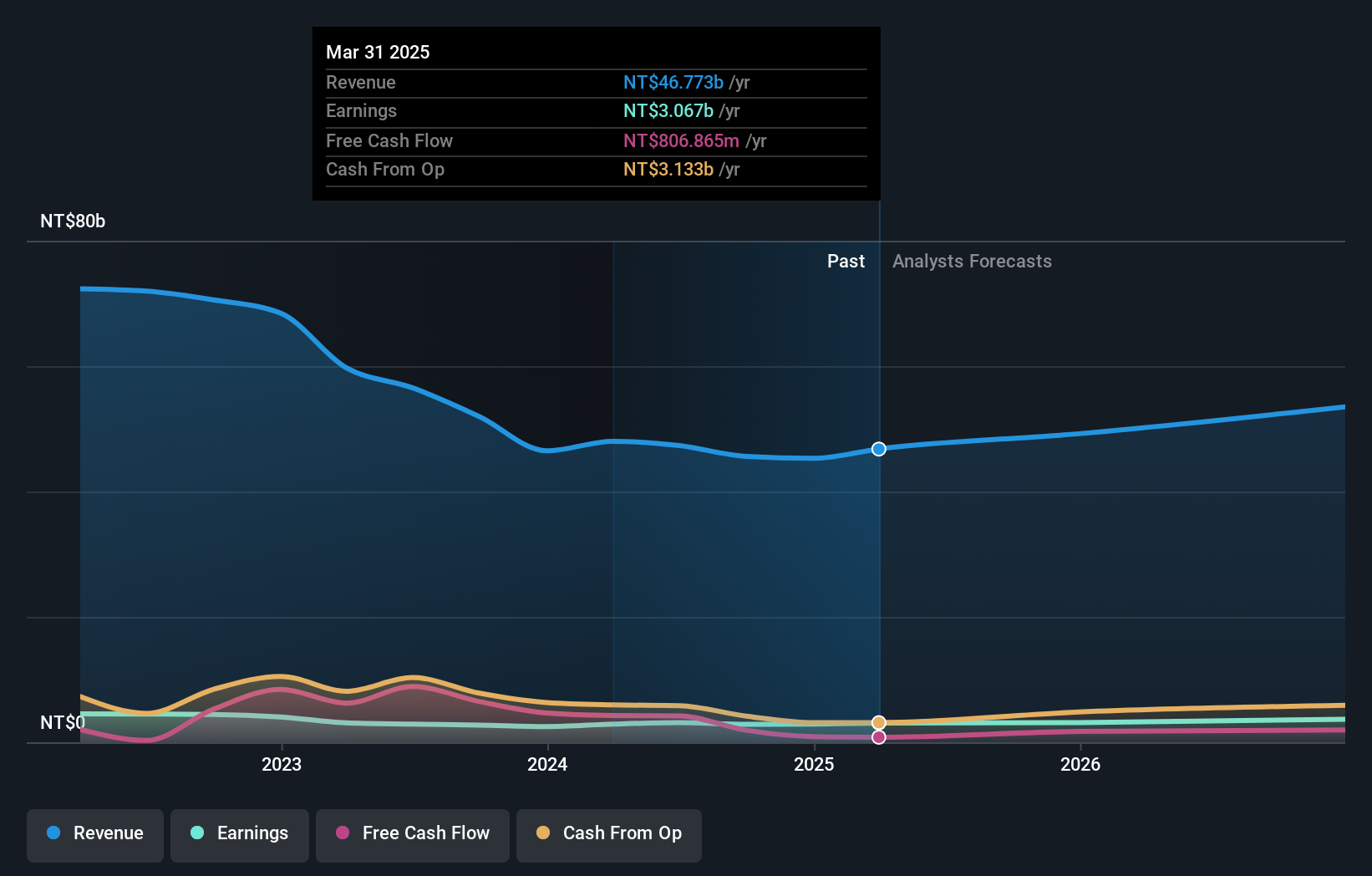

Taiwan Surface Mounting Technology (TWSE:6278)

Simply Wall St Value Rating: ★★★★★☆

Overview: Taiwan Surface Mounting Technology Corp. specializes in the design, processing, manufacturing, and trading of TFT-LCD panels, general electronic information products, and PCB surface mount packaging on a global scale with a market cap of NT$30.26 billion.

Operations: The company generates revenue primarily from its electronic components and parts segment, amounting to NT$45.60 billion.

Taiwan Surface Mounting Technology, a smaller player in its field, has shown resilience with earnings growing 9.3% annually over the past five years. Despite a challenging year where Q3 sales dipped to TWD 11 billion from TWD 12.74 billion last year, net income for the first nine months improved to TWD 2.2 billion from TWD 1.83 billion previously. The company's price-to-earnings ratio stands at an attractive 10.5x compared to the market's 21.2x, suggesting potential value for investors seeking opportunities in electronics manufacturing despite industry growth outpacing its recent performance of only 4.7%.

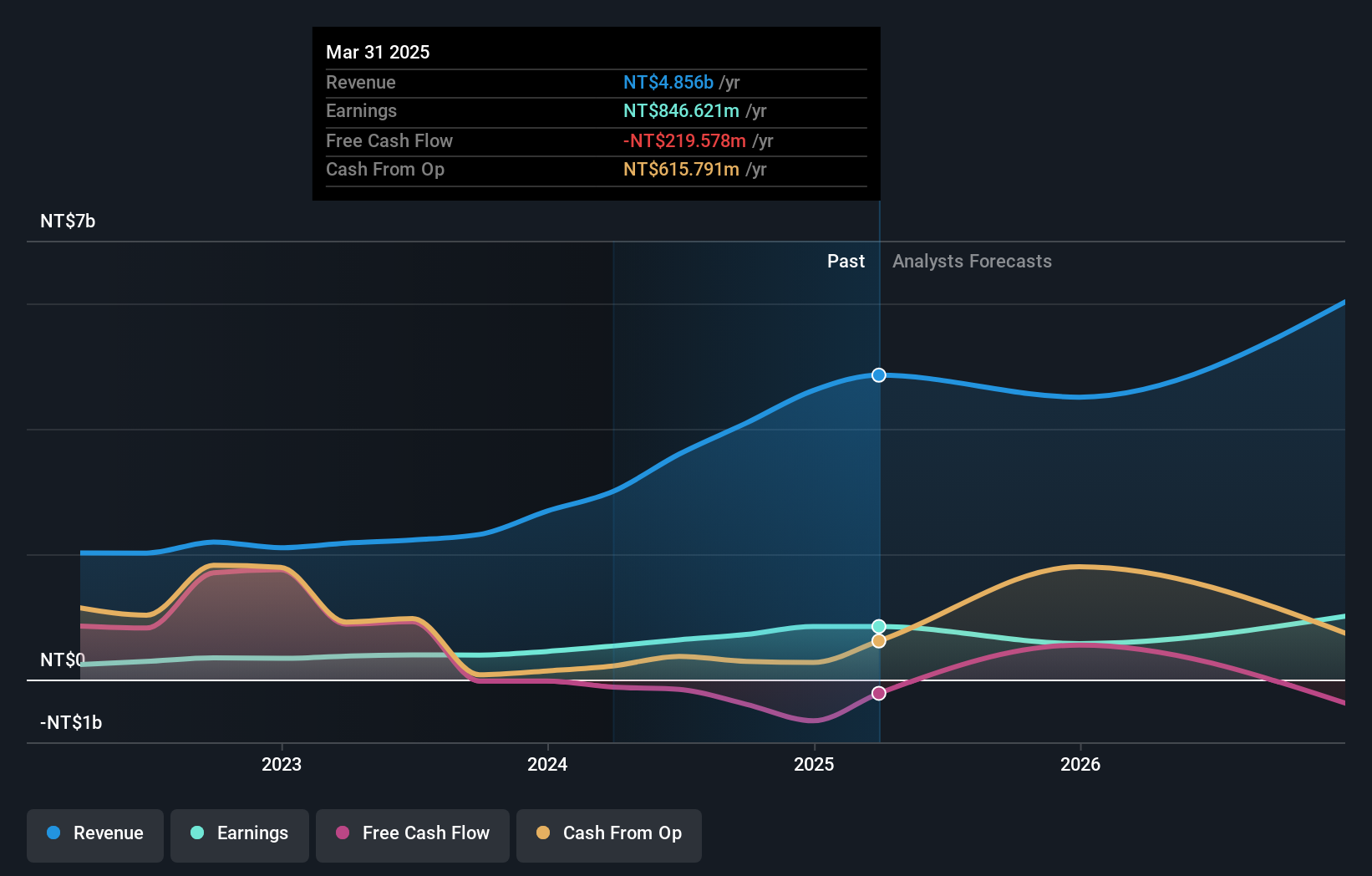

Arizon RFID Technology (Cayman) (TWSE:6863)

Simply Wall St Value Rating: ★★★★★☆

Overview: Arizon RFID Technology (Cayman) Co., Ltd. designs, develops, manufactures, and trades radio-frequency identification systems in Taiwan, China, and internationally with a market capitalization of NT$16.94 billion.

Operations: Arizon RFID Technology generates revenue primarily through the design, development, manufacturing, and trading of radio-frequency identification systems across multiple regions. The company has a market capitalization of NT$16.94 billion.

Arizon RFID Technology, a smaller player in the communications sector, has shown robust performance with its earnings soaring by 83.9% over the past year, outpacing the industry average of -9.2%. The company reported third-quarter sales of TWD 1.15 billion, significantly up from TWD 655.27 million last year, and net income rose to TWD 171.09 million from TWD 86.96 million previously. Despite high levels of non-cash earnings and a favorable price-to-earnings ratio at 23.6x compared to the industry average of 29.1x, free cash flow remains negative amid volatile share prices recently observed over three months.

Make It Happen

- Access the full spectrum of 4629 Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taiwan Surface Mounting Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6278

Taiwan Surface Mounting Technology

Engages in the design, processing, manufacturing, and trading of TFT-LCD panels, general electronic information products, and PCB surface mount packaging worldwide.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor