Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:3031

Does Bright LED Electronics Corp.'s (TWSE:3031) Weak Fundamentals Mean That The Market Could Correct Its Share Price?

Bright LED Electronics' (TWSE:3031) stock is up by a considerable 10% over the past week. However, in this article, we decided to focus on its weak fundamentals, as long-term financial performance of a business is what ultimately dictates market outcomes. In this article, we decided to focus on Bright LED Electronics' ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Bright LED Electronics

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Bright LED Electronics is:

7.7% = NT$239m ÷ NT$3.1b (Based on the trailing twelve months to September 2024).

The 'return' is the income the business earned over the last year. That means that for every NT$1 worth of shareholders' equity, the company generated NT$0.08 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Bright LED Electronics' Earnings Growth And 7.7% ROE

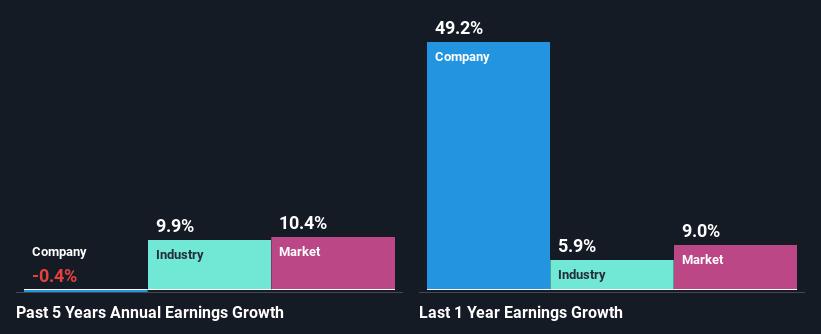

On the face of it, Bright LED Electronics' ROE is not much to talk about. A quick further study shows that the company's ROE doesn't compare favorably to the industry average of 11% either. Hence, the flat earnings seen by Bright LED Electronics over the past five years could probably be the result of it having a lower ROE.

Next, on comparing with the industry net income growth, we found that the industry grew its earnings by 9.9% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Bright LED Electronics''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Bright LED Electronics Efficiently Re-investing Its Profits?

Bright LED Electronics has a high three-year median payout ratio of 76% (or a retention ratio of 24%), meaning that the company is paying most of its profits as dividends to its shareholders. This does go some way in explaining why there's been no growth in its earnings.

Moreover, Bright LED Electronics has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth.

Conclusion

In total, we would have a hard think before deciding on any investment action concerning Bright LED Electronics. As a result of its low ROE and lack of much reinvestment into the business, the company has seen a disappointing earnings growth rate. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. You can do your own research on Bright LED Electronics and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

Valuation is complex, but we're here to simplify it.

Discover if Bright LED Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:3031

Bright LED Electronics

Manufactures and sells light-emitting diodes, indicator lights, displays, and other products in China, Taiwan, Korea, the United States, and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor