Advertisement

- Taiwan

- /

- Semiconductors

- /

- TPEX:6457

Hycon Technology Corporation's (GTSM:6457) Stock Is Going Strong: Have Financials A Role To Play?

Most readers would already be aware that Hycon Technology's (GTSM:6457) stock increased significantly by 93% over the past three months. As most would know, fundamentals are what usually guide market price movements over the long-term, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. In this article, we decided to focus on Hycon Technology's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Hycon Technology

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hycon Technology is:

27% = NT$160m ÷ NT$600m (Based on the trailing twelve months to September 2020).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.27 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

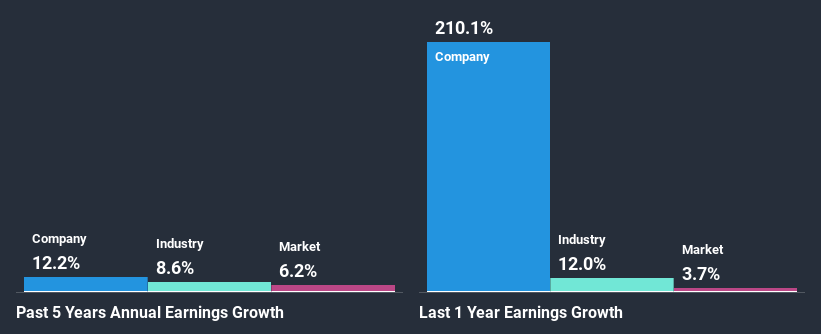

A Side By Side comparison of Hycon Technology's Earnings Growth And 27% ROE

Firstly, we acknowledge that Hycon Technology has a significantly high ROE. Second, a comparison with the average ROE reported by the industry of 11% also doesn't go unnoticed by us. Probably as a result of this, Hycon Technology was able to see a decent net income growth of 12% over the last five years.

As a next step, we compared Hycon Technology's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 8.6%.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Hycon Technology is trading on a high P/E or a low P/E, relative to its industry.

Is Hycon Technology Efficiently Re-investing Its Profits?

Hycon Technology has a very high three-year median payout ratio of 111% suggesting that the company's shareholders are getting paid from more than just the company's earnings. Still the company's earnings have grown respectably. It would still be worth keeping an eye on that high payout ratio, if for some reason the company runs into problems and business deteriorates. To know the 2 risks we have identified for Hycon Technology visit our risks dashboard for free.

Moreover, Hycon Technology is determined to keep sharing its profits with shareholders which we infer from its long history of six years of paying a dividend.

Conclusion

On the whole, we do feel that Hycon Technology has some positive attributes. Specifically, its high ROE which likely led to the growth in earnings. Bear in mind, the company reinvests little to none of its profits, which means that investors aren't necessarily reaping the full benefits of the high rate of return. So far, we've only made a quick discussion around the company's earnings growth. To gain further insights into Hycon Technology's past profit growth, check out this visualization of past earnings, revenue and cash flows.

If you’re looking to trade Hycon Technology, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hycon Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:6457

Hycon Technology

Designs, produces, and sells mixed signal microcontroller units, and battery management and touch panel ICs in Taiwan and China.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor