- Taiwan

- /

- Real Estate

- /

- TWSE:2520

Top Dividend Stocks To Consider In November 2024

Reviewed by Simply Wall St

In a week marked by busy earnings reports and fluctuating economic signals, global markets have shown mixed results, with major U.S. indices like the Nasdaq Composite and S&P MidCap 400 hitting record highs before retreating. As investors navigate this tumultuous landscape, dividend stocks stand out as a potential source of stability and income, offering consistent returns even amid market volatility.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Tsubakimoto Chain (TSE:6371) | 4.25% | ★★★★★★ |

| Mitsubishi Shokuhin (TSE:7451) | 3.85% | ★★★★★★ |

| Guaranty Trust Holding (NGSE:GTCO) | 6.72% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.06% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.45% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.20% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.62% | ★★★★★★ |

| Business Brain Showa-Ota (TSE:9658) | 4.18% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.63% | ★★★★★★ |

| DoshishaLtd (TSE:7483) | 3.83% | ★★★★★★ |

Click here to see the full list of 2017 stocks from our Top Dividend Stocks screener.

We're going to check out a few of the best picks from our screener tool.

Shanghai Sinotec (SHSE:603121)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Shanghai Sinotec Co., Ltd. is a company that develops, produces, and sells auto parts in China with a market capitalization of CN¥3.01 billion.

Operations: Shanghai Sinotec Co., Ltd.'s revenue segments are not provided in the text.

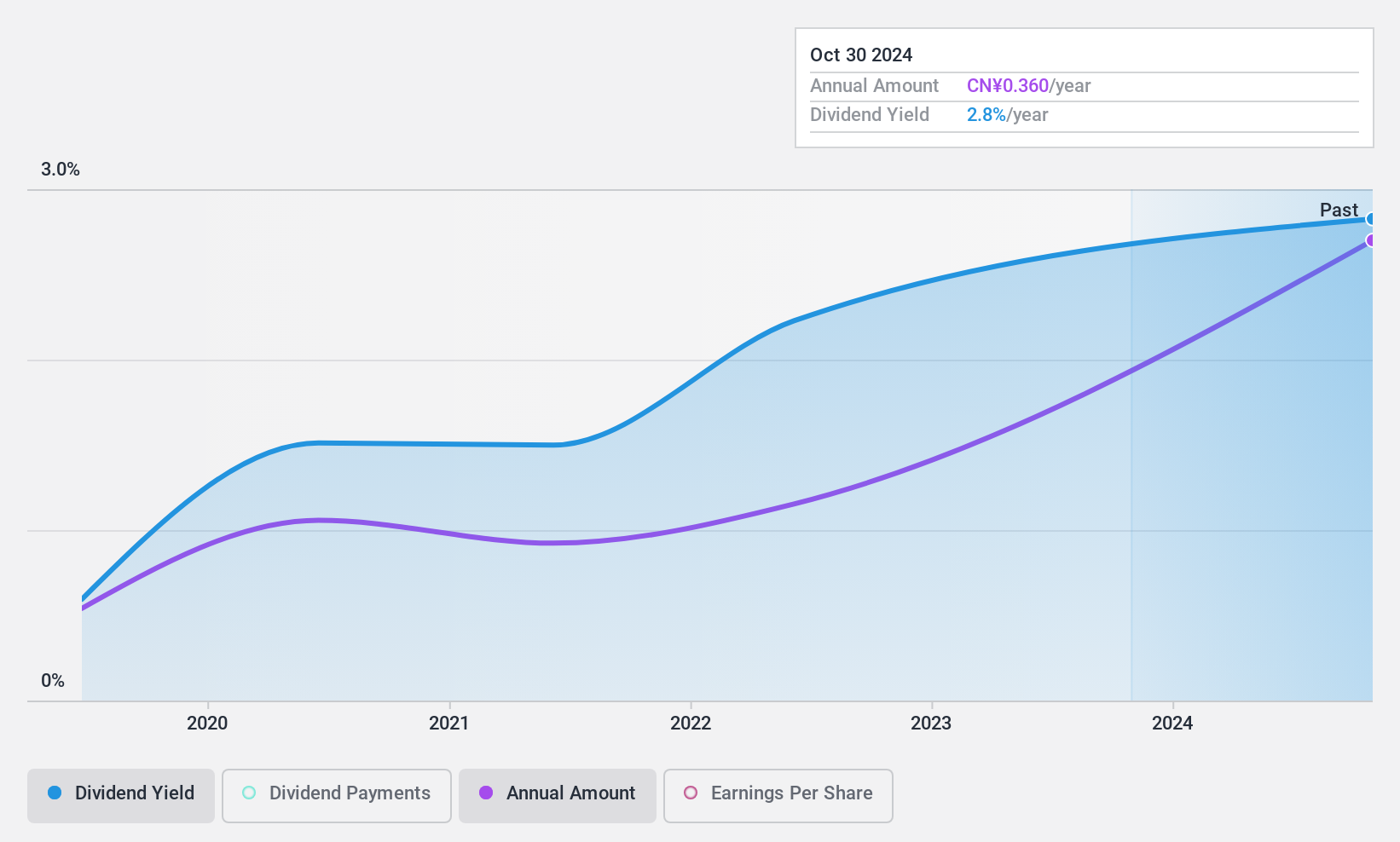

Dividend Yield: 4%

Shanghai Sinotec's dividend payments are covered by earnings and cash flows, with a payout ratio of 66.7% and a cash payout ratio of 79.4%, respectively. Despite being in the top 25% for dividend yield in China, the company's dividends have been unstable and volatile over its five-year history of payments. Recent financials show net income declined to CNY 71.24 million from CNY 96.53 million year-over-year, potentially affecting future dividend stability.

- Click to explore a detailed breakdown of our findings in Shanghai Sinotec's dividend report.

- The valuation report we've compiled suggests that Shanghai Sinotec's current price could be inflated.

HBIS Resources (SZSE:000923)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: HBIS Resources Co., Ltd. is involved in the mining, processing, selling, and servicing of mineral products across Asia, Africa, Europe, and the Americas with a market capitalization of CN¥10.40 billion.

Operations: HBIS Resources Co., Ltd. generates revenue through its operations in mining, processing, and selling mineral products across multiple continents including Asia, Africa, Europe, and the Americas.

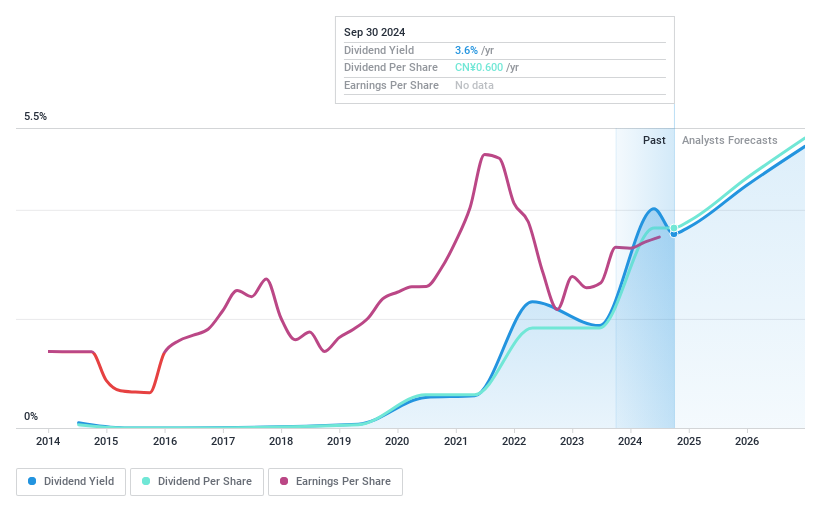

Dividend Yield: 3.8%

HBIS Resources offers a dividend yield in the top 25% of the Chinese market, with a payout ratio of 47.6% indicating dividends are well-covered by earnings. Despite this, its dividend history is marked by volatility and instability over the past decade. Recent financials show an increase in sales to CNY 4.65 billion for nine months ending September 2024, but net income declined to CNY 577.59 million from CNY 666.77 million year-over-year, which may impact future payouts.

- Delve into the full analysis dividend report here for a deeper understanding of HBIS Resources.

- The valuation report we've compiled suggests that HBIS Resources' current price could be quite moderate.

Kindom Development (TWSE:2520)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Kindom Development Co., Ltd., along with its subsidiaries, engages in the construction, development, and sale of real estate properties in Taiwan and has a market cap of NT$25.66 billion.

Operations: Kindom Development Co., Ltd. generates revenue through its Manufacturing segment (NT$5.76 billion), Department Store operations (NT$1.74 billion), and Construction Segments (NT$21.75 billion).

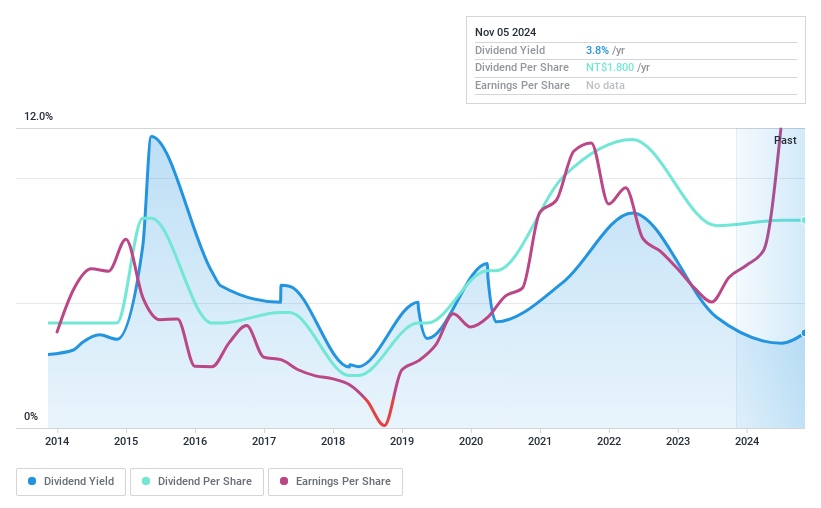

Dividend Yield: 3.8%

Kindom Development's dividends are well-supported by earnings and cash flows, with payout ratios of 20.1% and 15.5%, respectively. However, its dividend history has been volatile over the past decade despite recent earnings growth of 180.1%. The company trades at a significant discount to its estimated fair value but offers a lower yield (3.81%) compared to top-tier Taiwanese dividend payers (4.43%). Recent developments include new urban regeneration projects in Taipei valued at approximately NT$7.62 billion.

- Get an in-depth perspective on Kindom Development's performance by reading our dividend report here.

- Insights from our recent valuation report point to the potential undervaluation of Kindom Development shares in the market.

Next Steps

- Access the full spectrum of 2017 Top Dividend Stocks by clicking on this link.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kindom Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2520

Kindom Development

Kindom Development Co., Ltd., together with its subsidiaries, constructs, develops, and sells real estate properties in Taiwan.

Outstanding track record with flawless balance sheet and pays a dividend.