Despite shrinking by NT$1.1b in the past week, Taita Chemical Company (TWSE:1309) shareholders are still up 116% over 5 years

It's been a soft week for Taita Chemical Company, Limited (TWSE:1309) shares, which are down 14%. But at least the stock is up over the last five years. However we are not very impressed because the share price is only up 80%, less than the market return of 134%. Unfortunately not all shareholders will have held it for five years, so spare a thought for those caught in the 50% decline over the last three years: that's a long time to wait for profits.

While this past week has detracted from the company's five-year return, let's look at the recent trends of the underlying business and see if the gains have been in alignment.

Check out our latest analysis for Taita Chemical Company

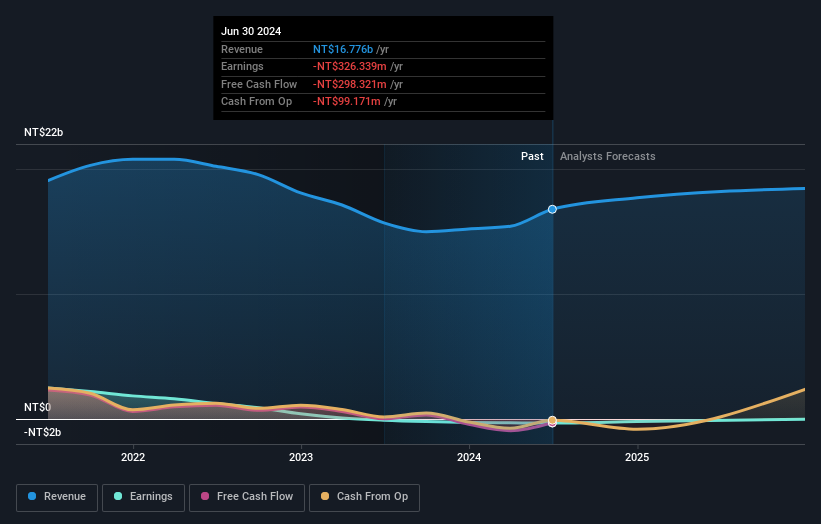

Because Taita Chemical Company made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. When a company doesn't make profits, we'd generally hope to see good revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

Over the last half decade Taita Chemical Company's revenue has actually been trending down at about 1.5% per year. The falling revenue is arguably somewhat reflected in the lacklustre return of 13% per year over that time. Arguably that's not bad given the soft revenue and loss-making position. Of course, a closer look at the bottom line - and any available analyst forecasts - could reveal an opportunity (if they point to future growth).

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

This free interactive report on Taita Chemical Company's balance sheet strength is a great place to start, if you want to investigate the stock further.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, Taita Chemical Company's TSR for the last 5 years was 116%, which exceeds the share price return mentioned earlier. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

Investors in Taita Chemical Company had a tough year, with a total loss of 2.3% (including dividends), against a market gain of about 35%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 17% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Even so, be aware that Taita Chemical Company is showing 2 warning signs in our investment analysis , and 1 of those is significant...

Of course Taita Chemical Company may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Taiwanese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Taita Chemical Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1309

Taita Chemical Company

Engages in the production and sale of styrenics in Taiwan, Hong Kong, Mainland China, Southeastern/Central Asia, Europe, and North America.

Adequate balance sheet and fair value.