- Taiwan

- /

- Basic Materials

- /

- TWSE:1101

We Wouldn't Be Too Quick To Buy TCC Group Holdings Co., Ltd. (TWSE:1101) Before It Goes Ex-Dividend

TCC Group Holdings Co., Ltd. (TWSE:1101) is about to trade ex-dividend in the next 4 days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least two business day to settle. Thus, you can purchase TCC Group Holdings' shares before the 1st of July in order to receive the dividend, which the company will pay on the 26th of July.

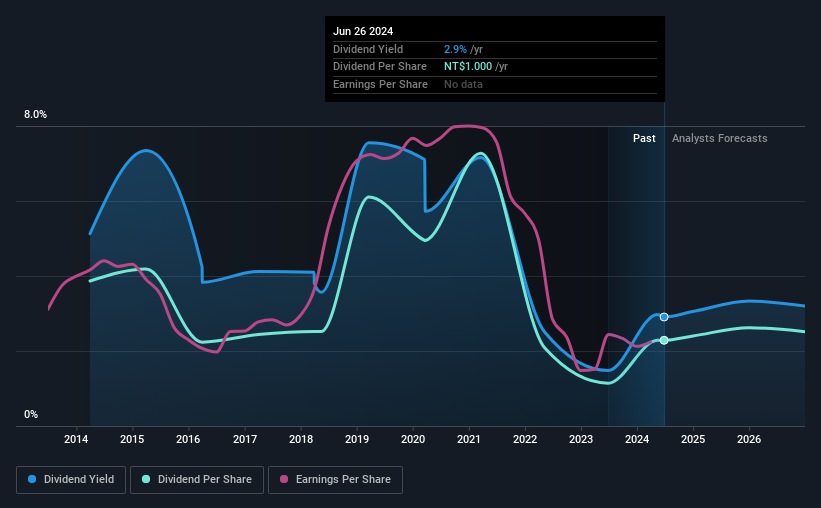

The company's upcoming dividend is NT$1.00 a share, following on from the last 12 months, when the company distributed a total of NT$1.00 per share to shareholders. Based on the last year's worth of payments, TCC Group Holdings has a trailing yield of 2.9% on the current stock price of NT$34.40. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! As a result, readers should always check whether TCC Group Holdings has been able to grow its dividends, or if the dividend might be cut.

Check out our latest analysis for TCC Group Holdings

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Its dividend payout ratio is 89% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. It could become a concern if earnings started to decline. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out an unsustainably high 308% of its free cash flow as dividends over the past 12 months, which is worrying. Unless there were something in the business we're not grasping, this could signal a risk that the dividend may have to be cut in the future.

While TCC Group Holdings's dividends were covered by the company's reported profits, cash is somewhat more important, so it's not great to see that the company didn't generate enough cash to pay its dividend. Cash is king, as they say, and were TCC Group Holdings to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings fall far enough, the company could be forced to cut its dividend. With that in mind, we're discomforted by TCC Group Holdings's 21% per annum decline in earnings in the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. TCC Group Holdings has seen its dividend decline 5.1% per annum on average over the past 10 years, which is not great to see. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

The Bottom Line

Has TCC Group Holdings got what it takes to maintain its dividend payments? It's definitely not great to see earnings per share shrinking. The company paid out an acceptable percentage of its income, but an uncomfortably high percentage of its cash flow over the past year. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

With that in mind though, if the poor dividend characteristics of TCC Group Holdings don't faze you, it's worth being mindful of the risks involved with this business. In terms of investment risks, we've identified 2 warning signs with TCC Group Holdings and understanding them should be part of your investment process.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if TCC Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1101

TCC Group Holdings

Engages in the production and sale of cement and ready-mix concrete in Taiwan.

Fair value with moderate growth potential.