Advertisement

- Taiwan

- /

- Healthcare Services

- /

- TPEX:6496

Here's Why Excelsior Biopharma's (GTSM:6496) Statutory Earnings Are Arguably Too Conservative

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. Today we'll focus on whether this year's statutory profits are a good guide to understanding Excelsior Biopharma (GTSM:6496).

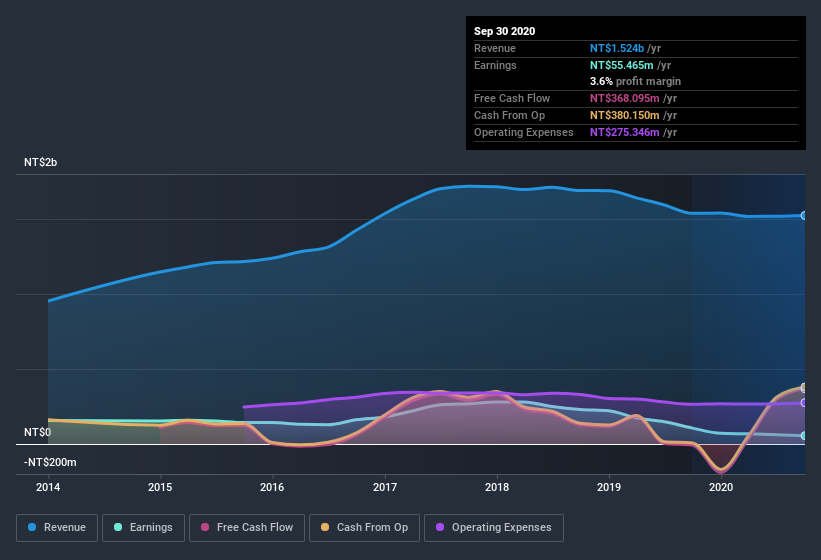

While Excelsior Biopharma was able to generate revenue of NT$1.52b in the last twelve months, we think its profit result of NT$55.5m was more important. Below, you can see that both its revenue and its profit have fallen over the last three years.

See our latest analysis for Excelsior Biopharma

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. As a result, we think it's well worth considering what Excelsior Biopharma's cashflow (when compared to its earnings) can tell us about the nature of its statutory profit. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Excelsior Biopharma.

A Closer Look At Excelsior Biopharma's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to September 2020, Excelsior Biopharma had an accrual ratio of -0.50. Therefore, its statutory earnings were very significantly less than its free cashflow. To wit, it produced free cash flow of NT$368m during the period, dwarfing its reported profit of NT$55.5m. Given that Excelsior Biopharma had negative free cash flow in the prior corresponding period, the trailing twelve month resul of NT$368m would seem to be a step in the right direction.

Our Take On Excelsior Biopharma's Profit Performance

Happily for shareholders, Excelsior Biopharma produced plenty of free cash flow to back up its statutory profit numbers. Based on this observation, we consider it possible that Excelsior Biopharma's statutory profit actually understates its earnings potential! On the other hand, its EPS actually shrunk in the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you want to do dive deeper into Excelsior Biopharma, you'd also look into what risks it is currently facing. To that end, you should learn about the 3 warning signs we've spotted with Excelsior Biopharma (including 1 which is a bit concerning).

This note has only looked at a single factor that sheds light on the nature of Excelsior Biopharma's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Excelsior Biopharma, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Excelsior Biopharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:6496

Excelsior Biopharma

Develops and sells pharmaceutical products in Taiwan, China, and internationally.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor