Advertisement

- China

- /

- Aerospace & Defense

- /

- SHSE:688510

Undiscovered Gems With Strong Fundamentals To Explore This January 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets show signs of recovery, with cooling inflation and robust bank earnings propelling U.S. stocks higher, investors are increasingly optimistic about the potential for rate cuts later in the year. This positive sentiment is reflected in key indices like the S&P MidCap 400 and Russell 2000, which have posted significant gains amid easing inflationary pressures and strong corporate performance. In this environment, identifying stocks with solid fundamentals becomes crucial as they may offer stability and growth opportunities even amidst broader market fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Marítima de Inversiones | NA | 82.67% | 21.14% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| SALUS Ljubljana d. d | 13.55% | 13.11% | 9.95% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Industrias del Cobre Sociedad Anónima | NA | 19.08% | 22.33% | ★★★★★★ |

| MAPFRE Middlesea | NA | 14.56% | 1.77% | ★★★★★☆ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

| BOSQAR d.d | 94.35% | 39.11% | 23.56% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

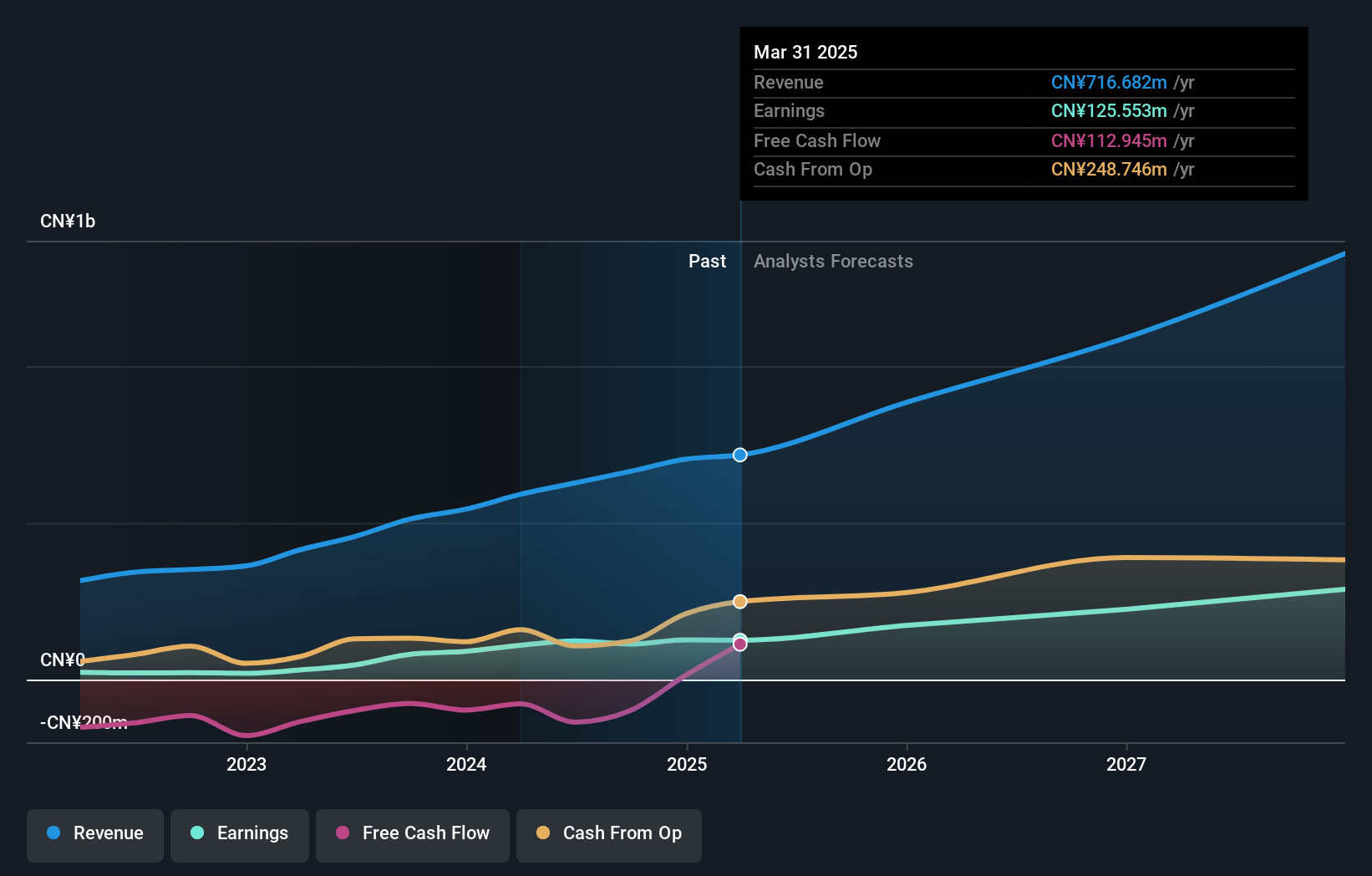

Wuxi HyatechLtd (SHSE:688510)

Simply Wall St Value Rating: ★★★★★☆

Overview: Wuxi Hyatech Co., Ltd. is engaged in the research, development, manufacturing, and sale of aero-engine parts and forged medical orthopedic implants both in China and internationally, with a market capitalization of CN¥4.05 billion.

Operations: Wuxi Hyatech generates revenue primarily from the sale of aero-engine parts and forged medical orthopedic implants. The company's financial performance can be analyzed through its market capitalization, which stands at CN¥4.05 billion.

Wuxi Hyatech showcases promising growth with earnings climbing by 40.5% over the past year, outpacing the Aerospace & Defense industry’s -13.4%. The company reported sales of CNY 520.07 million for nine months ending September 30, 2024, an increase from CNY 399.31 million the previous year, while net income reached CNY 92.75 million compared to CNY 69.48 million a year ago. With a price-to-earnings ratio of 35.7x below industry average and satisfactory net debt to equity ratio at 1.8%, it seems well-positioned despite its free cash flow challenges and rising debt-to-equity ratio from 12.9% to 20% over five years.

- Click to explore a detailed breakdown of our findings in Wuxi HyatechLtd's health report.

Review our historical performance report to gain insights into Wuxi HyatechLtd's's past performance.

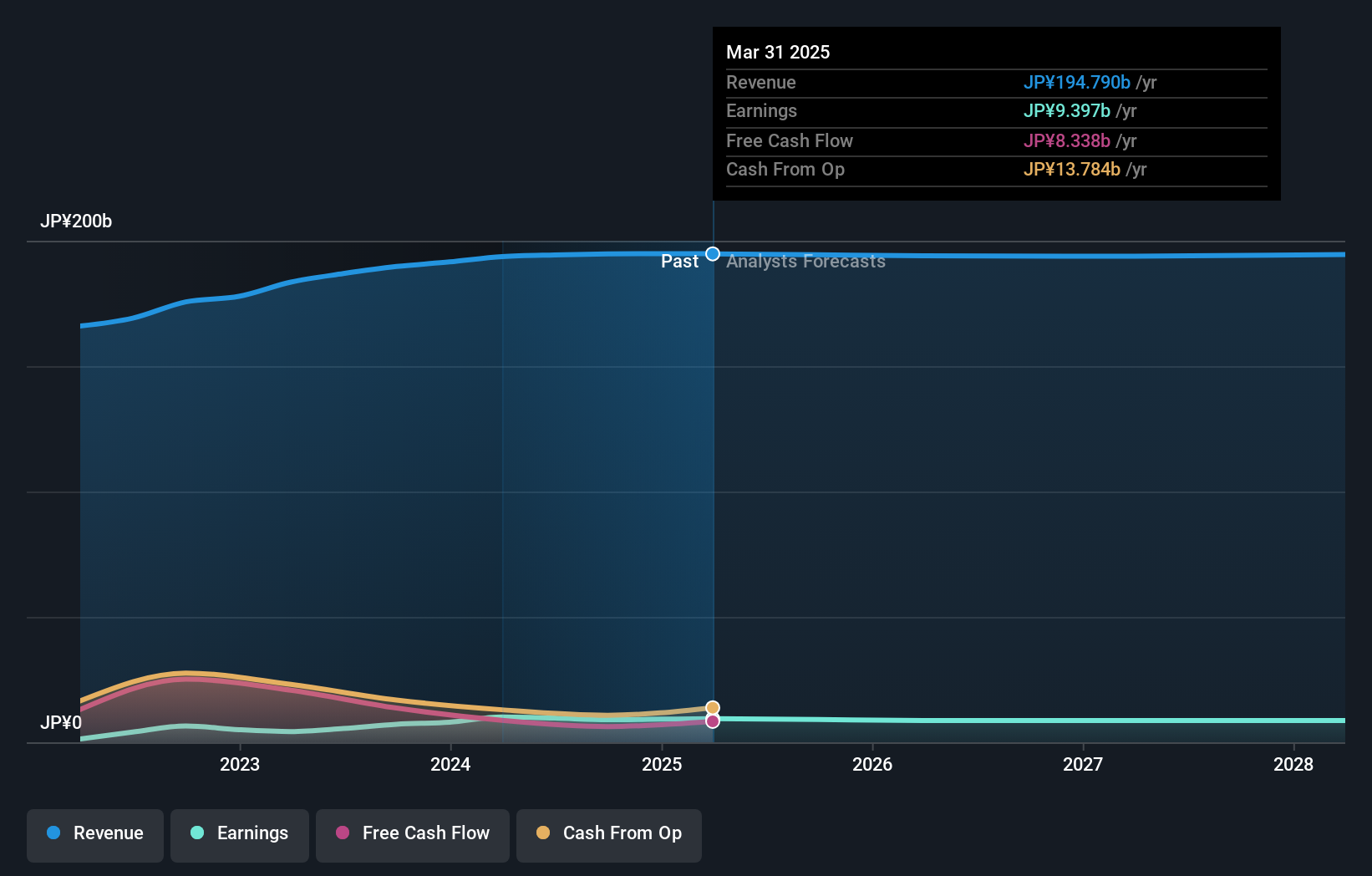

Aoyama Trading (TSE:8219)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Aoyama Trading Co., Ltd. operates in Japan, focusing on business wear, credit card services, printing and media, sundry sales, repair services, and franchisee operations with a market capitalization of ¥107.54 billion.

Operations: Aoyama Trading generates revenue primarily from its business wear segment, which contributes ¥133.02 billion, followed by franchisee operations at ¥15.67 billion and miscellaneous goods sales at ¥15.21 billion. The company also earns from its printing/media and comprehensive repair services segments, with revenues of ¥11.42 billion and ¥14.11 billion respectively. Notably, the net profit margin reflects a significant aspect of its financial performance over recent periods without being explicitly stated here due to data constraints in this summary format.

Aoyama Trading, a notable player in the retail sector, showcases robust financial health with interest payments well covered by EBIT at 83 times. Despite an increase in the debt-to-equity ratio from 44% to 52% over five years, its net debt to equity remains satisfactory at 9%. The company's earnings growth of 25% outpaced its industry peers' average of nearly 6%, indicating strong performance. Recent buybacks saw ¥3 billion spent on repurchasing shares, enhancing shareholder value. With a P/E ratio of 12x below Japan's market average and high-quality past earnings, Aoyama offers compelling value for investors.

- Take a closer look at Aoyama Trading's potential here in our health report.

Assess Aoyama Trading's past performance with our detailed historical performance reports.

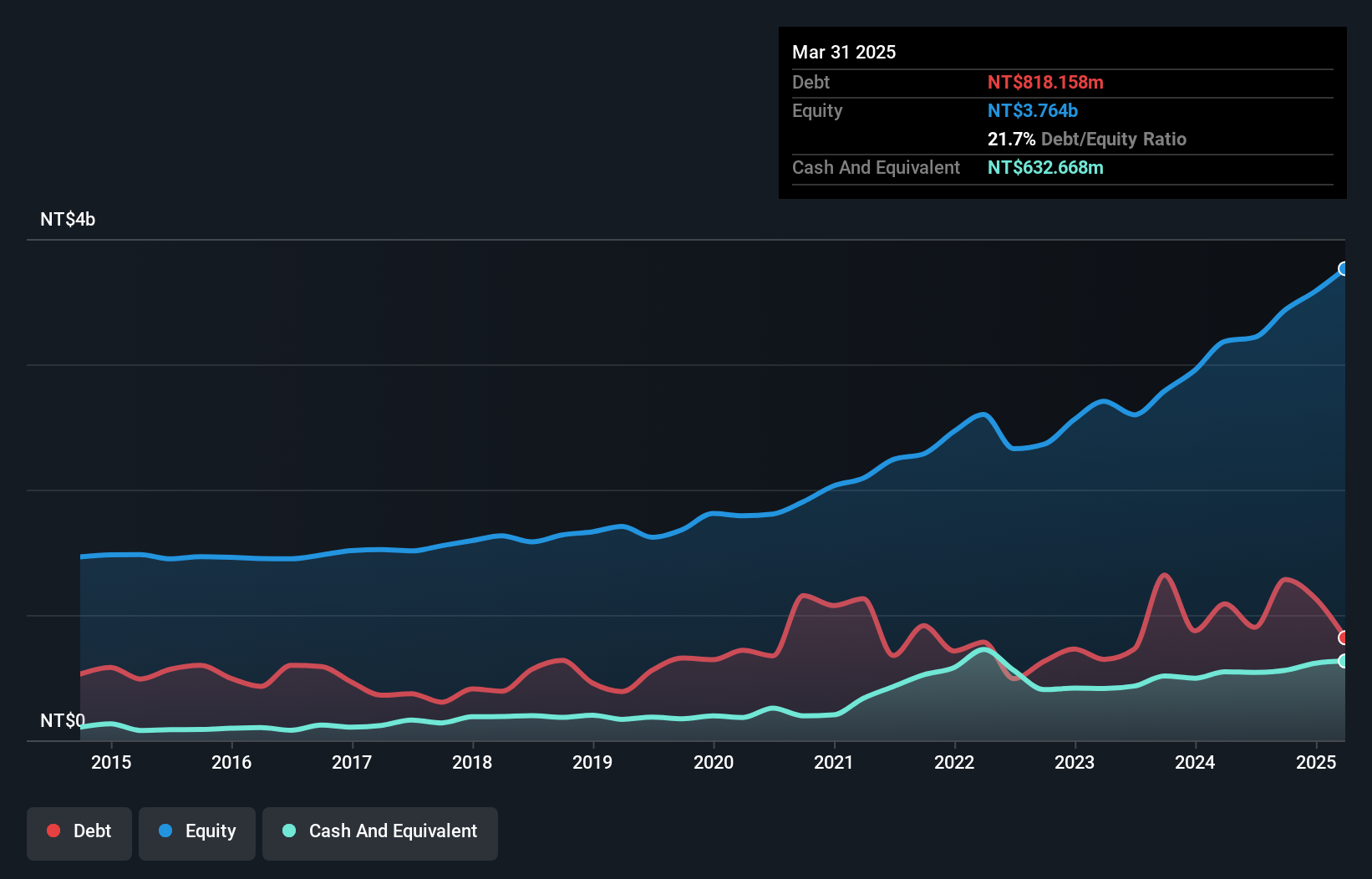

Dah San Electric Wire & Cable (TWSE:1615)

Simply Wall St Value Rating: ★★★★★★

Overview: Dah San Electric Wire & Cable Corp. specializes in manufacturing and selling power cables, communication cables, electronic wires, and bare copper wires with a market capitalization of NT$10.92 billion.

Operations: Dah San Electric Wire & Cable generates revenue primarily from its Wire and Cable Department, amounting to NT$5.27 billion.

Dah San Electric Wire & Cable has shown impressive growth, with earnings rising by 37.8% over the past year, outpacing the Electrical industry's 6.1%. The company's net debt to equity ratio is a satisfactory 21.1%, reflecting its solid financial footing. Recent figures reveal third-quarter sales of TWD 1.68 billion, up from TWD 1.44 billion last year, while net income climbed to TWD 213.97 million from TWD 173.48 million previously, indicating robust performance and profitability in a competitive market environment despite challenges that may arise from capital expenditures and changes in working capital dynamics.

- Navigate through the intricacies of Dah San Electric Wire & Cable with our comprehensive health report here.

Understand Dah San Electric Wire & Cable's track record by examining our Past report.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 4651 Undiscovered Gems With Strong Fundamentals now.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wuxi HyatechLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688510

Wuxi HyatechLtd

Research, develops, manufactures, and sells aero-engine parts and forged medical orthopedic implants in China and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor