Earnings Beat: AirTAC International Group Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

AirTAC International Group (TPE:1590) just released its quarterly report and things are looking bullish. AirTAC International Group delivered a significant beat to revenue and earnings per share (EPS) expectations, with sales hitting NT$5.9b and statutory EPS reaching NT$7.65, both beating estimates by more than 10%. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

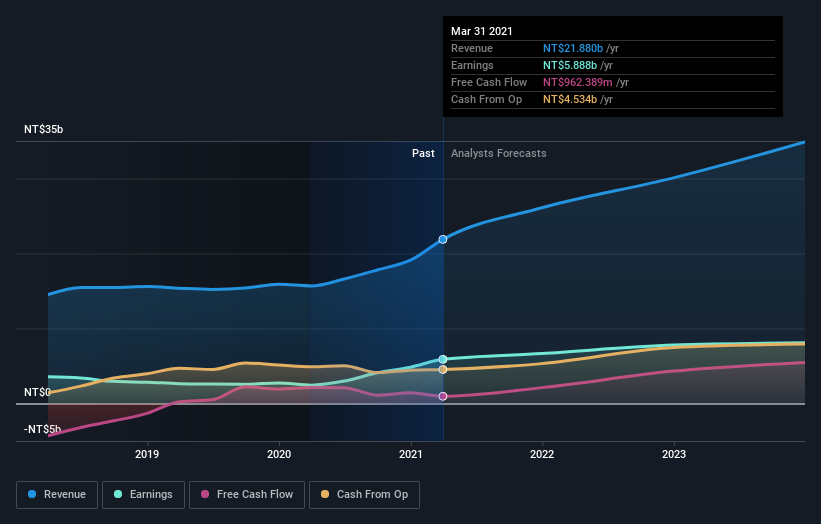

See our latest analysis for AirTAC International Group

Taking into account the latest results, the most recent consensus for AirTAC International Group from 14 analysts is for revenues of NT$26.1b in 2021 which, if met, would be a notable 19% increase on its sales over the past 12 months. Statutory earnings per share are predicted to swell 12% to NT$34.85. Yet prior to the latest earnings, the analysts had been anticipated revenues of NT$24.5b and earnings per share (EPS) of NT$32.03 in 2021. So there seems to have been a moderate uplift in sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

Despite these upgrades,the analysts have not made any major changes to their price target of NT$1,364, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on AirTAC International Group, with the most bullish analyst valuing it at NT$1,590 and the most bearish at NT$865 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. The analysts are definitely expecting AirTAC International Group's growth to accelerate, with the forecast 26% annualised growth to the end of 2021 ranking favourably alongside historical growth of 14% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 16% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that AirTAC International Group is expected to grow much faster than its industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around AirTAC International Group's earnings potential next year. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on AirTAC International Group. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple AirTAC International Group analysts - going out to 2023, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 1 warning sign for AirTAC International Group you should be aware of.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1590

Airtac International Group

Manufactures and sells pneumatic control components worldwide.

Flawless balance sheet, good value and pays a dividend.