Discovering November 2024's Undiscovered Gems with Promising Potential

Reviewed by Simply Wall St

In the wake of a significant political shift in the U.S., global markets have reacted strongly, with major indices reaching record highs and small-cap stocks showing notable gains. The Russell 2000 Index's recent surge reflects investor optimism around anticipated economic growth and regulatory changes under a new administration. In this dynamic environment, identifying promising stocks involves looking for companies that can leverage favorable policy shifts and demonstrate resilience amidst evolving market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Interactive Digital Technologies | 9.01% | 4.39% | 3.03% | ★★★★★☆ |

| Bakrie & Brothers | 22.66% | 7.78% | 13.50% | ★★★★★☆ |

| S J Logistics (India) | 34.96% | 59.89% | 51.25% | ★★★★★☆ |

| Billion Industrial Holdings | 3.63% | 18.00% | -11.38% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

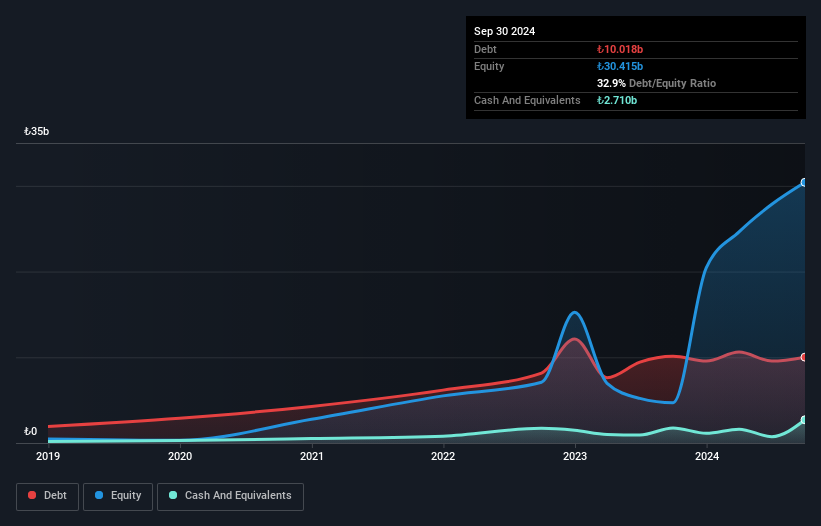

Akfen Yenilenebilir Enerji (IBSE:AKFYE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Akfen Yenilenebilir Enerji is involved in the production of renewable energy in Turkey, with a market cap of TRY17.98 billion.

Operations: Akfen Yenilenebilir Enerji generates revenue primarily from its renewable energy production activities in Turkey. The company has a market capitalization of TRY17.98 billion, reflecting its significant presence in the industry.

Akfen Yenilenebilir Enerji, with a notable reduction in its debt to equity ratio from 762.4% to 32.9% over five years, presents an intriguing profile within the renewable energy sector. The company's net debt to equity ratio stands at a satisfactory 24%, and its price-to-earnings ratio of 4.4x is significantly lower than the TR market average of 14.3x, suggesting potential value for investors. Despite becoming profitable this year, recent earnings reports show challenges; third-quarter sales were TRY 1,083 million compared to TRY 1,592 million last year, with a net loss of TRY 149 million versus a previous profit of TRY 21 million.

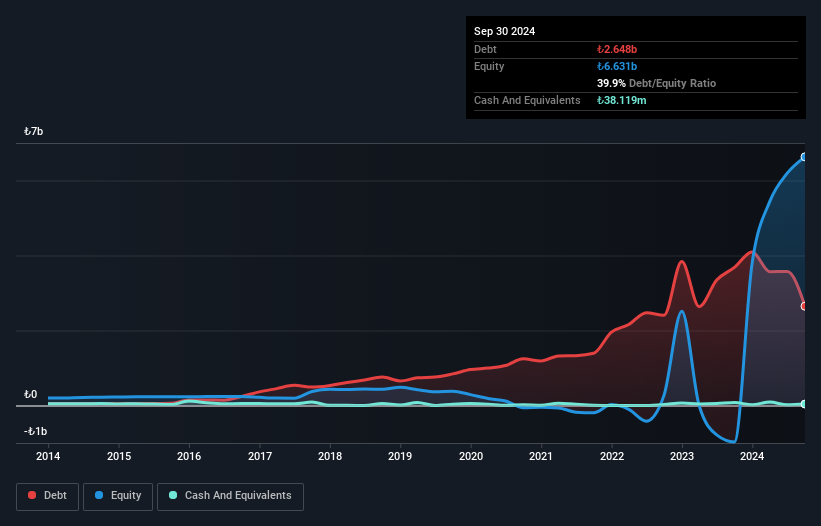

Batisöke Söke Çimento Sanayii T.A.S (IBSE:BSOKE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Batisöke Söke Çimento Sanayii T.A.S. is a Turkish company involved in the production and sale of cement and clinker products, with a market capitalization of TRY19.99 billion.

Operations: BSOKE generates revenue primarily from the sale of cement, amounting to TRY3.12 billion.

Batişöke has shown resilience with its net debt to equity ratio now at a satisfactory 39.4%, down from 220.6% over five years, reflecting improved financial health. Despite recent volatility in its share price, the company has turned profitable this year, marking a significant turnaround from previous losses. Its price-to-earnings ratio of 13.7x is attractive compared to the TR market average of 14.3x, suggesting potential undervaluation in the market's eyes. However, challenges remain as third-quarter sales dropped to TRY 785 million from TRY 1,073 million last year and reported a net loss of TRY 118 million for the same period.

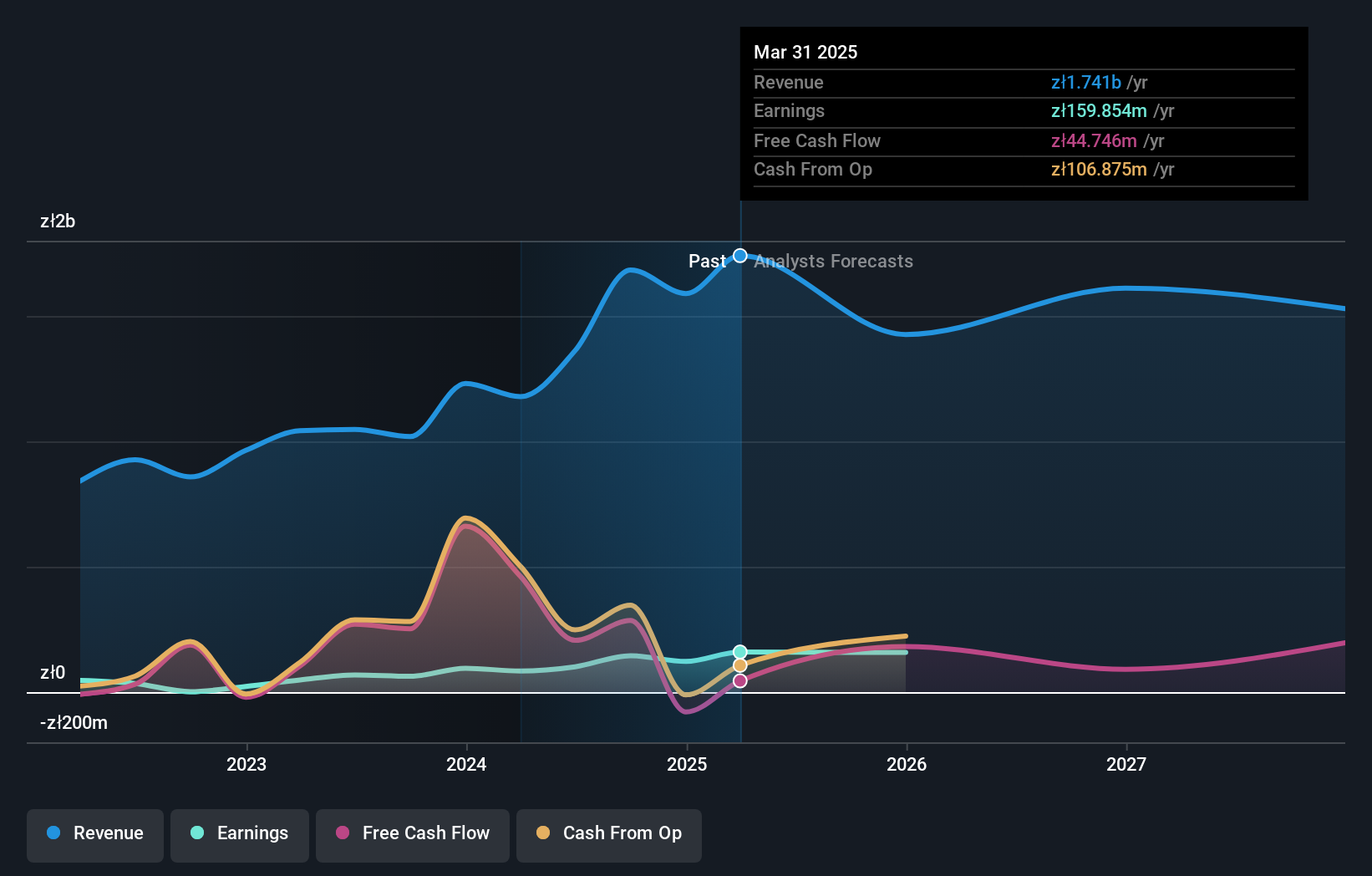

Newag (WSE:NWG)

Simply Wall St Value Rating: ★★★★★★

Overview: Newag S.A. is a company involved in the production and sale of railway locomotives and rolling stock in Poland, with a market capitalization of PLN1.61 billion.

Operations: Newag generates revenue primarily from repair services, modernization of rolling stock, and production of rolling stock and control systems, amounting to PLN1.44 billion. Activities of financial holdings contribute an additional PLN84.19 million to its revenue streams.

Newag's financial performance has been notable, with earnings surging 47% last year, outpacing the machinery industry's modest 0.4% growth. The company's cash position comfortably exceeds its total debt, and interest payments are well-covered by EBIT at a ratio of 15.3 times. Over five years, Newag's debt to equity ratio impressively dropped from 63% to 14%. Recent results show robust sales growth to PLN 352 million in Q2 from PLN 168 million a year prior, while net income rose to PLN 31.7 million from PLN 14.64 million, reflecting strong operational momentum and enhanced profitability prospects moving forward.

- Get an in-depth perspective on Newag's performance by reading our health report here.

Evaluate Newag's historical performance by accessing our past performance report.

Make It Happen

- Investigate our full lineup of 4643 Undiscovered Gems With Strong Fundamentals right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Newag might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About WSE:NWG

Newag

Engages in the production and sale of railway locomotives and rolling stocks in Poland.

Flawless balance sheet with proven track record.