Seatrium Leads These 3 SGX Stocks That Could Be Trading Below Fair Value

Reviewed by Simply Wall St

The Singapore stock market has been experiencing a mixed performance recently, with some sectors showing resilience amid global economic uncertainties. In such an environment, identifying undervalued stocks can be a strategic move for investors seeking potential growth opportunities. A good stock in this context is one that demonstrates strong fundamentals and may be trading below its intrinsic value due to temporary market inefficiencies.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Singapore Technologies Engineering (SGX:S63) | SGD4.41 | SGD7.36 | 40.1% |

| LHN (SGX:41O) | SGD0.34 | SGD0.41 | 17.5% |

| Digital Core REIT (SGX:DCRU) | US$0.58 | US$0.82 | 29.2% |

| Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD1.10 | SGD2.15 | 48.9% |

| Nanofilm Technologies International (SGX:MZH) | SGD0.775 | SGD1.42 | 45.5% |

| Seatrium (SGX:5E2) | SGD1.56 | SGD2.90 | 46.1% |

Here we highlight a subset of our preferred stocks from the screener.

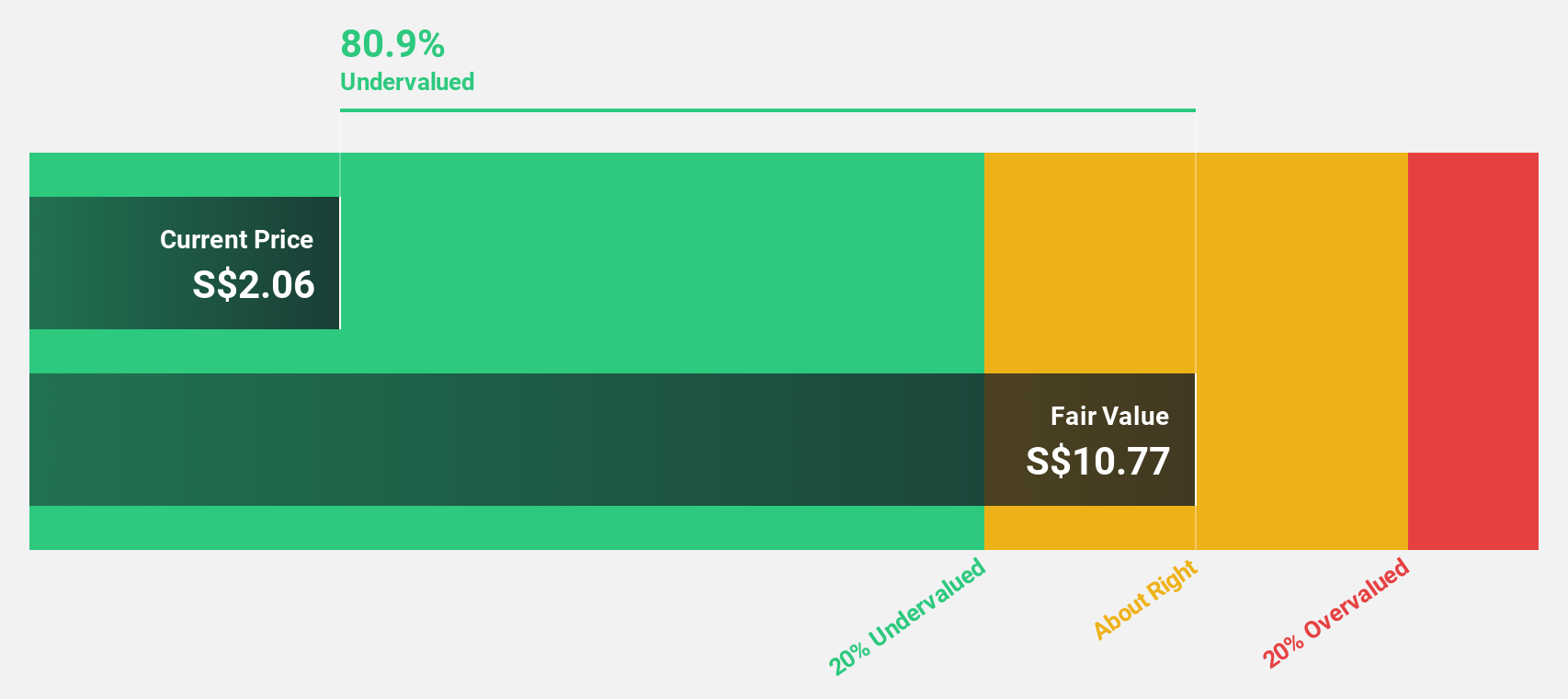

Seatrium (SGX:5E2)

Overview: Seatrium Limited offers engineering solutions to the offshore, marine, and energy industries and has a market cap of SGD5.31 billion.

Operations: The company's revenue segments include Ship Chartering, which generated SGD24.71 million, and Rigs & Floaters, Repairs & Upgrades, Offshore Platforms and Specialised Shipbuilding, contributing SGD8.39 billion.

Estimated Discount To Fair Value: 46.1%

Seatrium Limited appears significantly undervalued based on cash flows, trading at 46.1% below its estimated fair value of S$2.9. The company has demonstrated strong project execution capabilities, evidenced by the early delivery of the Vali jackup rig and a substantial contract win for an offshore transmission system with TenneT. Despite facing regulatory scrutiny, Seatrium's recent return to profitability and forecasted earnings growth of 75.55% per year reinforce its potential as an undervalued investment in Singapore's market.

- Upon reviewing our latest growth report, Seatrium's projected financial performance appears quite optimistic.

- Navigate through the intricacies of Seatrium with our comprehensive financial health report here.

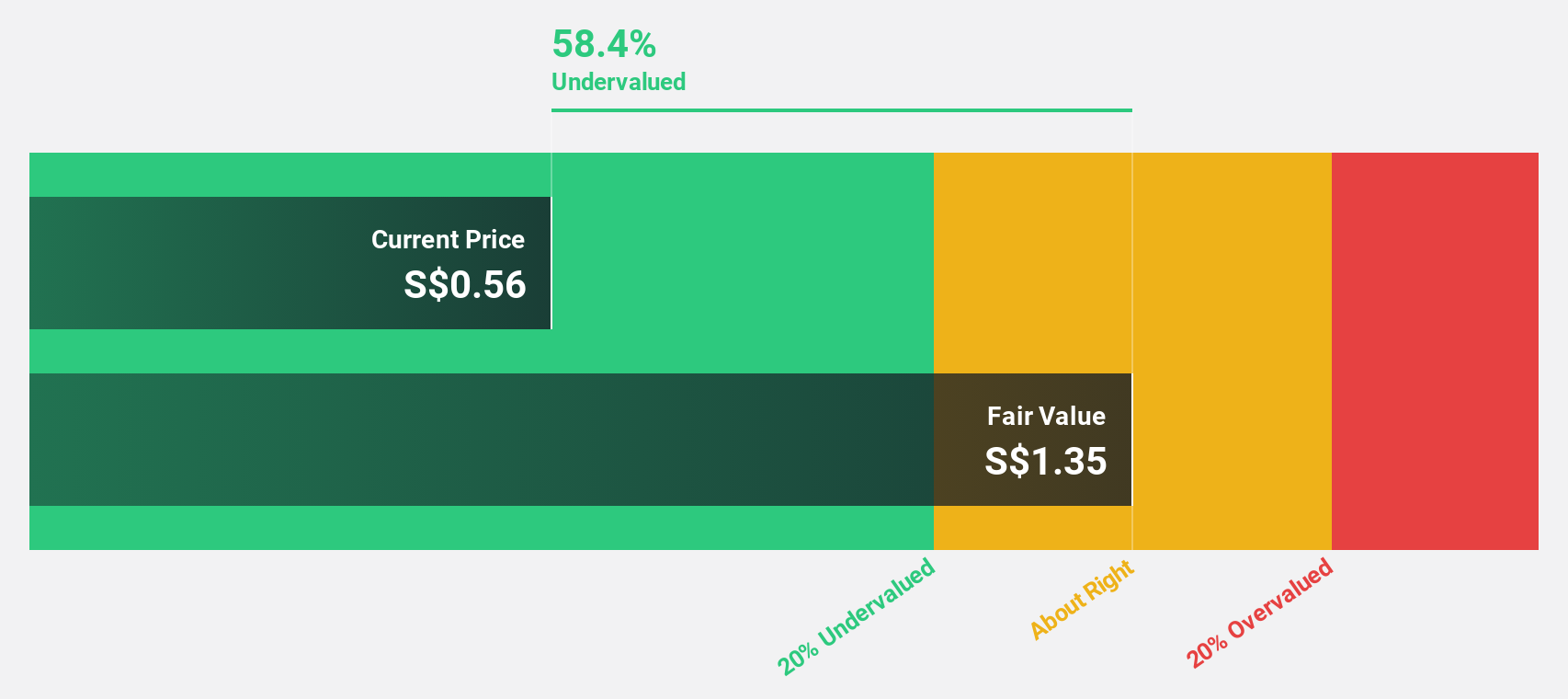

Frasers Logistics & Commercial Trust (SGX:BUOU)

Overview: Frasers Logistics & Commercial Trust (SGX:BUOU) is a Singapore-listed real estate investment trust with a market cap of S$4.13 billion, managing a diversified portfolio of 107 industrial and commercial properties valued at approximately S$6.4 billion across Australia, Germany, Singapore, the United Kingdom, and the Netherlands.

Operations: FLCT generates revenue primarily from its portfolio of 107 industrial and commercial properties valued at approximately S$6.4 billion, located in Australia, Germany, Singapore, the United Kingdom, and the Netherlands.

Estimated Discount To Fair Value: 48.9%

Frasers Logistics & Commercial Trust is trading at S$1.1, significantly below its estimated fair value of S$2.15, highlighting its undervaluation based on cash flows. Despite an unstable dividend track record and low forecasted return on equity (5.8%), the trust's earnings are projected to grow 39.43% annually, outpacing the market average. However, debt coverage by operating cash flow remains a concern for investors considering this stock in Singapore's market.

- The growth report we've compiled suggests that Frasers Logistics & Commercial Trust's future prospects could be on the up.

- Click here to discover the nuances of Frasers Logistics & Commercial Trust with our detailed financial health report.

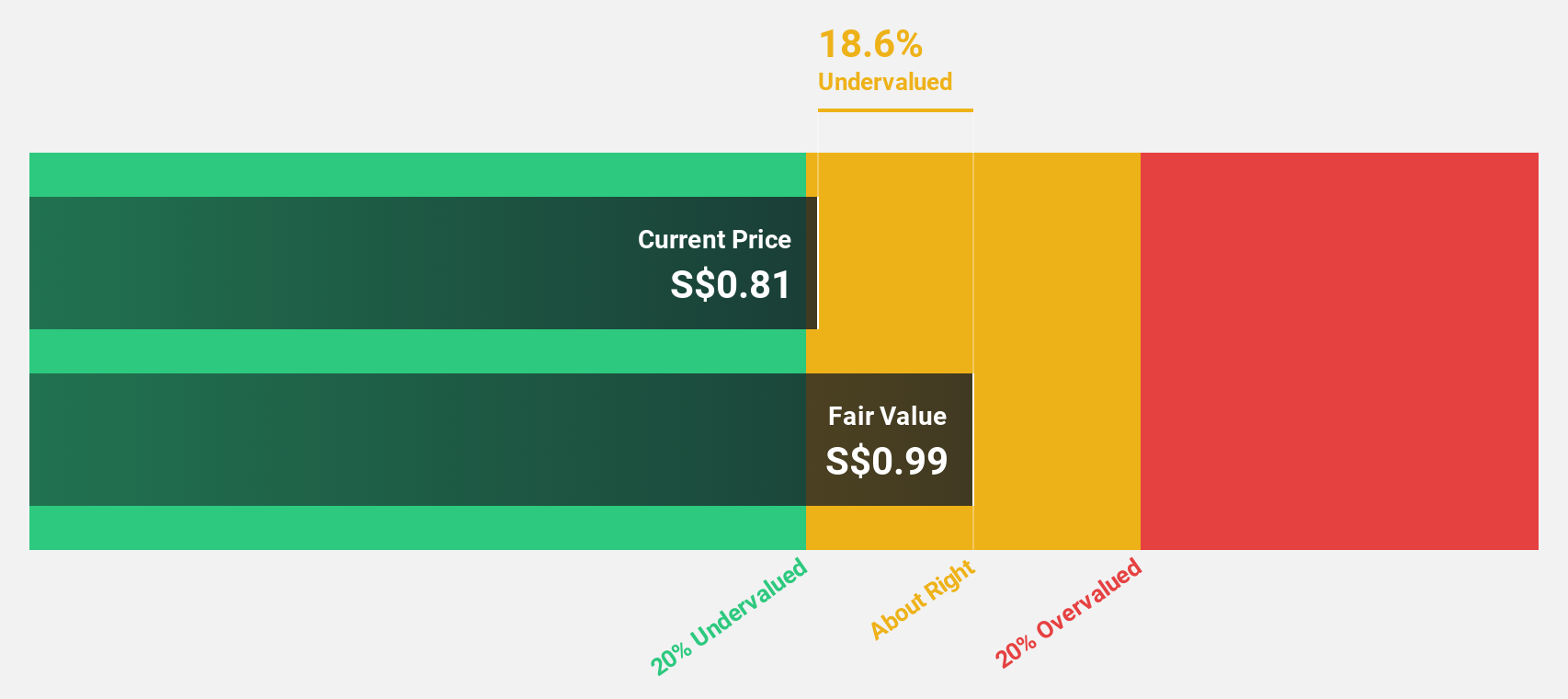

Nanofilm Technologies International (SGX:MZH)

Overview: Nanofilm Technologies International Limited, with a market cap of SGD504.59 million, provides nanotechnology solutions across Singapore, China, Japan, and Vietnam.

Operations: Nanofilm Technologies International Limited generates revenue from four main segments: Sydrogen (SGD1.40 million), Nanofabrication (SGD18.37 million), Advanced Materials (SGD153.32 million), and Industrial Equipment (SGD28.71 million).

Estimated Discount To Fair Value: 45.5%

Nanofilm Technologies International is trading at S$0.78, significantly below its estimated fair value of S$1.42, indicating undervaluation based on cash flows. Despite a current net loss of S$3.74 million for H1 2024, revenue increased to S$82.65 million from last year’s S$73.15 million. The company anticipates higher revenues and profits for the second half of 2024, though full-year earnings are expected to be comparable to 2023's S$3 million due to lower projected second-half earnings.

- In light of our recent growth report, it seems possible that Nanofilm Technologies International's financial performance will exceed current levels.

- Dive into the specifics of Nanofilm Technologies International here with our thorough financial health report.

Seize The Opportunity

- Click through to start exploring the rest of the 3 Undervalued SGX Stocks Based On Cash Flows now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nanofilm Technologies International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:MZH

Nanofilm Technologies International

Provides nanotechnology solutions in Singapore, China, Japan, and Vietnam.

Flawless balance sheet with reasonable growth potential.