June 2024 Insight Into Three SGX Stocks Estimated Below Value

Reviewed by Simply Wall St

As Singapore's market continues to adapt to global digital trends, the introduction of innovative services like Visa's digital emergency card highlights the increasing reliance on technology in financial transactions. In this environment, identifying stocks that are potentially undervalued becomes particularly pertinent, as companies that leverage such technological advancements may present compelling opportunities for informed investors.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Singapore Technologies Engineering (SGX:S63) | SGD4.19 | SGD7.86 | 46.7% |

| LHN (SGX:41O) | SGD0.335 | SGD0.37 | 10.2% |

| Hongkong Land Holdings (SGX:H78) | US$3.20 | US$5.63 | 43.2% |

| Digital Core REIT (SGX:DCRU) | US$0.56 | US$1.10 | 49.3% |

| Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD0.96 | SGD1.63 | 41.1% |

| Seatrium (SGX:5E2) | SGD1.47 | SGD2.36 | 37.8% |

| Nanofilm Technologies International (SGX:MZH) | SGD0.745 | SGD1.34 | 44.2% |

Let's uncover some gems from our specialized screener

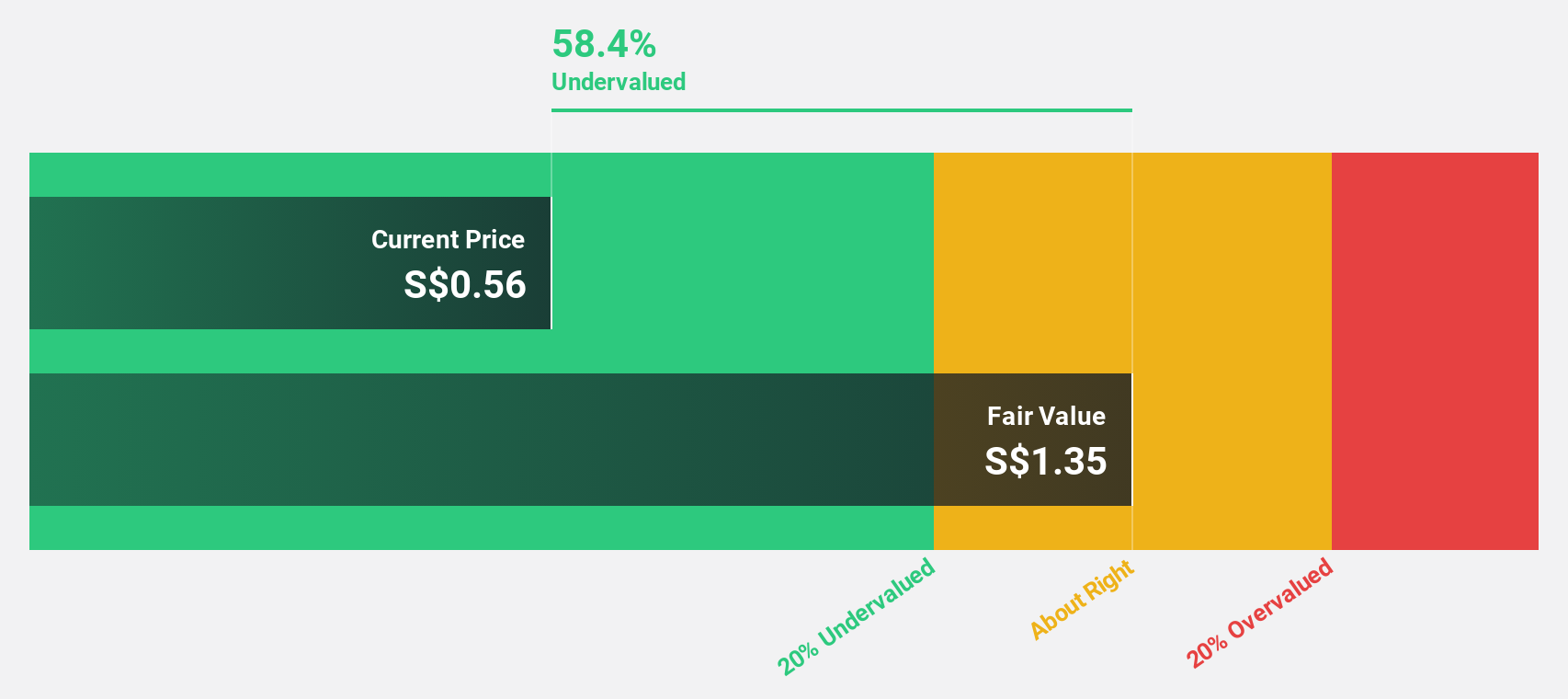

Frasers Logistics & Commercial Trust (SGX:BUOU)

Overview: Frasers Logistics & Commercial Trust (SGX:BUOU) is a Singapore-listed real estate investment trust that manages 107 industrial and commercial properties valued at approximately S$6.4 billion, across five developed markets including Australia, Germany, Singapore, the United Kingdom, and the Netherlands, with a market capitalization of about S$3.63 billion.

Operations: The revenue segments for the trust are not explicitly detailed in the provided text.

Estimated Discount To Fair Value: 41.1%

Frasers Logistics & Commercial Trust, trading at S$0.96, is noted to be significantly below its estimated fair value of S$1.63, indicating it may be undervalued based on discounted cash flow analysis. Despite a recent decrease in net income from S$118.07 million to S$93.59 million and unstable dividend records, the trust is expected to see revenue growth outpacing the Singapore market average and profit forecasts suggest improvement over the next three years. However, debt coverage by operating cash flow remains a concern.

- The growth report we've compiled suggests that Frasers Logistics & Commercial Trust's future prospects could be on the up.

- Unlock comprehensive insights into our analysis of Frasers Logistics & Commercial Trust stock in this financial health report.

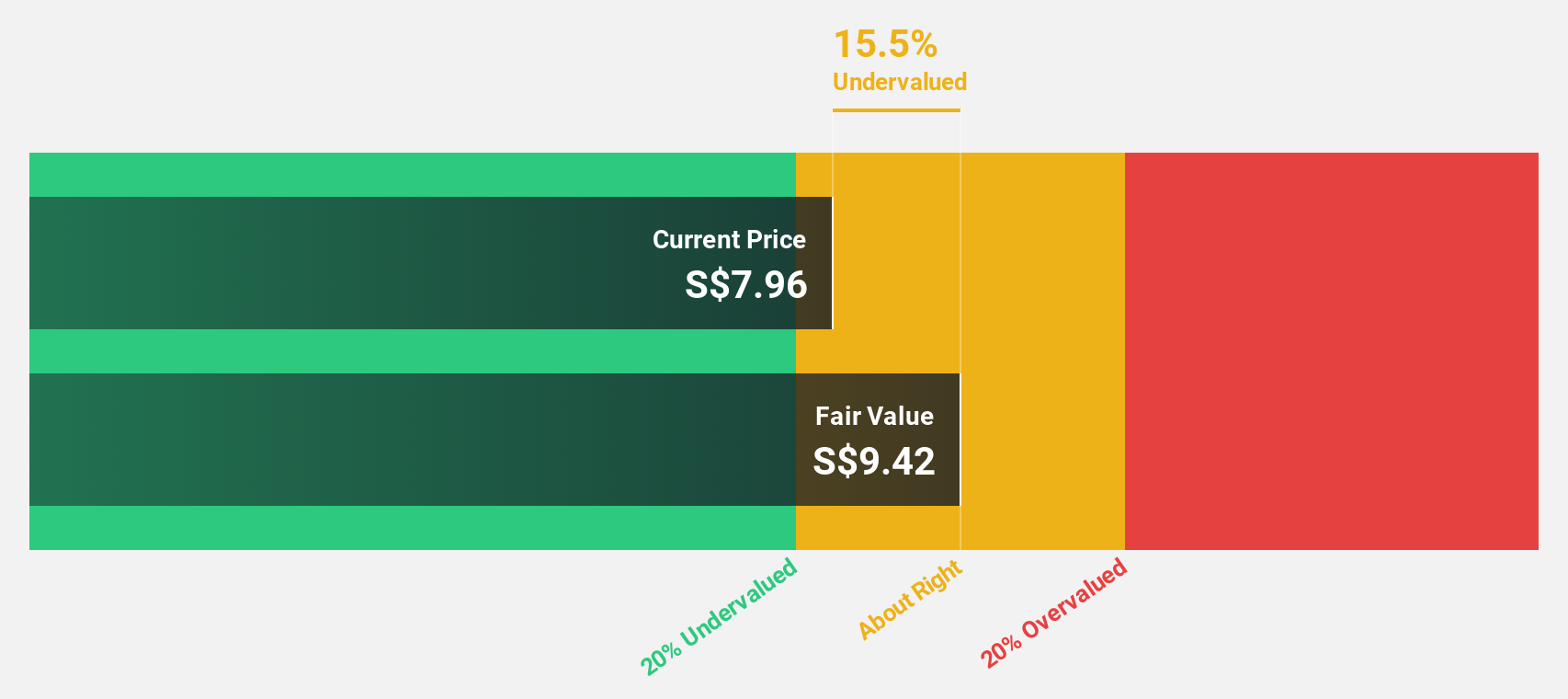

Nanofilm Technologies International (SGX:MZH)

Overview: Nanofilm Technologies International Limited offers nanotechnology solutions across Singapore, China, Japan, and Vietnam with a market capitalization of SGD 462.22 million.

Operations: The company generates revenue through several segments, including Sydrogen (SGD 1.05 million), Nanofabrication (SGD 16.05 million), Advanced Materials (SGD 141.54 million), and Industrial Equipment (SGD 37.17 million).

Estimated Discount To Fair Value: 44.2%

Nanofilm Technologies International, priced at SGD0.75, appears undervalued with an estimated fair value of SGD1.34. Despite a low return on equity forecast at 9% and profit margins decreasing from 18.5% to 1.8%, the company is poised for significant earnings growth, projected at 50.66% annually over three years and revenue growth forecasts of 15.1% annually outstripping the Singapore market's 3.6%. Recent corporate guidance confirms optimism for FY2024, expecting increased revenues and profits barring unforeseen events.

- Our earnings growth report unveils the potential for significant increases in Nanofilm Technologies International's future results.

- Navigate through the intricacies of Nanofilm Technologies International with our comprehensive financial health report here.

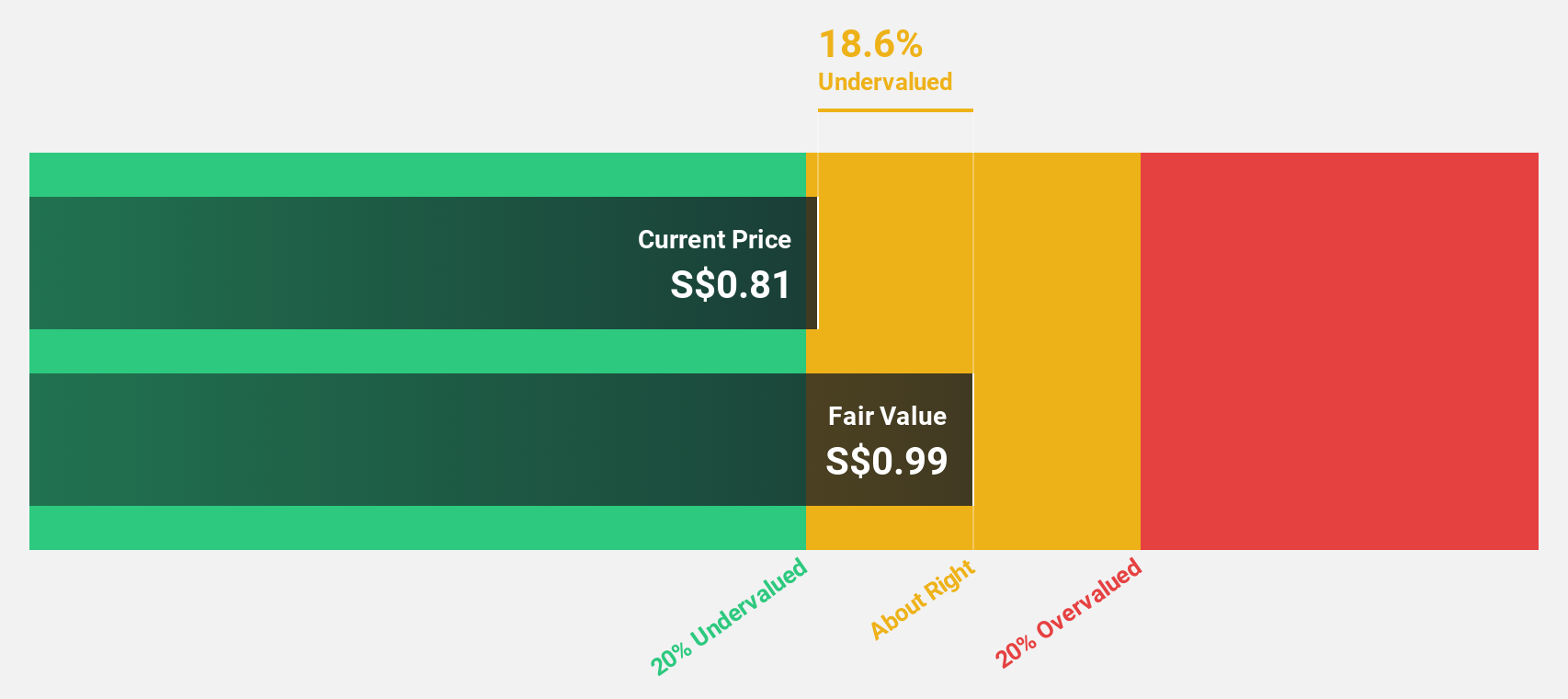

Singapore Technologies Engineering (SGX:S63)

Overview: Singapore Technologies Engineering Ltd is a global technology, defense, and engineering company with a market capitalization of SGD 12.91 billion.

Operations: The company's revenue is derived from three primary segments: Commercial Aerospace (SGD 3.97 billion), Urban Solutions & Satcom (SGD 1.98 billion), and Defence & Public Security (SGD 4.29 billion).

Estimated Discount To Fair Value: 46.7%

Singapore Technologies Engineering, priced at SGD4.19, trades below its estimated fair value of SGD7.86, indicating a potential undervaluation based on cash flows. Despite this, the company's financial position is burdened by high levels of debt and an unstable dividend track record. Recent strategic moves include a share buyback program and consistent dividends affirmations, reflecting confidence in operational stability and shareholder value enhancement. However, expected revenue growth at 6.9% annually lags behind more aggressive market averages.

- Insights from our recent growth report point to a promising forecast for Singapore Technologies Engineering's business outlook.

- Get an in-depth perspective on Singapore Technologies Engineering's balance sheet by reading our health report here.

Key Takeaways

- Get an in-depth perspective on all 7 Undervalued SGX Stocks Based On Cash Flows by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nanofilm Technologies International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:MZH

Nanofilm Technologies International

Provides nanotechnology solutions in Singapore, China, Japan, and Vietnam.

Flawless balance sheet with reasonable growth potential.