Stock Analysis

- Singapore

- /

- Aerospace & Defense

- /

- SGX:S63

Exploring Three SGX Stocks With Estimated Intrinsic Discounts Ranging From 40.5% to 41.9%

Reviewed by Simply Wall St

Amidst fluctuating performances akin to global tech giants, the Singapore market presents unique opportunities for investors seeking value. In the current environment, identifying stocks trading below their intrinsic value could offer potential advantages.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| LHN (SGX:41O) | SGD0.335 | SGD0.37 | 10% |

| Singapore Technologies Engineering (SGX:S63) | SGD4.37 | SGD7.40 | 40.9% |

| Winking Studios (Catalist:WKS) | SGD0.29 | SGD0.51 | 42.8% |

| Hongkong Land Holdings (SGX:H78) | US$3.38 | US$5.81 | 41.9% |

| Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD0.995 | SGD1.67 | 40.5% |

| Seatrium (SGX:5E2) | SGD1.47 | SGD2.63 | 44% |

| Digital Core REIT (SGX:DCRU) | US$0.625 | US$1.11 | 43.9% |

| Nanofilm Technologies International (SGX:MZH) | SGD0.95 | SGD1.48 | 35.7% |

We'll examine a selection from our screener results.

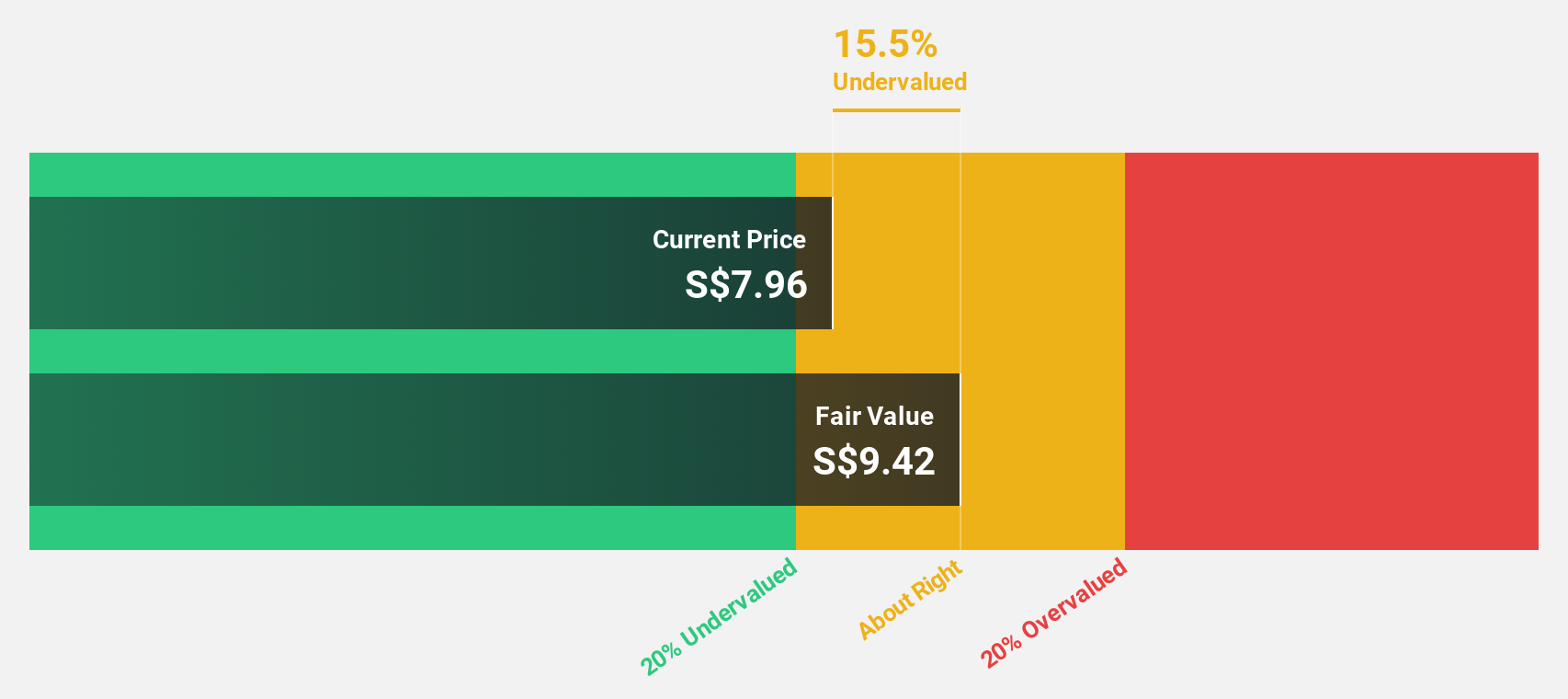

Frasers Logistics & Commercial Trust (SGX:BUOU)

Overview: Frasers Logistics & Commercial Trust (SGX:BUOU) is a Singapore-listed real estate investment trust specializing in industrial and commercial properties, with a portfolio valued at approximately S$6.4 billion across Australia, Germany, Singapore, the United Kingdom, and the Netherlands, and a market capitalization of about S$3.74 billion.

Operations: The trust generates revenue from a portfolio of 107 industrial and commercial properties located in Australia, Germany, Singapore, the United Kingdom, and the Netherlands.

Estimated Discount To Fair Value: 40.5%

Frasers Logistics & Commercial Trust is trading at a significant discount, valued 40.5% below its estimated fair value, indicating potential undervaluation based on cash flows. Despite this, the trust faces challenges with debt not well covered by operating cash flow and an unstable dividend track record. Analysts expect a revenue growth of 6.1% per year and forecast the company to become profitable within three years, outpacing the average market growth rate. Recent financial results show a decrease in net income from SGD 118.07 million to SGD 93.59 million year-over-year, reflecting some earnings pressure despite higher sales figures.

- Upon reviewing our latest growth report, Frasers Logistics & Commercial Trust's projected financial performance appears quite optimistic.

- Get an in-depth perspective on Frasers Logistics & Commercial Trust's balance sheet by reading our health report here.

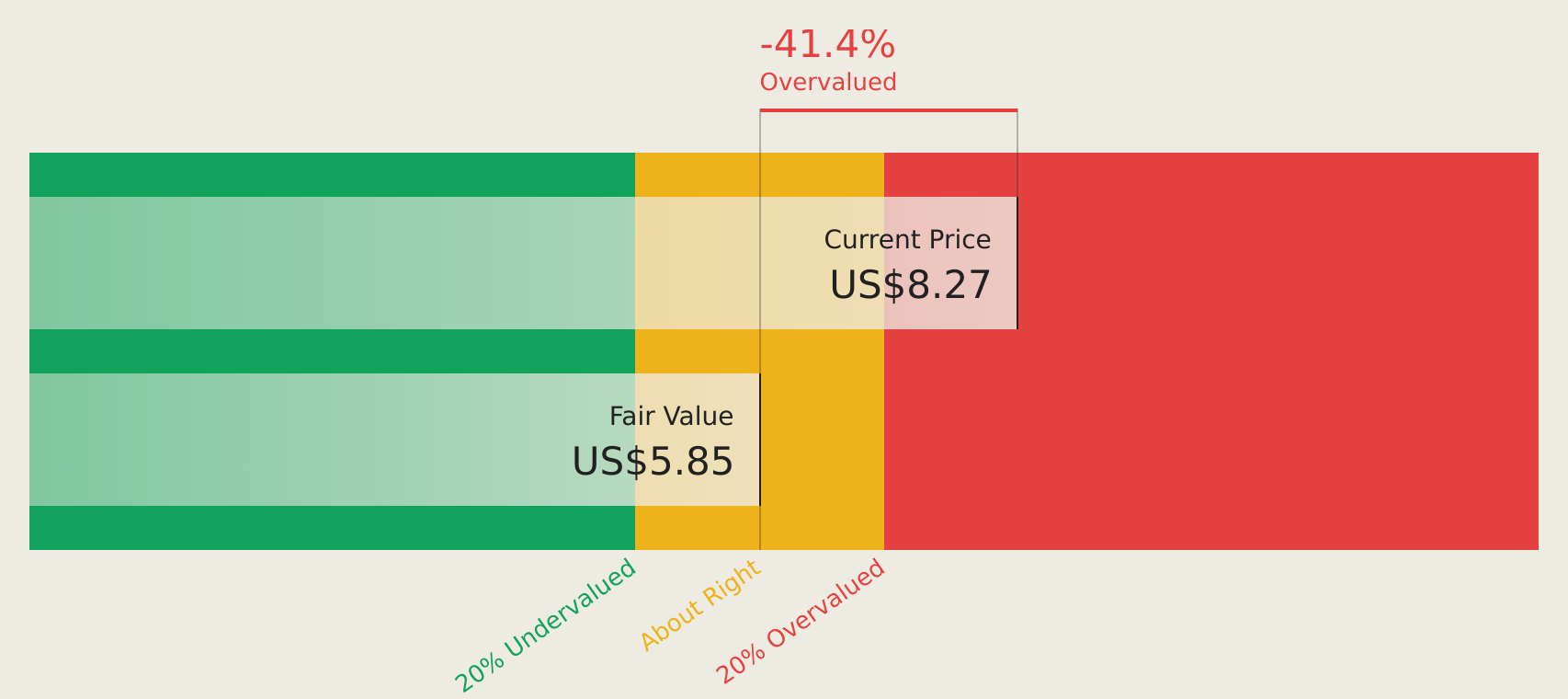

Hongkong Land Holdings (SGX:H78)

Overview: Hongkong Land Holdings Limited operates in the investment, development, and management of properties across Hong Kong, Macau, Mainland China, Southeast Asia, and other international locations with a market capitalization of approximately $7.46 billion.

Operations: The company generates revenue through two primary segments: Investment Properties, which brought in $1.08 billion, and Development Properties, contributing $0.76 billion.

Estimated Discount To Fair Value: 41.9%

Hongkong Land Holdings is perceived as undervalued, trading at S$3.38 against a fair value of S$5.81, marking a 41.9% discount. Despite modest revenue growth projections at 4.6% annually, which surpasses Singapore's market average of 3.6%, its dividend coverage by earnings remains weak. The company's return on equity is anticipated to remain low at 2.4% over the next three years, though it is expected to turn profitable within this period with earnings forecasted to grow by 43.34% annually.

- The growth report we've compiled suggests that Hongkong Land Holdings' future prospects could be on the up.

- Unlock comprehensive insights into our analysis of Hongkong Land Holdings stock in this financial health report.

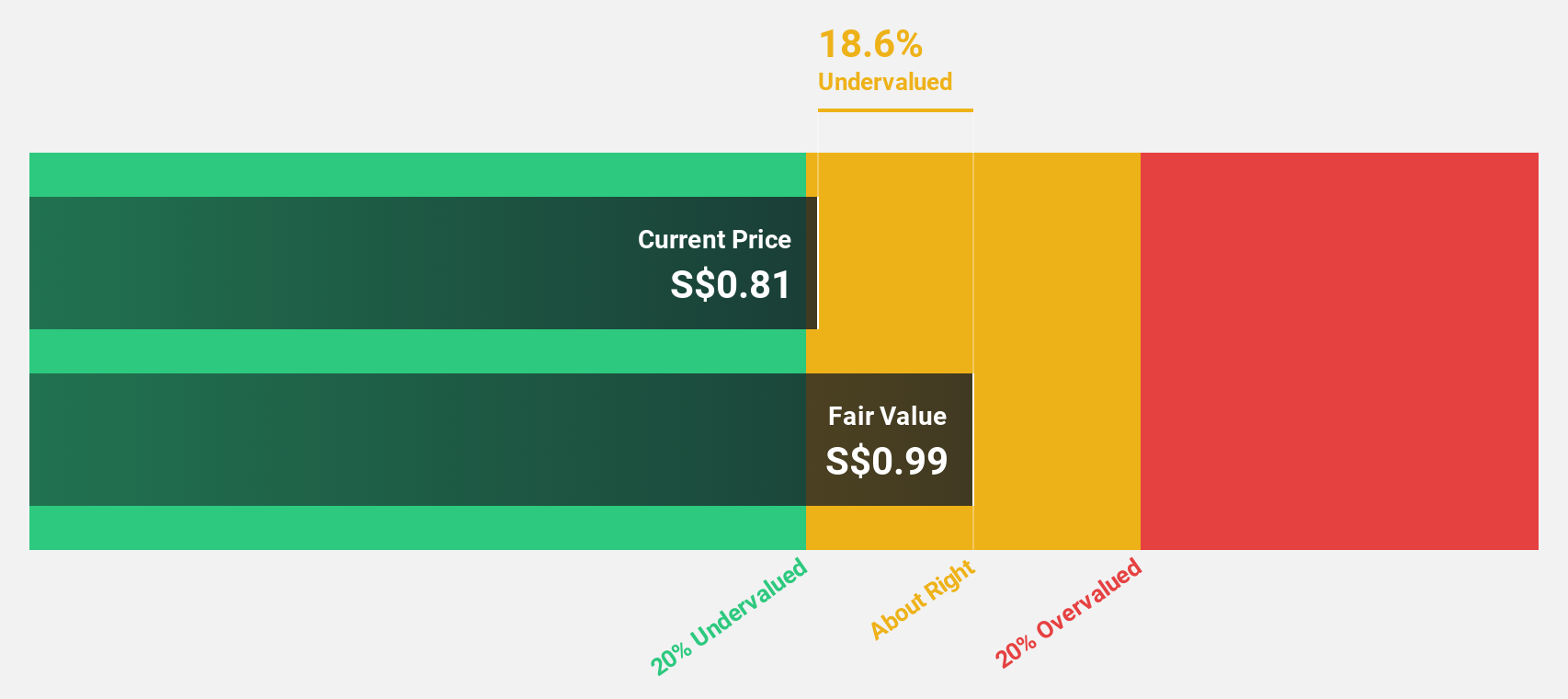

Singapore Technologies Engineering (SGX:S63)

Overview: Singapore Technologies Engineering Ltd is a global technology, defense, and engineering group with a market capitalization of approximately SGD 13.63 billion.

Operations: The company's revenue is segmented into Commercial Aerospace (SGD 3.97 billion), Urban Solutions & Satcom (SGD 1.98 billion), and Defence & Public Security (SGD 4.29 billion).

Estimated Discount To Fair Value: 40.9%

Singapore Technologies Engineering, valued at S$4.37, is currently trading 40.9% below its estimated fair value of S$7.4, indicating potential undervaluation based on discounted cash flows. While the company's revenue growth forecast at 6.5% annually outpaces the Singapore market average of 3.6%, its earnings growth is less impressive at 11.7% annually compared to a significant benchmark of over 20%. Additionally, despite a high forecasted return on equity at 27.5%, it carries a high level of debt which could be concerning for risk-averse investors.

- In light of our recent growth report, it seems possible that Singapore Technologies Engineering's financial performance will exceed current levels.

- Delve into the full analysis health report here for a deeper understanding of Singapore Technologies Engineering.

Summing It All Up

- Gain an insight into the universe of 8 Undervalued SGX Stocks Based On Cash Flows by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Singapore Technologies Engineering is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:S63

Singapore Technologies Engineering

Operates as a technology, defence, and engineering company worldwide.

Good value with reasonable growth potential.