Stock Analysis

There's Been No Shortage Of Growth Recently For Nordic LEVEL Group AB (publ.)'s (STO:LEVEL) Returns On Capital

If you're looking for a multi-bagger, there's a few things to keep an eye out for. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So when we looked at Nordic LEVEL Group AB (publ.) (STO:LEVEL) and its trend of ROCE, we really liked what we saw.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Nordic LEVEL Group AB (publ.), this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.012 = kr2.6m ÷ (kr398m - kr181m) (Based on the trailing twelve months to December 2023).

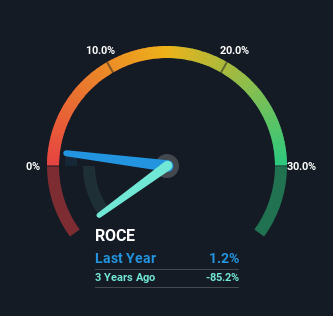

Therefore, Nordic LEVEL Group AB (publ.) has an ROCE of 1.2%. Ultimately, that's a low return and it under-performs the Electronic industry average of 18%.

See our latest analysis for Nordic LEVEL Group AB (publ.)

Historical performance is a great place to start when researching a stock so above you can see the gauge for Nordic LEVEL Group AB (publ.)'s ROCE against it's prior returns. If you'd like to look at how Nordic LEVEL Group AB (publ.) has performed in the past in other metrics, you can view this free graph of Nordic LEVEL Group AB (publ.)'s past earnings, revenue and cash flow.

How Are Returns Trending?

Nordic LEVEL Group AB (publ.) has recently broken into profitability so their prior investments seem to be paying off. Shareholders would no doubt be pleased with this because the business was loss-making five years ago but is is now generating 1.2% on its capital. Not only that, but the company is utilizing 814% more capital than before, but that's to be expected from a company trying to break into profitability. We like this trend, because it tells us the company has profitable reinvestment opportunities available to it, and if it continues going forward that can lead to a multi-bagger performance.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 46%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. This tells us that Nordic LEVEL Group AB (publ.) has grown its returns without a reliance on increasing their current liabilities, which we're very happy with. However, current liabilities are still at a pretty high level, so just be aware that this can bring with it some risks.

Our Take On Nordic LEVEL Group AB (publ.)'s ROCE

Overall, Nordic LEVEL Group AB (publ.) gets a big tick from us thanks in most part to the fact that it is now profitable and is reinvesting in its business. Astute investors may have an opportunity here because the stock has declined 62% in the last five years. With that in mind, we believe the promising trends warrant this stock for further investigation.

One more thing: We've identified 5 warning signs with Nordic LEVEL Group AB (publ.) (at least 3 which are concerning) , and understanding them would certainly be useful.

While Nordic LEVEL Group AB (publ.) may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're helping make it simple.

Find out whether Nordic LEVEL Group AB (publ.) is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:LEVEL

Nordic LEVEL Group AB (publ.)

Nordic LEVEL Group AB (publ.) provides safety and security solutions primarily in Sweden.

Undervalued with reasonable growth potential.