Advertisement

Insider Buying Drives These 3 Undervalued Small Caps Across Regions

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have seen significant gains, with the Russell 2000 Index reaching record highs, signaling a renewed interest in small-cap stocks amid broader market optimism. Despite geopolitical tensions and mixed economic data, investor sentiment remains buoyant, driven by domestic policy developments and robust consumer spending. In this context, identifying promising small-cap stocks often involves looking for those with strong fundamentals and potential catalysts such as insider buying trends that may indicate confidence from within the company.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Paradeep Phosphates | 24.9x | 0.8x | 26.28% | ★★★★★☆ |

| Maharashtra Seamless | 9.8x | 1.7x | 36.14% | ★★★★★☆ |

| PSC | 7.9x | 0.4x | 41.54% | ★★★★☆☆ |

| Optima Health | NA | 1.2x | 39.04% | ★★★★☆☆ |

| NCL Industries | 15.6x | 0.6x | -89.31% | ★★★☆☆☆ |

| Semen Indonesia (Persero) | 20.1x | 0.6x | 31.24% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| HighPeak Energy | 11.7x | 1.7x | 32.00% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -80.23% | ★★★☆☆☆ |

| Sabre | NA | 0.5x | -90.74% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

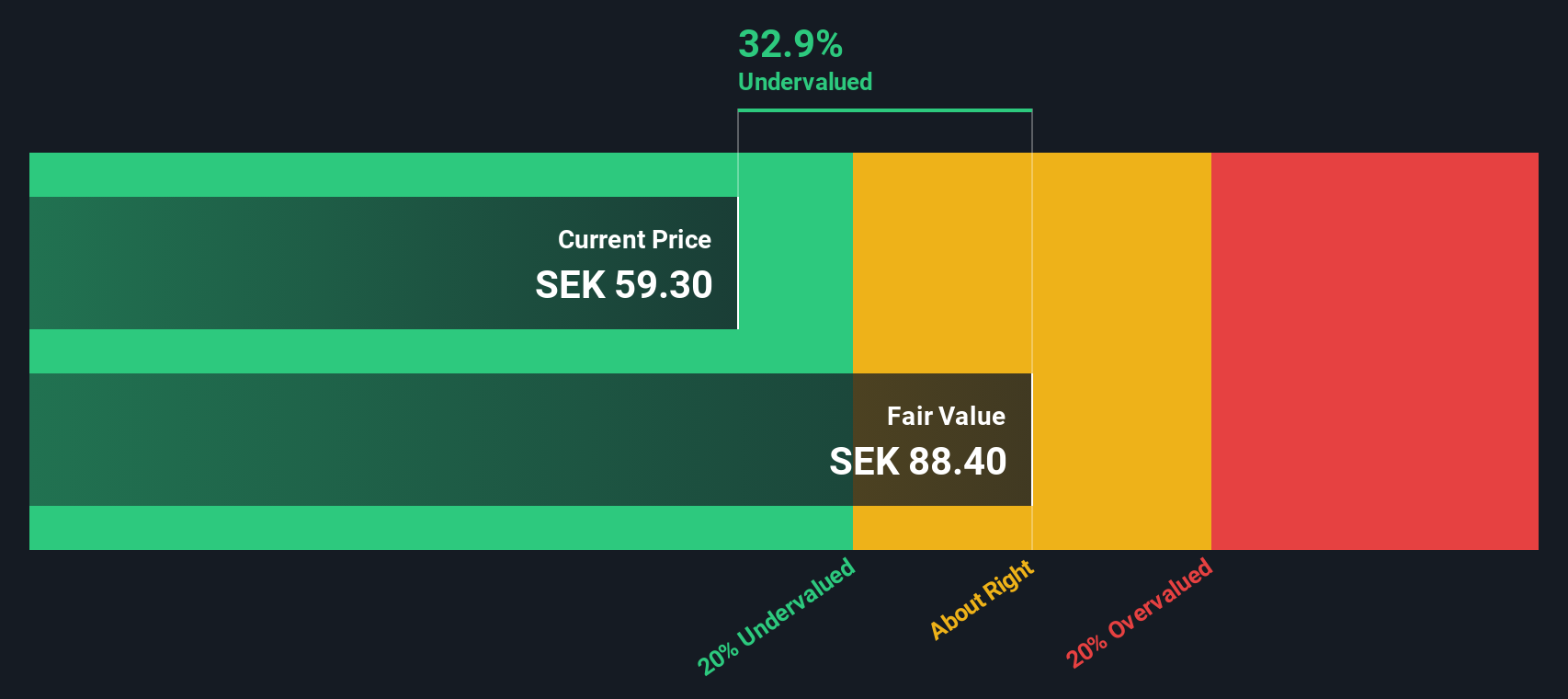

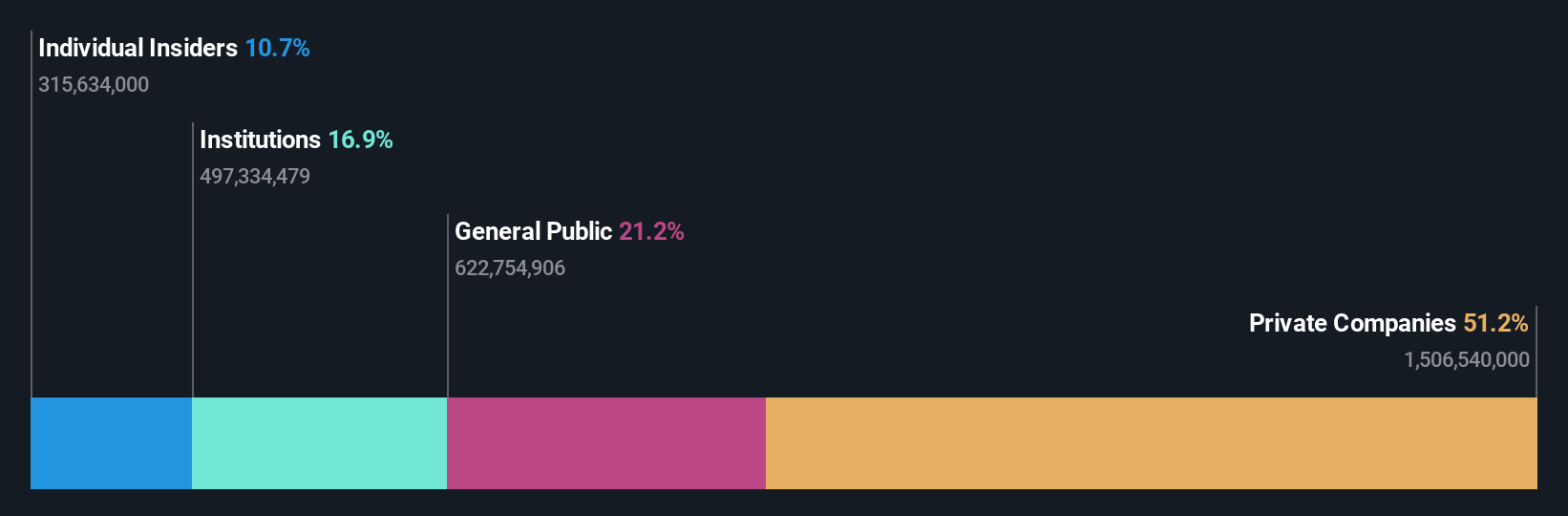

Nolato (OM:NOLA B)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Nolato is a Swedish company specializing in the development and production of polymer product systems for medical, consumer electronics, and industrial sectors, with a market capitalization of approximately SEK 16.23 billion.

Operations: The company generates revenue primarily from its Medical Solutions segment, which contributed SEK 5.38 billion. Over recent periods, the gross profit margin has shown fluctuations, reaching 16.36% as of September 2024. Operating expenses have consistently included significant allocations to sales and marketing alongside general and administrative costs.

PE: 25.5x

Nolato, a smaller company in its sector, has shown promising financial performance with a net income increase to SEK 164 million for Q3 2024, up from SEK 69 million the previous year. Despite relying on external borrowing for funding, which presents higher risk without customer deposits, their earnings are projected to grow by 18.66% annually. Insider confidence is evident as they have been purchasing shares throughout the year. This blend of growth potential and insider activity suggests a positive outlook amidst funding challenges.

- Navigate through the intricacies of Nolato with our comprehensive valuation report here.

Examine Nolato's past performance report to understand how it has performed in the past.

VBG Group (OM:VBG B)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: VBG Group is a diversified industrial company specializing in mobile thermal solutions, truck and trailer equipment, and power transmission products, with a market capitalization of approximately SEK 9.51 billion.

Operations: The company's revenue is primarily driven by Mobile Thermal Solutions, followed by Truck & Trailer Equipment and RINGFEDER Power Transmission. Over the periods analyzed, the gross profit margin has shown fluctuations, reaching 32.74% in September 2024. Operating expenses are significant, with major allocations to sales and marketing as well as research and development efforts.

PE: 12.0x

VBG Group's recent earnings report for Q3 2024 showed a decline in quarterly sales to SEK 1,272.9 million from SEK 1,439.8 million the previous year, with net income also dropping to SEK 112.3 million from SEK 158.9 million. However, nine-month figures reveal resilience with sales slightly increasing to SEK 4,302.3 million and net income rising to SEK 475.9 million from last year's figures of SEK 439.1 million. Insider confidence is evident as they have been purchasing shares consistently throughout the year, suggesting potential optimism about future performance despite reliance on external borrowing for funding and moderate projected growth of around 2% annually in earnings or revenue.

- Get an in-depth perspective on VBG Group's performance by reading our valuation report here.

Review our historical performance report to gain insights into VBG Group's's past performance.

SSY Group (SEHK:2005)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: SSY Group is a company engaged in the production and sale of medical materials and intravenous infusion solutions, with a market capitalization of HK$9.68 billion.

Operations: The company's primary revenue stream is from Intravenous Infusion Solution and Others, generating HK$6.30 billion, while Medical Materials contribute HK$402.49 million. Over recent periods, the net income margin has shown an upward trend, reaching 21.11% by mid-2024. Operating expenses have been a significant cost component, with Sales & Marketing being the largest expense within this category.

PE: 7.8x

SSY Group's recent insider confidence is evident as their Chairman & CEO purchased 1.5 million shares for HK$7.5 million, indicating belief in the company's potential despite higher risk funding through external borrowing. The company has made strides with multiple drug approvals from China's National Medical Products Administration, including treatments for tuberculosis and pain management, which could enhance its market position. Earnings are projected to grow by 6.77% annually, suggesting possible future value growth amidst these developments.

- Click to explore a detailed breakdown of our findings in SSY Group's valuation report.

Understand SSY Group's track record by examining our Past report.

Taking Advantage

- Get an in-depth perspective on all 188 Undervalued Small Caps With Insider Buying by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2005

SSY Group

An investment holding company, researches, develops, manufactures, trades in, and sells various pharmaceutical products to hospitals and distributors in the People’s Republic of China and internationally.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor